Oil Pulls Back After Rally: Middle East and U.S. Inventories in Focus

The Three-Day Holiday Is Over

Thursday began with a reality check for the oil market. After three straight days of gains—delighting bulls, frustrating bears, and forcing traders to revise their models—the market finally saw a correction. A modest one. A measured one. Almost a polite one. But a correction nonetheless.

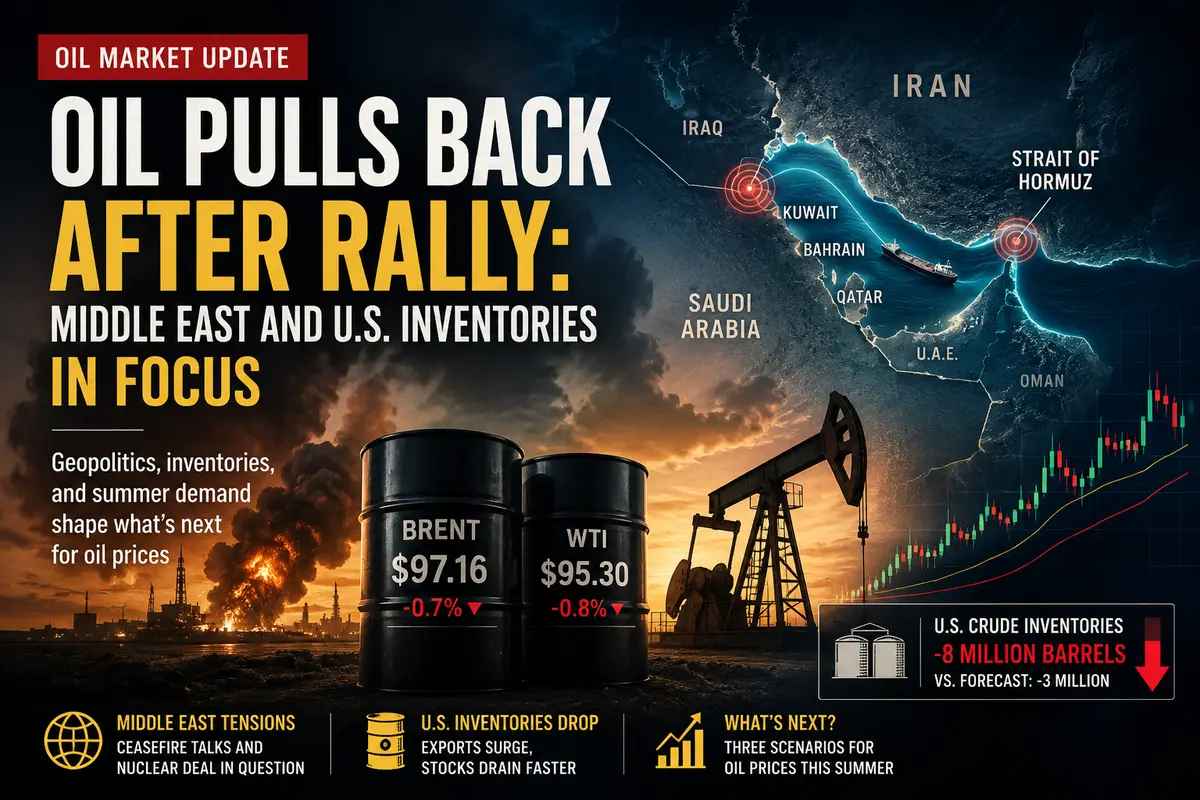

Brent crude futures, the European benchmark, were down 0.7% on Thursday morning, trading at $97.16 per barrel. Its American counterpart, WTI, slipped slightly more, losing 0.8% to $95.30 per barrel. Prices that would have seemed extraordinary just a week ago now look like business as usual.

Still, this decline is hardly dramatic. It is simply profit-taking. Investors who entered the market last week when prices were 5–7% lower have decided it is time to take some money off the table. They sell, prices fall. Nothing personal—just business.

Yet beneath this routine profit-taking lies something more interesting: risk assessment.

The oil market today resembles a tightrope walker balancing above a canyon. On one side is geopolitical turmoil in the Middle East; on the other are the hard numbers coming from U.S. crude inventories. Both factors are pushing prices higher. But there are forces pulling in the opposite direction as well. More on those shortly.

The Middle East: War, Ceasefire, and a Nuclear Deal

Let’s begin with the biggest source of oil market volatility in recent weeks: the Middle East—a region that gave the world agriculture, writing, and seemingly an endless supply of conflict.

Events unfolded at cinematic speed this week.

First came Iranian missile strikes against Kuwait and Bahrain. These small but wealthy Gulf monarchies, accustomed to life under the American security umbrella, suddenly found themselves on the front line. The missiles came from Iran—the United States’ primary regional adversary, Hezbollah’s main backer, and a perennial source of instability.

