Gold in a Trap: How Iran Talks Have Pushed the Metal Into Its Tightest Range in Months

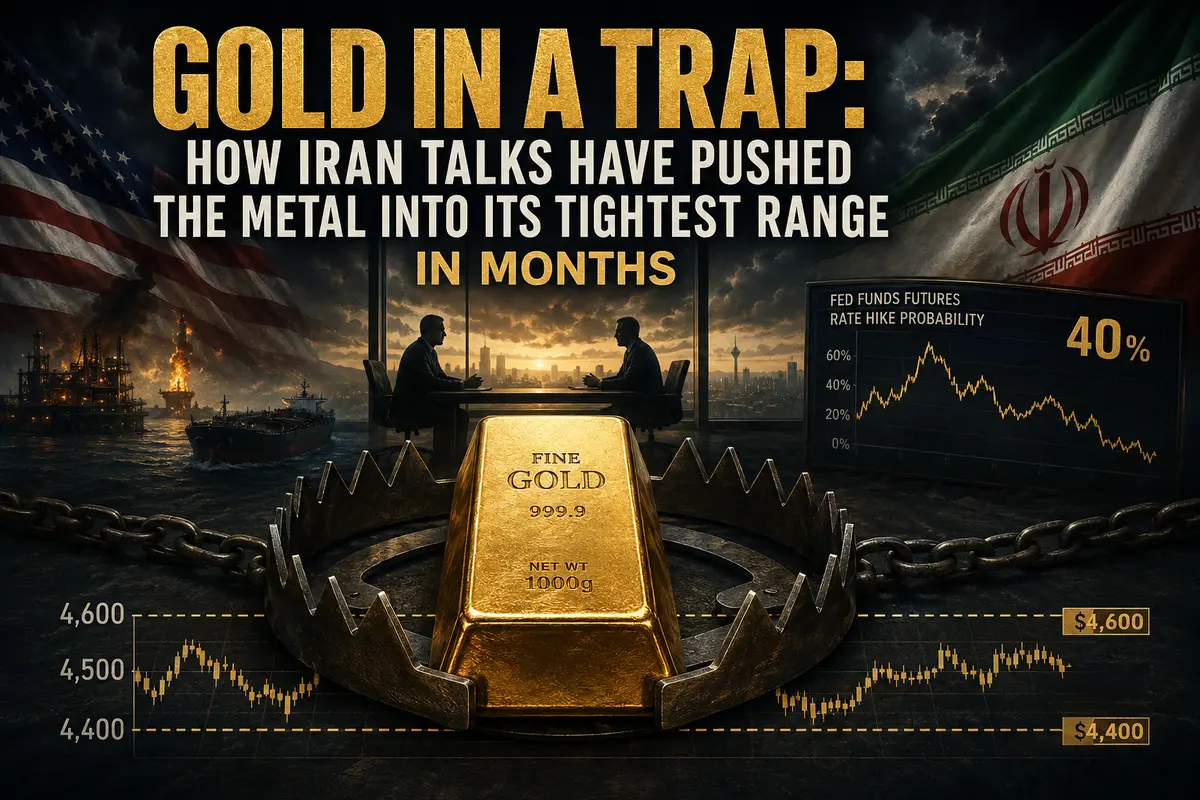

Ten days. Ten long days that spot gold has been unable to break out of the range between $4,400 and $4,600 per ounce. For an asset accustomed to swinging hundreds of dollars in a single session, this is an agonizingly narrow corridor. Gold is stuck as if trapped in a vise, with neither bulls nor bears able to move it from dead center.

On Wednesday morning, spot prices edged up a symbolic 0.2% to $4,518. Futures added 0.3%, reaching $4,550. The move is so modest it almost feels embarrassing to call it a rally. Yet beneath this apparent stillness lies a fierce battle between two opposing forces, each pulling gold in its own direction. And the name of those forces is Iran.

Negotiations That Suffocate and Save at the Same Time

The main reason gold cannot decide on a direction is the stream of contradictory signals coming from the peace negotiations between the United States and Iran.

On Monday, U.S. forces struck targets in southern Iran. Gold, as expected, fell. Why did it fall instead of rise? Because the logic of the current conflict has turned traditional market relationships upside down.

Normally, war is fuel for gold. Investors flee risk, buy safe-haven assets, and the yellow metal rises. But this war is different. It has created an energy crisis that accelerated inflation. Inflation, in turn, has forced central banks to threaten higher interest rates. And the threat of higher rates is deadly poison for gold, which yields no interest income.

That is why the bombing of Iran is not pushing gold higher — it is dragging it lower instead. The market fears not the war itself, but its monetary consequences.

