Rupee Under the Oil Press: Why ING Doesn’t Expect a Meltdown

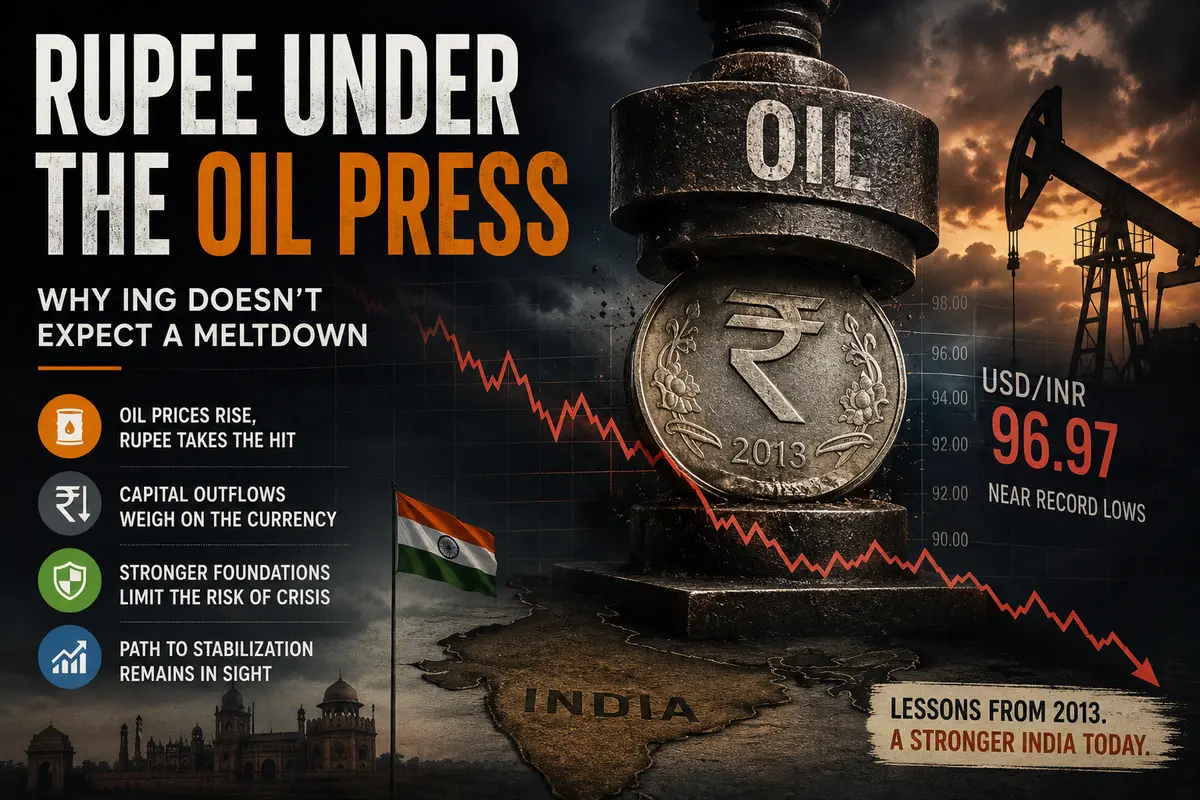

In recent weeks, the Indian rupee has looked like a punching bag—hitting seven consecutive record lows, slipping close to 97 per dollar, and triggering waves of panic headlines in the local press. But if we step back from the day-to-day volatility and look at the broader picture, a more nuanced—and surprisingly less alarming—reality emerges.

ING analysts have examined the rupee’s situation under a microscope and reached a clear conclusion: yes, the currency is likely to remain under pressure as long as oil prices stay elevated. However, the risk of a disorderly collapse—the kind that forces central banks into emergency rate hikes and sends the IMF scrambling to prepare rescue packages—appears limited. India has come a long way since 2013 and now stands on a much stronger foundation.

Oil Shock: Why It Hurts Less Than Before

Back in 2013, when the Federal Reserve merely hinted at reducing monetary stimulus, the rupee plunged and India found itself on the brink of a balance-of-payments crisis. At the time, the current account deficit had reached nearly 5% of GDP, foreign exchange reserves were thin, and the country’s dependence on oil imports seemed like a structural vulnerability.

Today, the picture is very different. ING expects India’s current account deficit to widen to around 2.1% of GDP in 2026. For comparison, it was roughly 0.5% last year. The increase is driven almost entirely by higher oil prices. India still imports more than 80% of the crude oil it consumes, and when oil becomes more expensive, the import bill inevitably swells.

But a deficit of just over 2% of GDP is not the same as 5%. It remains a manageable level that does not threaten macroeconomic stability. Why? Because India has diversified its sources of energy supply. Whereas the country once depended heavily on a small group of Middle Eastern exporters, its import geography is now far broader. This does not eliminate the price shock—oil is still a globally traded commodity—but it does reduce the risk of physical supply disruptions caused by conflicts in any single region.

