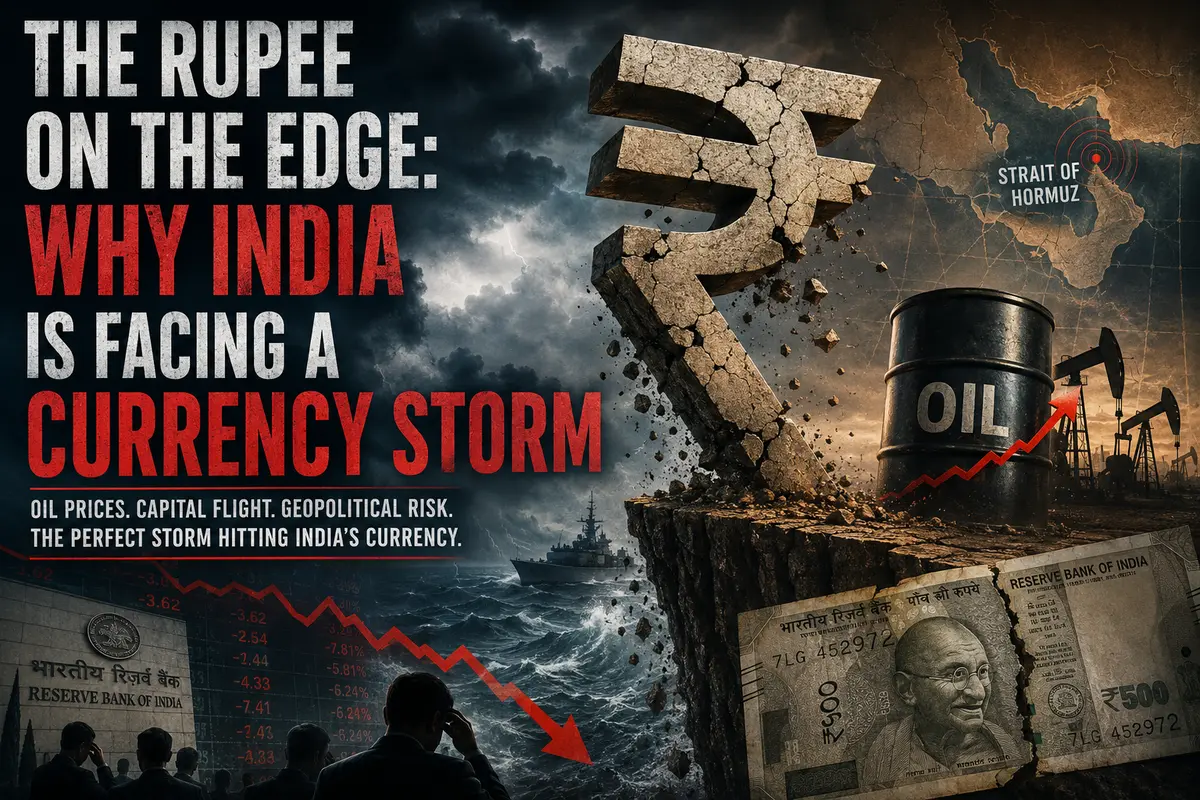

The Rupee on the Edge: Why India Is Facing a Currency Storm

The 96.8650 level that USD/INR pierced this week is not just another number flashing across traders’ screens. It is a diagnosis. Seven consecutive all-time highs are not how healthy markets behave during temporary stress — this is how a system behaves when some fundamental safeguard has broken down. The rupee has fallen before; there have been crashes and speculative panics. But the current situation stands out for its relentless, almost hopeless consistency. The currency is not merely weakening — it is losing the ability to find a bottom. And while the world watches the standoff in the Strait of Hormuz with fascination, the real drama is unfolding not on the decks of destroyers, but in the corridors of the Reserve Bank of India and on the balance sheets of Indian importers staring in horror at their dollar-denominated invoices.

The Oil Trap: Anatomy of a Curse

The entire structure of the Indian economy resembles a building erected on barrels of crude oil. This is neither exaggeration nor literary metaphor. India is the world’s third-largest oil consumer, yet unlike the other members of this uneasy top three, it possesses very little domestic production. More than 80% of the oil the country consumes is imported, sending foreign currency flowing to Saudi Arabia, Iraq, and — in less tense times — Iran.

When oil trades around seventy dollars a barrel, this structure can still maintain balance. But when prices surge by more than fifty percent in just a few months, as they have since late February, the current account begins to crack under the pressure.