At the same time, however, negotiations continue. Diplomats remain at the table, discussing terms and exchanging draft agreements. Every headline suggesting progress affects gold in exactly the opposite way.

Hope for peace means hope for the reopening of the Strait of Hormuz, lower oil prices, easing inflationary pressure, and therefore a lower probability of rate hikes. And a lower probability of higher rates is a green light for gold. So on days when the talks appear to be going well, gold rises.

This paradox has created a perfect storm of uncertainty. Traders do not know what to do. Buy gold in anticipation of peace? Or sell it in anticipation of war? The answer depends entirely on the next headline.

And while headlines swing between “Trump announces progress” and “The U.S. launches new strikes,” gold remains trapped in its ten-day corridor, unable to break either the upper or lower boundary.

Forty Percent Chance of a Hike: The Market Guesses the Fed’s Next Move

While gold drifts sideways, the Fed futures market paints an intriguing picture. According to CME FedWatch data, the probability of a rate hike by December is now close to 40%.

That is not a majority, but it is remarkably high for a market that only a few months ago did not believe further tightening was possible at all.

What stands behind that 40%? Fear.

Fear that inflation, fueled by expensive oil, will prove persistent. Fear that central banks will have to act more aggressively than planned. Fear that the soft landing everyone hoped for will turn into a hard landing accompanied by fresh rate hikes.

March and April inflation data already showed a sharp rise in energy-driven prices. And although oil has pulled back somewhat from its highs in May, it remains expensive enough to continue pressuring consumer prices.

For gold, this is a direct threat. Every additional percentage point in the probability of a rate hike acts like a weight chained to the yellow metal’s legs.

With a 40% chance of higher rates, gold cannot rally confidently. But with a 60% probability that rates will remain unchanged or even decline, it cannot fall decisively either. Hence this painful sideways grind.

Ten Days Inside a Box: The Anatomy of Stagnation

The ten-day range between $4,400 and $4,600 is not merely a technical detail. It reflects the psychological paralysis gripping the market.

Two hundred dollars — that is the width of the corridor. For gold, it is a narrow crack. Historically, such tight ranges often precede powerful moves, like a compressed spring that eventually snaps loose.

Why can gold not break above the upper boundary? Because every time the price approaches $4,600, sellers step in, remembering the 40% probability of a rate hike. They sell to lock in profits or open short positions.

Why can gold not break below the lower boundary? Because around $4,400, buyers emerge, seeing persistent geopolitical uncertainty and the potential for monetary easing if a peace deal is reached. They buy aggressively, creating support.

The result is a perfect equilibrium of fear and greed.

Bears fear peace, which could weaken the dollar and bond yields. Bulls fear war, which could intensify inflation and force the Fed to tighten policy further.

And as long as this balance remains intact, gold will continue moving in circles.

Silver and Platinum: Different Destinies

Other precious metals showed mixed performance on Wednesday.

Silver rose 0.2%, following gold higher. Its situation is particularly interesting because silver has a dual nature — both a safe-haven asset and an industrial metal. Hopes for peace support industrial demand from electronics and solar panels, while fears of higher rates pressure it as a defensive asset. These two forces are nearly balancing each other out.

Platinum fell 0.7%. It is far more dependent on industrial demand, especially from the automotive sector, where it is used in catalytic converters. Ongoing uncertainty surrounding oil and the war is weighing on automakers, and therefore on platinum demand as well.

In addition, platinum does not enjoy the same safe-haven status as gold, so geopolitical fears provide far less support.

What Will Break the Range

The gold market now resembles a patient under anesthesia. It is alive, but motionless. To wake it up, a shock is needed. And there are only two possible shocks.

The first is a breakthrough in the Iran negotiations. If Trump and Iranian leaders actually sign an agreement, oil prices could collapse, inflation expectations would fall, the probability of rate hikes would decline, and gold could break above the upper boundary of the range, surging toward new highs.

The second is a complete collapse of negotiations and a fresh escalation of conflict. In that scenario, oil would likely spike again, inflation fears would intensify, the probability of rate hikes could jump to 50–60%, and gold would break below the lower boundary, falling under $4,400.

Until one of those scenarios materializes, gold will remain trapped inside the box.

Traders trying to play the breakout should prepare for patience. Ten days of sideways movement could easily become fifteen, twenty, or thirty. The market is waiting.

And whoever waits for the right moment may be rewarded. Whoever rushes risks ending up on the wrong side of the sharp move that inevitably follows a long consolidation.

Gold has frozen in place — but this is the calm before the storm. And the storm will be powerful.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.