Then came the U.S. response: strikes on Iran’s Qeshm Island. Located in the Strait of Hormuz, the narrow waterway through which roughly one-fifth of the world’s oil passes, Qeshm is strategically significant. The strikes were more than a military operation; they were a message. Washington was effectively telling Tehran: “If you threaten the Strait, we will destroy your ability to do so.”

Meanwhile, Israel, America’s closest regional ally, expanded military operations in southern Lebanon, targeting areas controlled by Hezbollah. Backed by Iran, Hezbollah has long posed a major security threat to northern Israel and is widely regarded as the region’s most powerful proxy force.

By Wednesday evening, the picture looked grim: three active fronts, three conflicts, and no clear diplomatic solution in sight.

Then came an unexpected development.

Washington announced that Israel and Lebanon had agreed to implement a ceasefire arrangement. A breakthrough? Perhaps. But there was a catch. The agreement depends on Hezbollah halting military operations. And Hezbollah is not the Lebanese government. Beirut can sign whatever documents it likes; if Hezbollah chooses to continue firing rockets, the agreement will not be worth the paper it is written on.

Nevertheless, the very fact that negotiations are taking place is a positive signal. Markets prefer headlines about diplomacy to headlines about missiles. That is one reason oil prices eased on Thursday morning as part of the geopolitical risk premium was priced out.

The most surprising development came later when U.S. President Donald Trump stated in a podcast interview that Iran had agreed not to pursue nuclear weapons.

If true, the implications would be enormous. Iran’s nuclear program has been one of the West’s biggest strategic concerns for two decades. Sanctions, negotiations, threats, and covert operations have all revolved around one central question: will Iran obtain a nuclear weapon? If Tehran has genuinely abandoned that objective, the prospect of long-term stability in the region becomes more realistic.

If it is not true—and many analysts remain skeptical given the absence of any official confirmation from Tehran—oil could quickly resume its climb once the market realizes it was reacting to an unverified claim.

For now, traders are taking a wait-and-see approach. Thursday’s decline is not panic. It is caution. Everyone is waiting for confirmation or denial.

The Strait of Hormuz: The Achilles’ Heel of the Global Economy

The Strait of Hormuz deserves special attention. It is where geography meets geopolitics—and where oil prices are often determined.

The strait connects the Persian Gulf to the Indian Ocean. Its width ranges from roughly 30 to 90 kilometers, and it is deep enough to accommodate the world’s largest tankers. Around 20 million barrels of oil pass through it every day, accounting for approximately one-fifth of global consumption.

Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar all ship much of their oil through Hormuz. If the waterway were blocked, the world would lose roughly 20% of its oil supply overnight.

Iran, which controls the northern shoreline, has threatened for decades to close the strait in the event of conflict with the United States or its allies. Historically, those threats remained largely rhetorical because shutting down Hormuz would effectively mean declaring economic war on much of the world. However, after the U.S. strikes on Qeshm Island, such threats no longer feel quite as theoretical.

Investors monitor Hormuz the way a cardiologist monitors a patient’s pulse. Any reports involving naval deployments, mine-laying operations, or tanker seizures trigger immediate market reactions.

On Thursday, tensions eased somewhat following reports of a ceasefire initiative between Israel and Lebanon. Yet Qeshm Island remains a reminder that Hormuz is not merely a shipping lane—it is also a potential battlefield.

America Unexpectedly Supports Oil Prices

While geopolitics pushed prices higher, fresh data from the United States added further bullish momentum.

The U.S. Energy Information Administration (EIA) released its weekly crude inventory report for the week ending May 29.

The numbers were significantly stronger than expected—at least from the perspective of oil bulls. Crude inventories fell by 8 million barrels, compared with analyst expectations for a 3 million barrel decline. That is nearly three times the forecast and a powerful signal.

Why such a large drawdown?

The first reason is refinery activity. U.S. refiners are operating at high utilization rates ahead of the summer driving season. Demand for gasoline is rising as millions of Americans prepare for vacation travel. Refineries are consuming crude oil and converting it into fuel, reducing stockpiles.

The second factor is exports.

American crude has become an unexpected beneficiary of Middle Eastern instability. Buyers in Europe and Asia who once relied heavily on Persian Gulf supplies are increasingly seeking alternatives amid fears that regional conflict could disrupt exports.

They have found those alternatives in the United States.

U.S. crude exports climbed to 5.9 million barrels per day, one of the highest levels on record. Tankers loaded with oil from Texas and North Dakota are sailing across the Atlantic and Pacific, replacing barrels that would otherwise come from Saudi Arabia or the UAE.