The mechanics of this destruction are simple and ruthless. Indian refiners now require far more dollars to pay for the same physical volume of imports. They enter the foreign exchange market and aggressively sell rupees to buy U.S. currency. The scale of these transactions is so enormous that they alone can move the exchange rate.

The rupee weakens, but therein lies the cruel irony: a weaker rupee makes every subsequent oil purchase even more expensive in local currency terms. A vicious circle emerges in which currency depreciation fuels cost inflation, while inflation itself demands even larger amounts of rupees to acquire the same quantity of dollars. This is a classic inflationary spiral triggered not by domestic demand, but by an external supply shock.

The Specter of War in the Strait

Geography, in this case, plays the role of fate itself. The Strait of Hormuz is the narrow bottleneck through which a substantial share of Middle Eastern oil reaches India’s refineries. The confrontation between the United States and Iran has transformed these waters into a permanent zone of military risk.

The market’s reaction is entirely rational, no matter how many diplomatic statements promise “progress” in negotiations. Traders remember perfectly well the episodes involving Iranian speedboats, drones, and mysterious attacks on tankers during previous rounds of escalation. Any spark in the region is instantly priced into shipping insurance premiums.

A tanker sailing through potentially hostile waters costs more to insure and charter. That additional cost becomes embedded in every barrel India imports. Washington may speak endlessly about diplomatic breakthroughs, but as long as ship captains see warships on radar screens and insurers classify the risks as critical, the Indian rupee will continue paying this geopolitical war tax.

Capital Flight: Voting With Their Feet

The oil shock alone would already be severe. But it has collided with another development that makes the situation in Mumbai and Delhi feel almost hopeless: a massive flight of foreign capital.

When officials say that between $22 and $25 billion have exited local equities and bonds since late February, those dry numbers conceal a genuine financial drama. Imagine major international funds, pension managers, and sovereign investors all liquidating positions simultaneously. This is not merely selling — it is an exodus.

The reason behind this exodus lies in a global reassessment of risk. World bond markets are undergoing a brutal repricing: yields on U.S. Treasuries — considered the benchmark risk-free asset — have surged to multi-year highs.

When the safest instrument in the world suddenly offers significantly higher returns, global investors rapidly lose their appetite for risk. Why hold Indian assets — potentially profitable, but exposed to currency volatility, geopolitical instability, and inflation — when one can earn attractive returns in dollars simply by buying Treasuries?

The calculation is ruthless and rational. Investors take their dollars and leave, abandoning behind them a drained stock market and even greater pressure on the rupee.

The Domino Effect in the Domestic Economy

The departure of foreign investors triggers a chain reaction inside the country itself. A falling stock market erodes household wealth and weakens consumption. Bond prices decline, increasing borrowing costs for both the Indian government and corporations.

Companies accustomed to borrowing abroad suddenly discover that servicing foreign-currency debt at nearly ninety-seven rupees per dollar becomes almost unbearable.

The Reserve Bank of India finds itself trapped in the classic dilemma that currency crises impose on emerging-market central banks.

It can attempt to defend the exchange rate by burning through foreign exchange reserves in interventions. But reserves — no matter how large — are finite, while pressure from oil imports and capital outflows appears endless. Spending reserves merely to allow foreign investors to exit at favorable rates is a strategy that often leads to an even greater catastrophe later, once the reserves are depleted.

Alternatively, the central bank can raise interest rates to make rupee assets more attractive and stem capital flight. But that would suffocate an economy already struggling with inflation, make borrowing prohibitively expensive, and sharply slow GDP growth.

Every available option is painful.

The Rupee as a Mirror of Global Tectonic Shifts

The rupee’s roughly six-percent decline since the conflict began has placed it among Asia’s weakest currencies — an unenviable distinction.

Yet on a deeper level, the rupee’s crisis is less a story about India’s weakness than about the dollar’s overwhelming strength during periods of global turbulence. Whenever the world enters storm conditions, capital flees toward safe harbor. And whether one likes it or not, that harbor remains the U.S. dollar.

India simply happened to be one of the first boats to take on water.

The approach toward the ninety-seven mark is symbolic, but one hundred is already visible on the horizon. If tensions in the Strait of Hormuz persist, if oil remains at current levels or rises further, the psychological barrier will likely break as easily as previous historic highs did.

At that point, a far more dangerous phase may begin — one in which economic slowdown is accompanied by panic dollar-buying by the population itself.

That will be the true moment of reckoning for the Indian economy.

For now, the rupee continues falling into the abyss, and each new step downward feels more frightening than the last — because no bottom is visible at all.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.