Oil Storm: Trump Imposes a Blockade on Iran as Prices Surge 10 Percent

Introduction: An Escalation That Changes the Rules of the Game

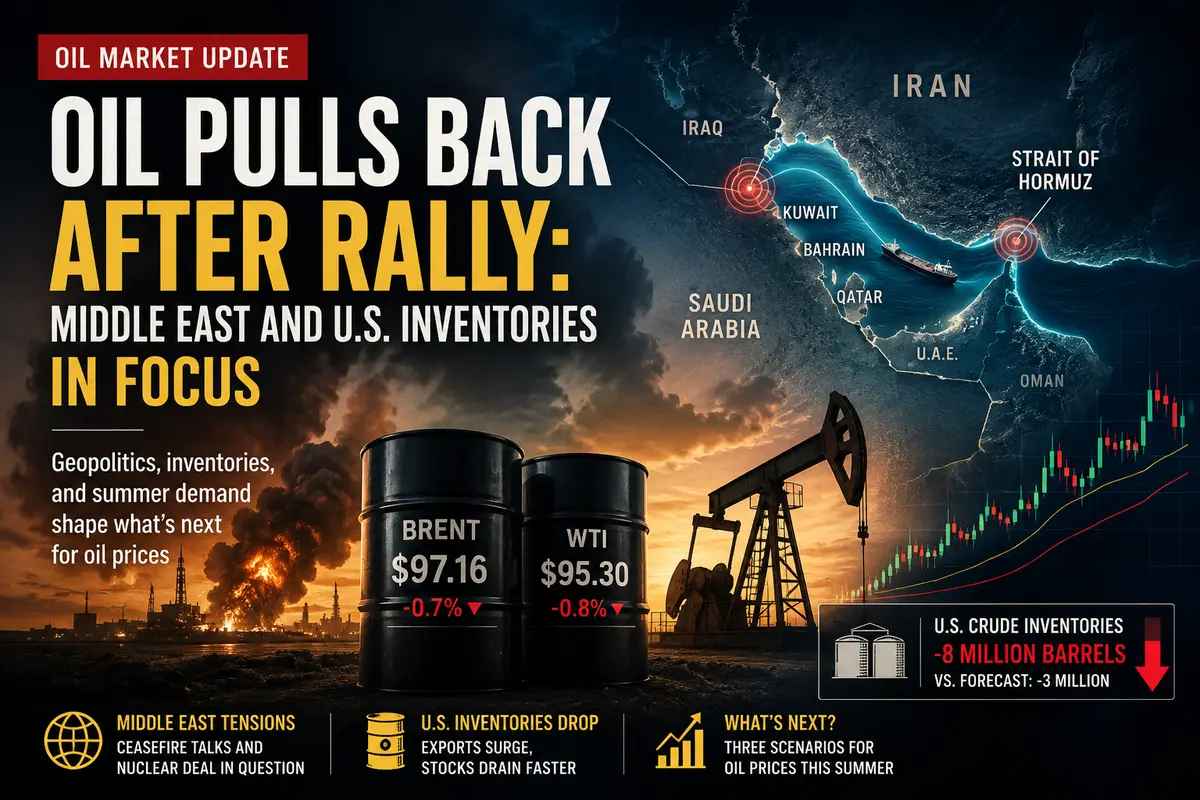

Tuesday began with a new round of escalation in the oil markets. President Donald Trump announced the reinstatement of a naval blockade against Iran and the introduction of a 20 percent transit fee on cargo passing through the Strait of Hormuz. Oil prices reacted immediately: Brent crude rose 2.1 percent to $85.01 per barrel, while WTI gained 2.1 percent to $79.78.

However, this was merely a continuation of the rally that began on Monday, when both global benchmark grades jumped by nearly 10 percent—their largest one-day increase in several months. Tensions between the United States and Iran have reached a new level, and markets are pricing in the risk of serious disruptions to oil supplies from the Persian Gulf.

What is behind this decision? What are the consequences for the global economy? And where will prices move next? In this article, we examine every aspect of the current crisis and its impact on the oil markets.

The Blockade of Iran: Trump’s Decisive Move

The Reinstatement of the Naval Blockade

President Trump stated that the United States would reinstate its naval blockade of Iran following the resumption of military clashes with Tehran. The decision came in response to Iranian drone strikes on US facilities in Kuwait and attacks on vessels in the Strait of Hormuz.

The US Armed Forces will begin enforcing the blockade on Tuesday, targeting vessels linked to Iran. Neutral commercial vessels will still be permitted to pass through the strait. This is an important distinction, demonstrating that the United States is attempting to restrict Iranian shipments rather than completely shut down maritime traffic.

A 20 Percent Transit Fee

Trump also announced that Washington would charge a 20 percent fee on cargo passing through the Strait of Hormuz to...