For U.S. producers, this is a golden period. They receive prices linked to global markets rather than domestic benchmarks, generating stronger profits and encouraging additional drilling.

For the global market, however, it means that U.S. inventories—the most closely watched indicator of supply-demand balance—are shrinking faster than normal.

What Traders Fear: Critically Low Inventories

Perhaps the most concerning aspect of the EIA report is not the 8-million-barrel decline itself, but the broader trend.

The agency warns that global oil inventories are being drawn down rapidly. If the trend continues, stockpiles could reach critical levels just as peak summer demand arrives.

What does “critical levels” mean?

It means inventories become so tight that any disruption—a Gulf of Mexico hurricane, a pipeline outage, or renewed escalation in the Middle East—could trigger sharp price spikes. Not 5%, but potentially 20–30%.

The market would become highly sensitive to every headline.

Summer demand adds another layer of pressure. From May through September, global oil consumption typically rises as travel increases, air-conditioning demand surges, and industrial activity remains strong.

This year, against the backdrop of geopolitical uncertainty, seasonal demand could be the catalyst that pushes prices firmly back into triple-digit territory.

The traders who took profits on Thursday understand this perfectly well. They are not abandoning the oil market. They are simply stepping back and waiting for the next opportunity.

Diplomacy: A Fragile Hope

President Trump’s comments regarding Iran’s nuclear ambitions generated considerable attention.

If Iran has indeed agreed to abandon nuclear weapons development, a path toward sanctions relief could emerge. Sanctions relief would likely bring additional Iranian crude back onto the global market—potentially 1–2 million barrels per day—placing downward pressure on prices.

But there are too many uncertainties.

There has been no official confirmation from Tehran. Iranian media remain silent. European diplomats involved in discussions say they are unaware of any such agreement.

Perhaps Trump spoke prematurely. Perhaps he deliberately floated the information to gauge reactions.

A market that has been disappointed many times before remains cautious.

That caution was evident on Thursday. Prices fell, but only modestly. Traders were not fully convinced.

The ceasefire discussions between Israel and Lebanon face similar challenges. While the announcement itself is significant, Hezbollah is under no obligation to comply. If rocket attacks continue, Israel is likely to respond, and the ceasefire could unravel almost immediately.

In the Middle East, everything ultimately depends on what Hezbollah decides to do next—and nobody knows the answer.

The Technical Picture: What the Charts Say

Stepping away from geopolitics, the technical outlook offers its own insights.

Brent reached a weekly high of $97.80 before pulling back. Resistance lies near $98.50. A breakout above that level could open the way toward the psychologically important $100 mark. Support sits around $95, with a move below potentially leading to a test of $93.

WTI is showing a similar pattern. This week’s high stands at $96.10. Resistance is near $97, while support is around $94.

Daily technical indicators suggest overbought conditions following the recent rally. That is entirely normal after three consecutive days of gains. Profit-taking is a healthy market response.

Importantly, overbought conditions do not automatically signal a trend reversal. In a strong uptrend, markets can remain overbought for weeks.

Trading volumes on Thursday were below average. Asian markets were active but lacked conviction. Most participants are waiting for the U.S. session, where liquidity and activity tend to be stronger.

What Comes Next: Three Scenarios

Bullish Scenario for Oil

Middle Eastern tensions continue to escalate. The Israel-Lebanon ceasefire collapses. Iran rejects Trump’s nuclear claims. In this case, geopolitical risk premiums return to the market, pushing Brent toward $100 and potentially beyond. By summer, prices could reach $105–110. Falling U.S. inventories would add further support.

Bearish Scenario

Diplomacy succeeds. Iran and the United States reach a nuclear agreement. Hezbollah halts attacks. Israel withdraws from Lebanon. The Strait of Hormuz becomes more secure. In this environment, geopolitical premiums disappear and oil could fall back to $85–90. Additional Iranian supply would reinforce the downward pressure.

Base Case

The conflict smolders but does not spiral out of control. Diplomacy makes little progress. U.S. inventories continue declining due to strong exports. Summer demand provides support. Under this scenario, oil remains largely range-bound between $95 and $100 through the end of summer, with periodic spikes on escalation headlines and pullbacks on diplomatic news.

Which outcome appears most likely?

Probably the middle one.

The Middle East is too complex for quick solutions. Iran is unlikely to abandon its nuclear ambitions overnight. Hezbollah will not disarm simply because Washington wants it to. Yet no major player appears eager for a full-scale regional war.

That leaves a familiar pattern: tension, negotiations, occasional flare-ups—and oil trading within a range.

Thursday offered the market a breather. Whether it proves brief or marks the start of a longer consolidation remains to be seen.

Oil markets are rarely predictable.

That is precisely what makes them so fascinating.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.