The Collapse of a Sneaker Empire: How Topsports Lost Nike and Half a Billion in Market Value in a Single Day

The Plunge That Shook the Hong Kong Stock Exchange

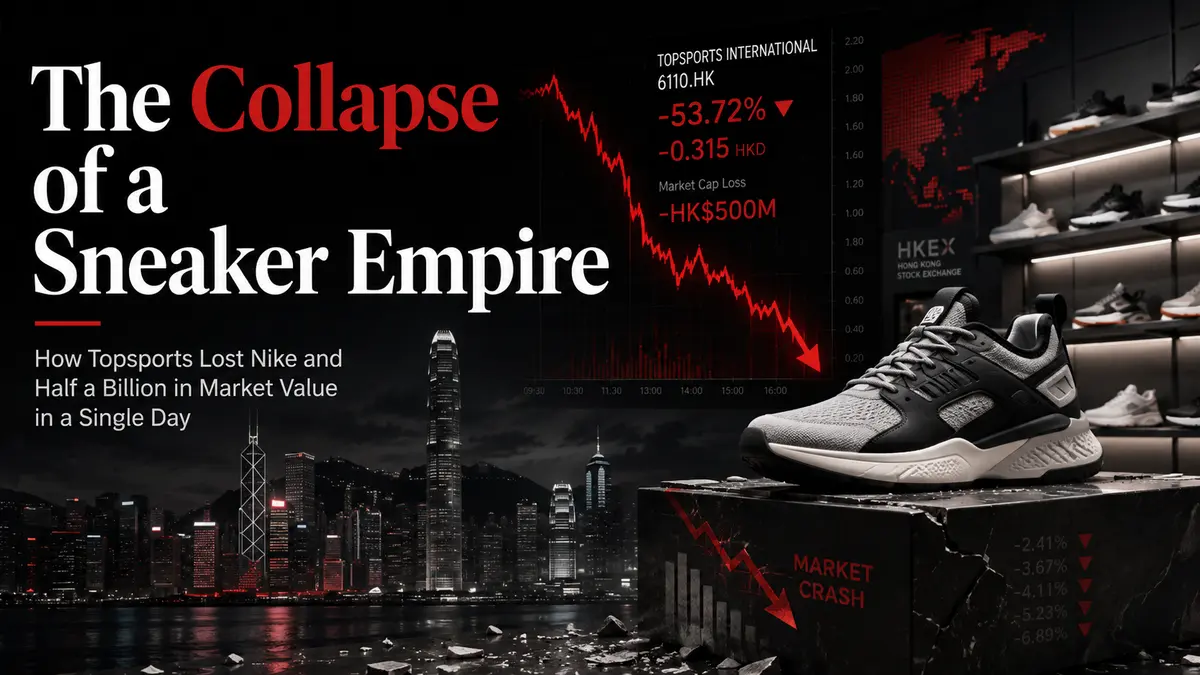

When trading opened in Hong Kong on 22.07.2026 Wednesday morning, no one expected such a nightmare. Shares of TPSRF ... International, one of China’s largest sportswear retailers, plunged 26.2% almost instantly, reaching an all-time low of HKDUSD ... HK$1.41.

This was not merely a market correction. It was a collapse that wiped out nearly a quarter of the company’s market capitalization within minutes. By the time the figures were recorded, the shares had recovered slightly but were still deeply in negative territory, down approximately 23.6% at HK$1.46. Traders stared at their screens in disbelief, repeatedly checking the data and wondering whether what they were seeing was real.

The reason for the collapse was as sudden as a lightning strike and as destructive as a tsunami. The previous evening, after the main trading session had closed, Topsports received an official notice from American sportswear giant NKE ... . Beginning on January 1, 2027, their long-standing partnership covering online sales in mainland China would be terminated completely.

Nike—the iconic Swoosh brand that had supported Topsports’ business for many years—had decided to sever its digital relationship with the retailer. A decision made quietly in corporate offices at Nike’s Oregon headquarters triggered a financial earthquake thousands of miles away in Hong Kong.

To understand the scale of the problem, online sales of Nike products accounted for approximately 22% of Topsports’ total revenue in the financial year that ended on February 28, 2026. This was not a small slice of the pie. It represented almost a quarter of the entire business.

Imagine that your primary supplier, responsible for nearly one in every four of your customers, suddenly tells you: “Starting next year, we will no longer work together in the same way.” News like that can destroy almost any...