US Session Weekly | 6–10 July 2026 Dow Jones at Record Highs as Oil Slides on Hormuz Reopening, Gold Rebounds on Soft Jobs Data, and Bitcoin Claws Back From Extreme Fear

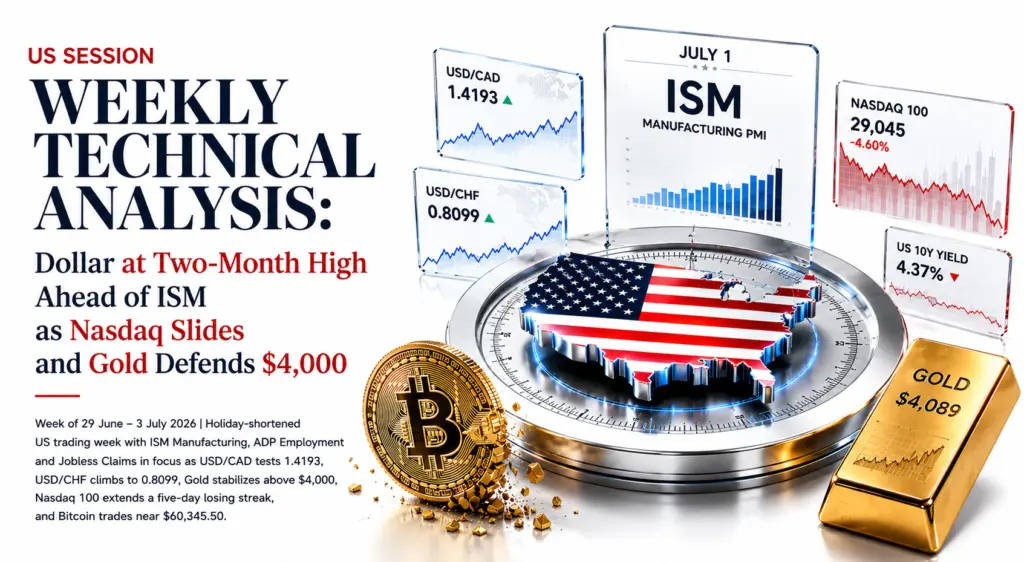

USD/CAD 1.4200 (7-month high range). USD/CHF 0.8032 (off 1-yr high 0.8139). Gold $4,174.71 (+2.3%) off $3,972 8-month low. WTI $68.73 (−3.6%) lowest since Feb. Dow record 52,900. US 10Y 4.48% (+6bps). BTC $62,641.86 (+7%) off June’s worst monthly close in 4 years. XRP $1.131 (+8%). FOMC minutes Wednesday.

LEVEL

HEADING INTO THE WEEK

USD/CAD

1.4200

USD/CHF

0.8032

Gold XAU

$4,174.71

WTI Crude

$68.73

Dow Jones

52,900.00

US 10Y Yield

4.48%

Bitcoin BTC

$62,641.86

XRP

$1.131

The holiday-shortened week of 29 June to 3 July turned on a single pivot: Thursday's 57,000 NFP print against a roughly 115,000 forecast, with 74,000 in downward revisions to prior months, cut September Fed hike odds from roughly 64 to 67% to roughly 50%. That data landed against the backdrop of a genuinely hawkish-leaning Fed hold earlier in June, and Warsh's Sintra remark that inflation expectations have come down gave markets room to price a more balanced outlook. The Dow closed at a fresh record 52,900.00, up 2% as capital rotated into blue-chip industrials while AI-linked semiconductor names -- Micron, Applied Materials, AMD, Sandisk -- sold off sharply on valuation concerns. Gold rebounded from an eight-month low as fading hike bets restored its appeal. WTI fell to its lowest since February as Hormuz flows normalised. Bitcoin rebounded 7% off June's worst monthly close in four years. XRP reclaimed $1.10 on a $281 million short squeeze. Wednesday's FOMC minutes are the week's tie-breaker.

FOMC Minutes Wednesday: The Week’s Single Most Important Release

The US 10-year yield at 4.48%, the Dow's record run, gold's rebound, and the broad-dollar bid behind USD/CAD's seven-month high are all suspended between two competing signals. The Fed's June hold left roughly half of FOMC members projecting at least one more 2026 hike...