Oil Plunges 4%: Peace With Iran Sends Prices Tumbling, But It’s Too Early to Celebrate

Monday: A Day of Major Relief

On Monday morning, when Asian traders returned to their desks after the weekend, they saw what many had been waiting for since the start of the year. Oil prices collapsed. Not a minor correction, not a half-percent decline—but a genuine plunge.

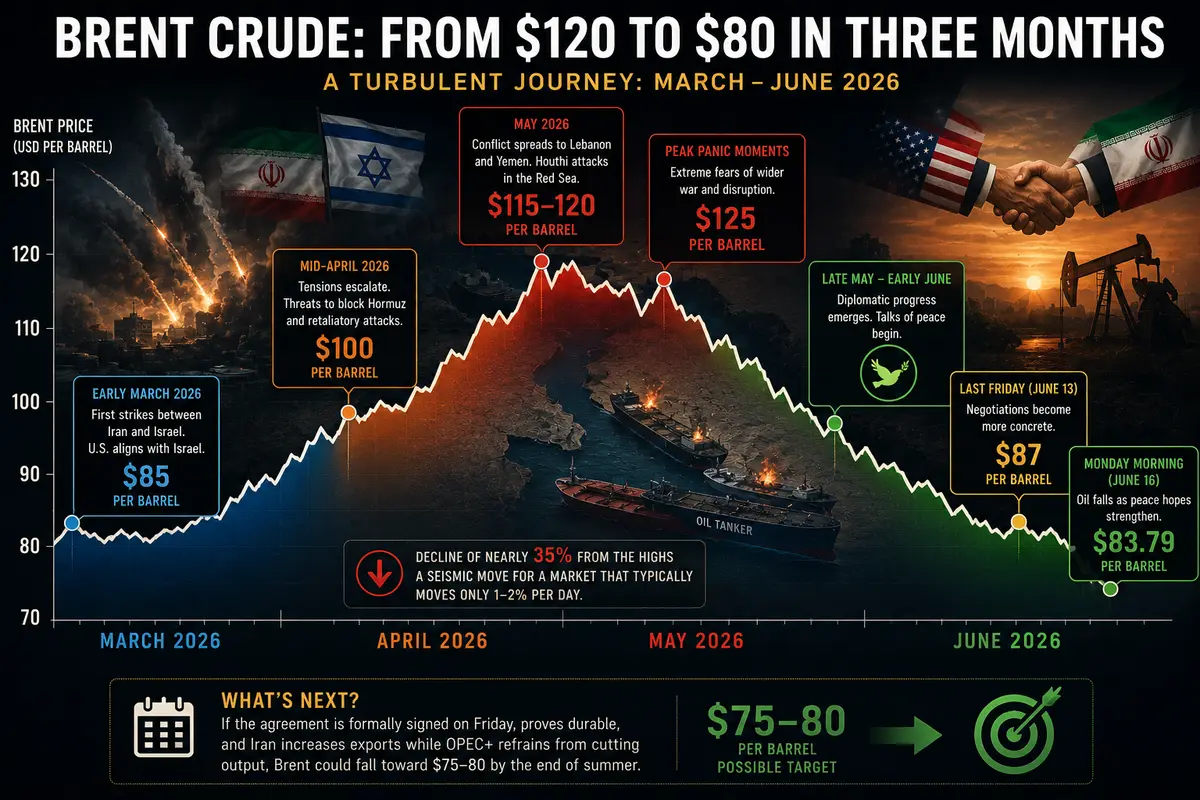

Brent crude futures fell 4.1% to $83.79 per barrel, while WTI dropped 4.6% to $80.95. Both benchmark grades hit their lowest levels since March 10. These are the lowest oil prices seen in three months.

The reason? Peace. Real, long-awaited, almost unbelievable peace between the United States and Iran.

On Sunday, President Donald Trump and Iranian officials issued a joint statement announcing a framework agreement to end hostilities and restore shipping through the Strait of Hormuz.

This is not merely another ceasefire—several of which have been reached and broken over recent months. It is a framework agreement designed as the foundation for a long-term peace settlement. The deal includes a ceasefire, the lifting of the U.S. blockade on Iran, restrictions on nuclear activities, and—most importantly for the oil market—the normalization of Iranian oil exports and the unrestricted passage of tankers through the Strait of Hormuz.

Trump, characteristically enthusiastic, posted on social media:

“Ships of peace, start your engines. Let the oil flow!”

And flow it did. Or rather, the price of oil fell sharply.

But let’s take a closer look at what is really driving this decline, how sustainable it may be, and what comes next.