The government has also introduced fuel subsidies that cushion the blow for consumers and businesses. Subsidies are a double-edged sword: they increase fiscal deficits, but they also prevent social unrest and support economic activity. ING notes that India has weathered the latest oil shock relatively well. That does not mean conditions are ideal—it simply means catastrophe has been avoided.

The Burden of Adjustment: Why the Rupee Is Absorbing the Shock

Perhaps ING’s most interesting conclusion concerns the mechanism through which India is adjusting to the oil shock.

In the past, the burden largely fell on economic growth and inflation. Expensive oil squeezed consumption, pushed prices higher, and forced the central bank to raise interest rates, slowing the economy even further. Today, according to ING, much of that adjustment burden has shifted to the exchange rate itself.

The rupee has weakened by roughly 6% since the beginning of the Iran-related conflict. This depreciation is not a flaw—it is a feature. It reflects not only the higher oil import bill but, more importantly, insufficient capital inflows. A weaker rupee makes Indian exports more competitive and partially offsets the rising cost of imports. This is the classic exchange-rate adjustment mechanism: rather than breaking the domestic economy, the external shock is absorbed through the currency.

There is, however, a downside. A weaker rupee fuels imported inflation. Goods that India purchases abroad—not just oil, but also electronics, fertilizers, and chemicals—become more expensive. This affects both consumers and businesses.

As a result, the Reserve Bank of India (RBI) faces a difficult dilemma: raise rates to contain inflation and support the rupee, or keep rates lower to sustain economic growth. RBI Governor Sanjay Malhotra has chosen a middle path, relying on both verbal guidance and direct market intervention to stabilize the currency without raising rates. So far, that strategy appears to be working.

The Capital Account: Why Money Is Leaving

ING points to a key issue that often gets overshadowed by oil-related headlines.

The rupee’s weakness is not solely a result of expensive oil. A more significant factor is the shortage of capital inflows. Foreign portfolio investors have been withdrawing money from Indian equities and bonds. Net foreign direct investment (FDI), traditionally considered a more stable source of capital, has also been declining.

The paradox is that gross FDI inflows remain substantial. India continues to attract multinational corporations that build factories, establish technology centers, and expand their local presence. At the same time, however, foreign companies already operating in India are repatriating increasing amounts of profit. They earn money in India and send it back to their home markets. In addition, Indian companies themselves are investing more aggressively overseas, which further increases capital outflows.

The result is a shrinking net inflow of capital.

This is a structural challenge that cannot be solved through currency intervention or interest-rate hikes. It requires improvements in the investment climate, more predictable regulation, and continued infrastructure development. It is a long-term issue, and ING does not expect a quick fix.

Light at the End of the Tunnel: Why the Rupee Could Stabilize

Despite the challenges, ING sees several factors that could help stabilize the rupee.

The first is debt capital inflows. Analysts expect them to improve gradually thanks to stable fiscal conditions and moderating inflation. Indian government bonds have been added to major global bond indices, attracting passive investors who must purchase them regardless of short-term market sentiment.

The second factor is intervention by the Reserve Bank of India. The RBI has been selling dollars from its reserves to smooth exchange-rate fluctuations. Reserves are finite, of course, but for now they remain large enough to prevent panic.

The third factor is the sharp decline in the rupee’s real effective exchange rate. Put simply, after adjusting for inflation, the rupee has become significantly cheaper. This makes Indian goods and services more competitive globally and should eventually support exports and foreign-currency inflows.

ING forecasts USD/INR at 95.50 by the end of 2026. That is below current levels near 96–97, implying some appreciation of the rupee. However, analysts stress that risks are skewed toward gradual stabilization rather than a sharp recovery. Few expect the rupee to return to the levels seen at the beginning of the year. More likely, it will find a new equilibrium at a weaker—but sustainable—level.

Lessons from 2013: Why Panic Is Premature

Whenever the rupee falls, memories of 2013 inevitably resurface—the year of the “taper tantrum,” when a single statement from the Federal Reserve sent emerging-market currencies tumbling.

But ING argues that today’s environment is fundamentally different. The current account deficit is much smaller. Foreign-exchange reserves are significantly larger. Inflation, while pushed higher by oil prices, remains under control. The banking sector is healthier. Fiscal discipline, though far from perfect, is stronger than it was a decade ago.

The rupee is likely to remain under pressure as long as oil prices stay elevated. That is an unavoidable reality. Yet ING does not expect the kind of disorderly collapse that would require emergency policy measures. India’s economy is adapting to the shock—through the exchange rate, through subsidies, and through diversified supply chains. The adjustment is not painless, but it is manageable.

For investors and market observers, this means that panic-driven headlines about the rupee’s “record lows” tell only half the story. The other half is the story of a country that is learning to live with expensive oil and has built enough buffers to weather the storm without a crisis.

The rupee has weakened, but it has not broken. And if ING is right, it may find its floor sooner than many expect.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.