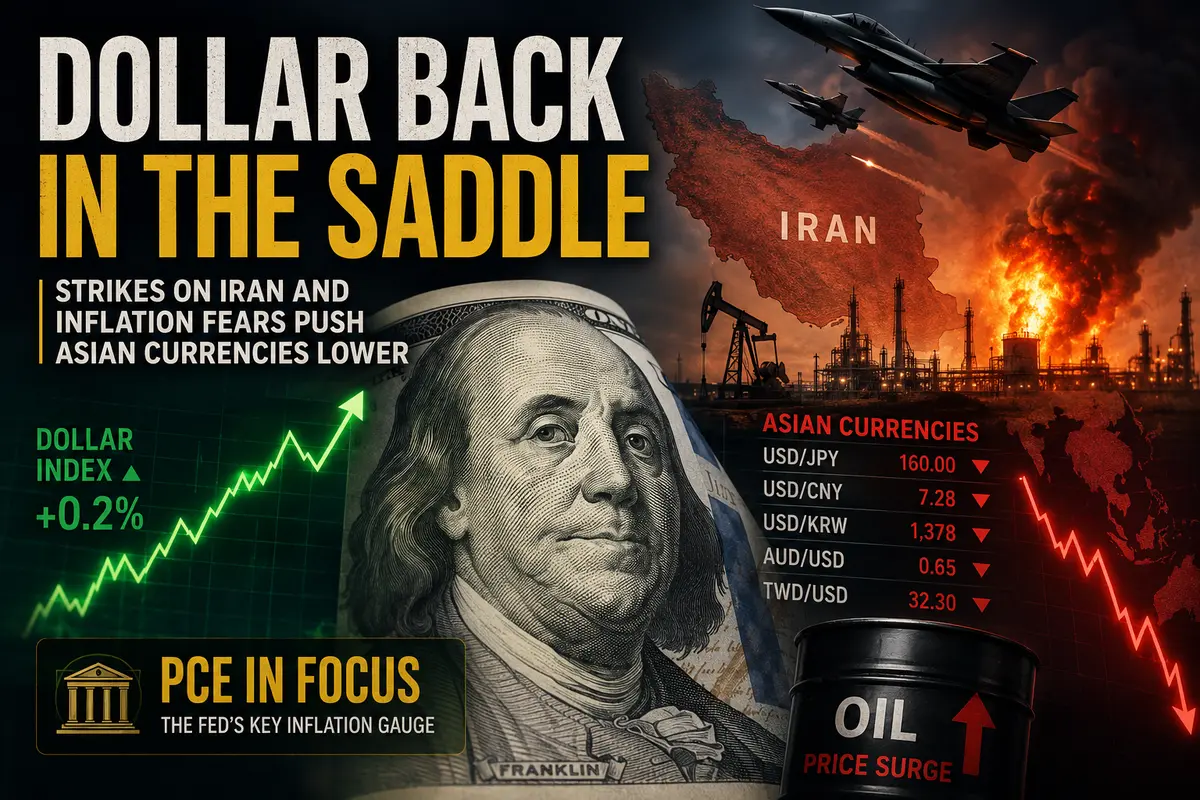

Dollar Back in the Saddle: Strikes on Iran and Inflation Fears Push Asian Currencies Lower

Thursday’s Asian trading session opened with news that, while increasingly familiar in recent weeks, remains deeply unsettling. U.S. armed forces launched another round of strikes on targets in southern Iran — the second such operation in a week. Markets reacted instantly and predictably: a rush into the dollar. The U.S. dollar index edged higher, Asian currencies fell into negative territory, and oil prices surged. All of this is unfolding on the very day the Federal Reserve is set to release its preferred inflation gauge — the PCE index. Thursday is shaping up to be a volatile one.

Second Strike in a Week: Why Bombs Move Currencies

Whenever the U.S. strikes Iranian targets, currency markets tend to follow the same script. The dollar rises, while nearly every other currency weakens. This has little to do with patriotism or confidence in American military power. It is simply cold financial logic.

Conflict involving Iran threatens oil supplies. Disruptions in oil supplies drive energy prices higher. Rising energy costs fuel inflation. Higher inflation, in turn, forces the Federal Reserve to keep interest rates elevated — or even raise them further. And high interest rates make the dollar more attractive to investors searching for yield.

But on Thursday, another element was added to this familiar chain reaction. President Trump personally rejected recent reports suggesting Iran was prepared to reopen the Strait of Hormuz within thirty days. That statement dealt a blow to the fragile optimism that had supported markets over the past few days. Investors who only yesterday hoped for a near-term peace agreement are now being forced to admit that the conflict may drag on. And a prolonged conflict means prolonged inflation. Prolonged inflation means rates staying higher for longer.

Markets have largely abandoned hopes for a quick resolution, and safe-haven capital is pouring into the dollar.

