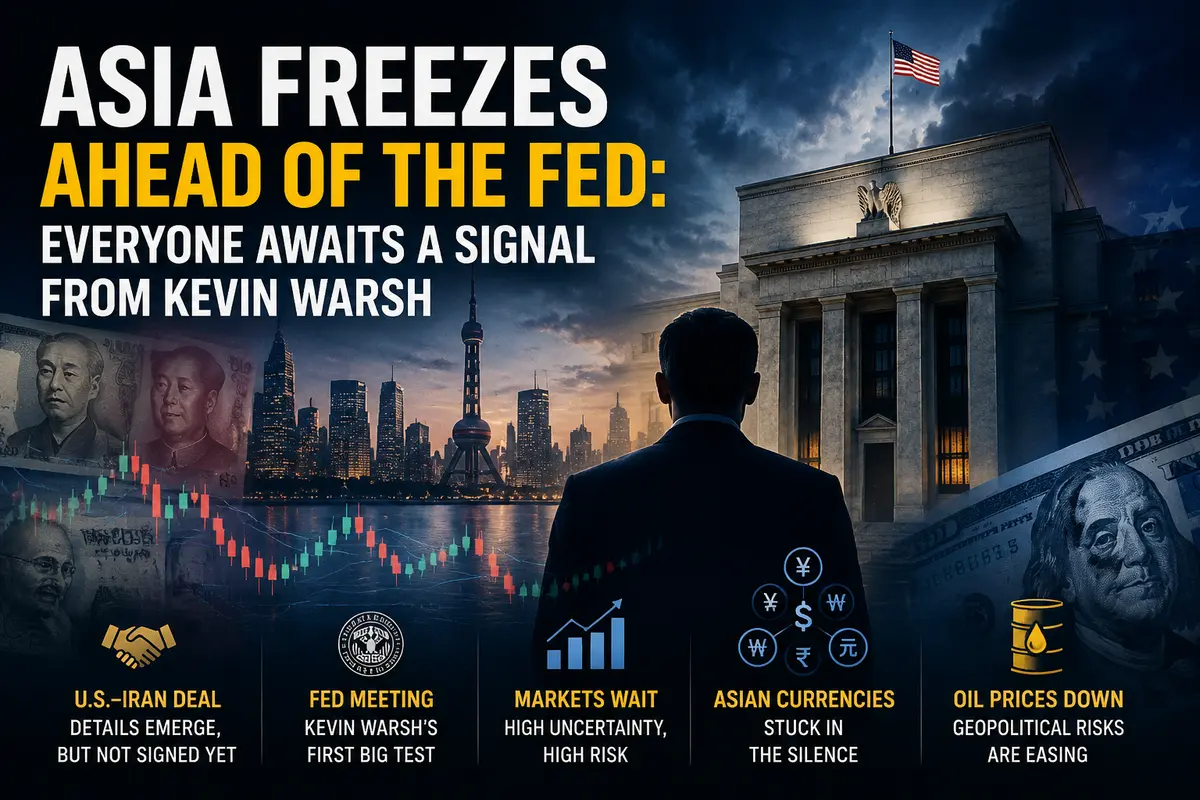

Asia freezes ahead of the Fed: everyone awaits a signal from Kevin Warsh

Wednesday in Asian currency markets began with an oppressive calm. Asian currencies did not move. The dollar did not move. The dollar index (DXY) remained frozen after four days of decline. Everyone stood still. Like rabbits before a predator. Or like traders ahead of the most important event of the week — the meeting of the U.S. Federal Reserve, the first under new Chairman Kevin Warsh.

USD/JPY — the Japanese yen — fell by 0.1% to 160.30. It was a symbolic move. Even after the Bank of Japan raised its rate to 1.0% the previous day — the highest in 31 years — the yen did not strengthen. Because everyone is waiting for the Fed.

USD/CNY — the Chinese yuan — was unchanged. USD/SGD — the Singapore dollar — was unchanged. USD/INR — the Indian rupee — fell by 0.3%, but this was a local move. AUD/USD — the Australian dollar — was unchanged after the RBA kept rates steady.

Only USD/KRW — the South Korean won — rose by 0.4%, breaking away from the general trend. But even this was likely linked to a tech rally in Samsung and SK Hynix shares rather than currency policy.

The reason for the calm is anticipation. Traders do not want to open new positions ahead of the Fed meeting. Uncertainty is too high. The risks are too large.

There is also the peace agreement between the U.S. and Iran. Details are becoming clearer. On Tuesday, the first concrete terms emerged. The agreement provides for the immediate resumption of Iranian oil exports. Iran agrees not to develop nuclear weapons and freezes its nuclear program for 60 days for negotiations.

This is positive for markets. But traders want to see a signed document, not just words. So they wait.

So what is happening in...