The Strait of Hormuz Reopens: The Biggest Risk Has Been Removed

For oil markets, the Strait of Hormuz is far more than a narrow waterway between Oman and Iran. It is the Achilles’ heel of the global economy.

Roughly one-fifth of the world’s oil and fuel consumption passes through the strait—between 17 and 20 million barrels every day. Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar all ship oil through Hormuz.

Iran, located along the northern shore, possesses unique capabilities to disrupt traffic through speedboats, missiles, and naval mines. The threat of a blockade has loomed over markets since the conflict began in March.

Now that threat has been removed.

The agreement provides for the restoration of shipping. Tankers can move freely again. Insurance premiums—which surged during the crisis, with some tanker companies refusing to enter the Persian Gulf altogether—are expected to decline. Supply chains should gradually normalize.

Markets reacted immediately.

Brent crude, which traded above $120 during the height of the crisis and briefly touched $125 in April, now sits around $83—a decline of roughly 35% from its peak.

For comparison, following the 2019 attacks on Saudi oil facilities, oil prices surged 20% in a single day before quickly retreating. Today, we are witnessing the opposite phenomenon: a rapid decline as geopolitical risk premiums evaporate.

At $83.79 per barrel, Brent is back near levels seen before the conflict escalated. Most producers remain profitable at these prices. Production costs range from approximately $40–60 per barrel in the United States, $10–20 in Saudi Arabia, and $30–40 in Russia.

However, the extraordinary profits associated with $120 oil are gone.

Iranian Oil Is Returning to the Market

The reopening of Hormuz is not the only factor weighing on prices.

Iran is a major oil producer. Before sanctions, it exported approximately 2.5–3 million barrels per day. Under increasingly strict sanctions during the conflict, exports fell to around 1–1.5 million barrels per day, much of it sold through gray-market channels involving ship-to-ship transfers, falsified documentation, and intermediary traders.

Now sanctions are expected to ease.

Iran will once again be able to sell oil legally. Analysts estimate that within three to six months of sanctions relief, Iranian exports could increase by an additional 1–1.5 million barrels per day.

That represents a significant increase in supply.

Global oil demand is growing only modestly. China’s recovery remains slower than hoped, while Europe continues to stagnate. Against that backdrop, an extra million barrels per day could put substantial downward pressure on prices.

There are, of course, challenges. Iran’s infrastructure has deteriorated. Some wells were shut down and require time to restart. Tankers previously used for unofficial exports may need upgrades or replacement.

Still, by the end of 2026, Iranian oil could return to global markets at full capacity.

The Numbers: From $120 to $80 in Three Months

To understand the scale of the move, it’s worth recalling how the situation evolved.

In early March 2026, when Iran and Israel exchanged their first strikes and the United States aligned itself with Israel, Brent traded around $85 per barrel.

As tensions escalated—with strikes on Iranian facilities, threats to block Hormuz, and retaliatory attacks—prices climbed steadily.

-

Mid-April: Brent reached $100.

-

May: As the conflict spread to Lebanon and Yemen and Houthi forces began attacking tankers in the Red Sea, Brent surged to $115–120.

-

Peak panic moments: Prices briefly touched $125.

Then diplomatic progress began to emerge in late May and early June.

Trump started discussing the possibility of peace. Prices eased from $110 to $100, then to $90.

Last Friday, as negotiations became more concrete, Brent settled around $87.

By Monday morning, it had fallen to $83.79.

A decline of nearly 35% from the highs is seismic for a market that typically moves only 1–2% per day.

And $83.79 may not be the bottom.

If the agreement is formally signed on Friday, proves durable, and Iran succeeds in ramping up exports while OPEC+ refrains from offsetting the increase through production cuts, Brent could fall toward $75–80 by the end of summer.

Trump’s Message: “Let the Oil Flow!”

Trump’s social media statement deserves special attention.

His remark—

“Ships of peace, start your engines. Let the oil flow!”

—is classic Trump: dramatic, simple, and memorable.

The phrase adds little factual information, but it serves as a powerful signal.

Only weeks ago, Trump was promising “total victory” over Iran. More recently, he was authorizing additional strikes. Now he is publicly celebrating peace and tying his political future to its success.

Markets notice such signals.

If Trump has invested significant political capital in the deal, he will likely work to keep it alive—pressuring Iran, Israel, Saudi Arabia, and other regional players to prevent a collapse of negotiations.

And for oil markets, “let the oil flow” has a very literal meaning:

More supply equals lower prices.

Market Reaction Extends Beyond Oil

The decline in oil prices affected a wide range of assets.