The dollar index and dollar futures both rose by around 0.1–0.2%, once again approaching nearly two-month highs. The move itself may be modest, but the direction is telling. The dollar is reclaiming its throne, and Asian currencies are bowing one after another.

PCE: The Moment of Truth

If Thursday were an ordinary day, markets might have focused solely on developments in Iran. But today is anything but ordinary.

Later in the session, the April PCE Price Index — the Federal Reserve’s preferred inflation measure — will be released. Unlike the more widely known CPI, the PCE index accounts for changes in consumer behavior. When beef prices rise, for example, consumers may switch to chicken, and the PCE captures that substitution effect. In the Fed’s view, this makes it a more accurate gauge of underlying inflation pressure.

Markets are awaiting the data anxiously. Earlier inflation reports released this month already showed a sharp increase in price pressures. If the PCE confirms that trend, expectations for further rate hikes will strengthen, giving the dollar another boost. If, on the other hand, the PCE shows inflation slowing, it could become a surprise catalyst for dollar weakness.

But until the numbers arrive, traders are preparing for the worst — and buying dollars.

Yen Nears the Danger Zone Again

The Japanese yen once again approached the 160-per-dollar level on Thursday. That threshold is the same red line that triggered large-scale currency intervention by the Bank of Japan earlier in May. At the time, Tokyo spent tens of billions of dollars to support the national currency, and for a while, the effort worked.

Now the yen is back near dangerous territory, and markets are increasingly nervous.

Japanese officials have warned they are ready to intervene again. But this time the situation is more complicated. The May interventions took place while hopes for peace with Iran were still alive and oil prices were lower. Now, after the latest strikes and Trump’s remarks, oil is rising again, intensifying pressure on the yen.

The Bank of Japan may soon face a difficult choice: either spend reserves on another round of interventions with uncertain effectiveness, or allow the yen to break through 160 and deal with the consequences — accelerating imported inflation and rising costs for energy and food.

USD/JPY moved only slightly higher on Thursday, but the calm may prove deceptive. Once the 160 level is seriously tested, real turbulence could begin.

Chinese Yuan and Taiwan Dollar: Weakening in Sync

The Chinese yuan and Taiwan dollar moved almost in lockstep on Thursday, both weakening roughly 0.1% against the U.S. dollar. That is no coincidence. Both currencies are suffering from the same pressures: expensive oil, uncertainty surrounding Iran, and a broad flight from risky assets.

But each also faces unique domestic challenges.

The yuan remains near a three-year low, forcing the People’s Bank of China to spend reserves defending the currency. Meanwhile, the Taiwan dollar is being pressured by rising tensions with China and uncertainty over U.S. weapons deliveries.

Both currencies have become hostages to geopolitics, and until the Iranian conflict is resolved, sustained gains will be difficult.

Australian Dollar: The Fear Gauge Slips

The Australian dollar is often viewed as a proxy for global risk appetite. When investors feel optimistic, they buy the Aussie. When fear returns, they sell it.

On Thursday, AUD/USD fell by around 0.3%. This is hardly a collapse, but it is a confident downward move signaling that market anxiety is returning.

Australia’s economy depends heavily on commodity exports, including energy and metals. On one hand, higher oil prices should theoretically support Australian exporters. On the other, prolonged conflict and uncertainty threaten global demand.

Investors are choosing caution, exiting the Aussie and rotating back into the dollar.

South Korean Won: New Governor, Old Problems

The Bank of Korea left interest rates unchanged at 2.5% on Thursday, fully in line with market expectations. The decision itself triggered little immediate reaction.

However, this meeting was significant because it was the first under new Governor Shin Hyun-song. And the tone from the new leadership caught the market’s attention.

Shin is known as a supporter of tighter monetary policy. His arrival coincides with growing inflation concerns driven by expensive oil. Although rates were left unchanged, several policymakers expressed support for a more hawkish stance.

This shift toward tighter policy could mean the Bank of Korea eventually raises rates even if economic growth slows. For the won, that is potentially positive over the longer term. But in the short term, geopolitical pressure continues to dominate.

USD/KRW rose around 0.3% on Thursday.

A Thursday That Could Set the Direction

Thursday in currency markets represents the collision of two powerful forces.

On one side is geopolitics: fresh strikes on Iran, harsh rhetoric from Trump, and fading hopes for a quick peace agreement.

On the other is macroeconomics: the PCE inflation report, which could either confirm inflation fears or unexpectedly ease them.

For now, geopolitics is winning. The dollar is rising, Asian currencies are weakening, and oil prices are climbing.

But after the PCE release, the picture could change quickly. If inflation comes in below expectations, the dollar may retreat and Asian currencies could finally find some relief. If inflation surprises to the upside, pressure will intensify, and talk of additional Fed rate hikes will return with renewed force.

Thursday is far from over — and its final outcome may still surprise the markets. Investors are waiting. And in that anticipation lies the day’s biggest intrigue.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.