Shares of major oil companies—including Exxon, Chevron, Shell, BP, and Lukoil (where traded)—fell between 2% and 4% in pre-market trading.

The Russian ruble, heavily linked to oil prices, weakened. Other commodity-linked currencies, including the Canadian dollar, Australian dollar, and Norwegian krone, also came under pressure.

Meanwhile, airline stocks, logistics companies, and retailers gained.

Cheaper jet fuel lowers costs for airlines. Lower gasoline prices increase consumers’ disposable income, allowing them to spend more elsewhere.

Gold, somewhat surprisingly, also rose.

The connection is indirect:

Lower oil prices → lower inflation expectations → a more accommodative Federal Reserve → a weaker dollar → stronger gold prices.

What Will OPEC+ Do?

Attention now turns to producers.

Over the past two years, OPEC+ has repeatedly reduced output to support prices. Most recently, in April, the group approved a modest production increase, largely symbolic in nature.

What happens if oil remains near $80?

OPEC+ will likely consider production cuts.

Saudi Arabia, the cartel’s de facto leader, generally prefers prices in the $80–90 range. Around $80 is considered the lower boundary of its comfort zone. If Brent falls below $75, Riyadh will likely push for additional reductions.

There is, however, a complication.

Iran’s returning production could offset those efforts.

Although Iran is a founding member of OPEC, it does not participate in the voluntary OPEC+ production-cut framework. Tehran is expected to increase output regardless of what other producers do.

The United States presents another challenge.

As the world’s largest oil producer, U.S. shale operators do not coordinate with OPEC+. Most shale projects remain profitable at $80 oil, though prices near $70 could force some companies to scale back drilling activity.

A new equilibrium will eventually emerge.

The only question is where.

Risks Remain: Peace Has Not Yet Been Signed

Despite Monday’s optimism, analysts caution against excessive enthusiasm.

A framework agreement is not a signed peace treaty.

The formal signing ceremony in Switzerland is still several days away, and a great deal can happen in the meantime.

Iranian hardliners may attempt to derail the deal. Israel—which is not a direct participant in the negotiations but has suffered heavily from the conflict—could launch preventive military actions. The United States could harden its position at the last moment.

Even after a formal signing, implementation will take time.

The Strait of Hormuz will not instantly return to normal operations. Tankers will not immediately flood through the passage until any security concerns are resolved, insurers reduce premiums, and shipping contracts are restored.

Analysts also note that other regional conflicts remain unresolved.

Houthi attacks in the Red Sea continue. The ceasefire between Israel and Hezbollah in Lebanon remains fragile. Iran could still exert pressure through proxy groups without technically violating its agreement with Washington.

Central Bank Week: The Fed, Bank of Japan, and Bank of England

Beyond geopolitics, investors will focus on several major central-bank meetings this week.

These decisions could affect the U.S. dollar—and, by extension, oil prices.

The Federal Reserve meets on June 16–17. Rates are widely expected to remain unchanged, but investors will closely examine the updated economic projections and Jerome Powell’s comments.

A dovish Fed could weaken the dollar and provide some support for oil. A more hawkish tone could strengthen the dollar and add further pressure to prices.

The Bank of Japan is expected to raise rates to 1%, marking a significant shift after years of ultra-loose monetary policy. A stronger yen would generally weaken the dollar, potentially supporting commodity prices.

The Bank of England is expected to leave rates unchanged amid weak economic growth.

Their influence on oil will be indirect, but it could still prove significant.

Conclusion: Peace Is Near, but Caution Is Still Warranted

Oil prices plunged 4% on Monday following news of a peace framework agreement between the United States and Iran.

Brent fell to $83.79 per barrel, while WTI dropped to $80.95, marking their lowest levels since March 10.

The key drivers are the reopening of the Strait of Hormuz and the anticipated return of Iranian oil exports—both of which increase global supply and reduce prices.

Markets are also pricing in lower inflation expectations and the possibility of a more accommodative Federal Reserve.

OPEC+ may attempt to support prices through production cuts, but the effectiveness of such efforts remains uncertain.

Risks persist. The agreement has not yet been formally signed. Implementation will take time. Other conflicts across the Middle East remain unresolved.

Central-bank decisions this week could add another layer of volatility.

But on Monday morning, traders chose optimism.

Cheaper oil is generally good news for the global economy. It means lower inflation, less pressure on central banks, and potentially stronger economic growth.

For now, it remains a story of hope.

And hope, as the saying goes, can sometimes be worth more than oil—even when oil itself is getting cheaper.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.