The Dollar Loses Ground, the Euro Rebounds — Peace with Iran Reshapes the Market Outlook

Friday: A Day of Diplomatic Optimism

Throughout Thursday and Friday, currency markets remained in a state of nervous anticipation. Not the sticky fear that accompanies missile strikes, but rather a cautious hope — what if? What if the seemingly endless Middle Eastern crisis, which has flared up intermittently for months, is finally approaching its conclusion? What if Trump, known for making bold statements, is telling the truth this time? What if a peace agreement with Iran is actually signed this weekend?

Investors decided that the mere possibility was enough to act. The U.S. dollar, which had strengthened in recent weeks amid geopolitical uncertainty and expectations of further Federal Reserve tightening, gave up some of its gains on Friday. The U.S. Dollar Index (DXY) fell 0.1% during London trading, stabilizing after touching its lowest level of the week. For the week as a whole, the index is down 0.3%. Not a dramatic move, but a symbolic one: the trend has shifted.

The euro, by contrast, regained momentum. EUR/USD hovered near its highest levels of the week and appeared set to post its strongest weekly performance in more than a month. The rally was supported not only by easing geopolitical tensions but also by the European Central Bank’s first interest-rate hike in nearly three years. While the Federal Reserve remains on pause, the ECB has finally taken a step it had been discussing for months.

So what happened? Three key factors are driving the story: Donald Trump’s peace overtures toward Iran, the sharp decline in oil prices triggered by those remarks, and U.S. inflation data that turned out to be less alarming than many had feared.

Trump Hints at an Iran Deal — and Markets Believe Him

The primary catalyst came on Thursday, when Donald Trump suggested that a peace agreement between the United States and Iran could be signed as early as this weekend.

The phrase “historic peace agreement” reportedly entered the conversation. Trump offered few specifics. He did not identify the location, the terms, or the exact signatories. Yet the fact that a U.S. president who only weeks ago was promising “total victory” over Iran and authorizing new strikes against Iranian targets was suddenly talking about peace shocked financial markets.

Their reaction was immediate. The Dollar Index, which had hovered around the 100 level all week, began to decline. Investors started moving out of traditional safe havens such as the dollar, gold, and government bonds and into currencies that tend to benefit from peace and expanding global trade, including the euro, pound sterling, and Australian dollar.

Why is the dollar so sensitive to developments in the Middle East? Because it remains the world’s primary safe-haven currency. When global risks rise, investors buy dollars. When hopes for stability emerge, they rotate into riskier assets. The logic is simple.

The dollar also enjoyed another advantage in recent weeks: relatively high U.S. interest rates. But as we will see, that support may be weakening as well.

Oil Falls to Two-Month Lows

Trump’s comments were followed by a sharp decline in oil prices. Crude fell to its lowest levels in roughly two months. Brent crude, which had recently traded above $95 per barrel, slipped below $92 and briefly touched $91 intraday. WTI crude dropped below $88.

The reason was the same: optimism about peace. If Washington and Tehran reach an agreement, concerns over disruptions in the Strait of Hormuz diminish. Iran’s influence over this critical shipping route, through which roughly one-fifth of the world’s oil supply passes, has long been a source of market anxiety. Reduced geopolitical risk means lower insurance premiums, smoother energy flows, and potentially lower oil prices.

There is another mechanism at work as well. Cheaper oil tends to reduce inflationary pressure. Lower inflation can lead to a more accommodative stance from central banks. Easier monetary policy generally weakens the dollar because investors favor the greenback when interest rates are high.

It is a long chain of causality, but a direct one. As oil prices declined, the dollar followed. Investors who had held dollars as an inflation hedge began unwinding those positions.

There is, however, an important nuance. U.S. producer-price data released on Thursday showed that producer inflation accelerated more than expected in May, largely because of higher energy costs linked to earlier disruptions in Middle Eastern oil supplies. Inflationary pressures have not disappeared; they have merely shifted from consumer prices to producer prices.

PPI Data Sends Mixed Signals to the Fed

Thursday’s Producer Price Index (PPI) report offered a mixed picture for Federal Reserve policymakers.

Headline PPI rose more than economists had expected, driven primarily by energy costs. Elevated oil prices from April and May filtered through to manufacturers, transportation firms, and utilities, all of which faced higher fuel expenses and passed some of those costs along.

However, core PPI — which excludes volatile food and energy prices — increased less than forecast.

This distinction is important. It suggests that underlying inflationary pressures within the U.S. economy may be easing. Expensive oil represents a temporary shock. If energy prices stabilize or decline, core inflation could continue its downward trend.

Markets, which only a week earlier had been pricing in a high probability of another Fed rate hike following strong employment data, adjusted their expectations slightly after the PPI release. The probability of a rate increase later this year fell from around 70% to approximately 65–67%.

The shift was modest, but financial markets often react more to changes in expectations than to absolute numbers.

Investors have also pushed expectations for any additional tightening further into the future. Whereas some analysts had previously considered a September rate hike possible, consensus expectations have shifted toward December or even beyond.

That is not particularly supportive for the dollar. The currency generally performs best when interest rates are rising, not when they are stagnant.

The Euro Has Its Own Story: The ECB

While the dollar weakened due to geopolitical optimism and softer inflation expectations, the euro received support from developments within Europe itself.

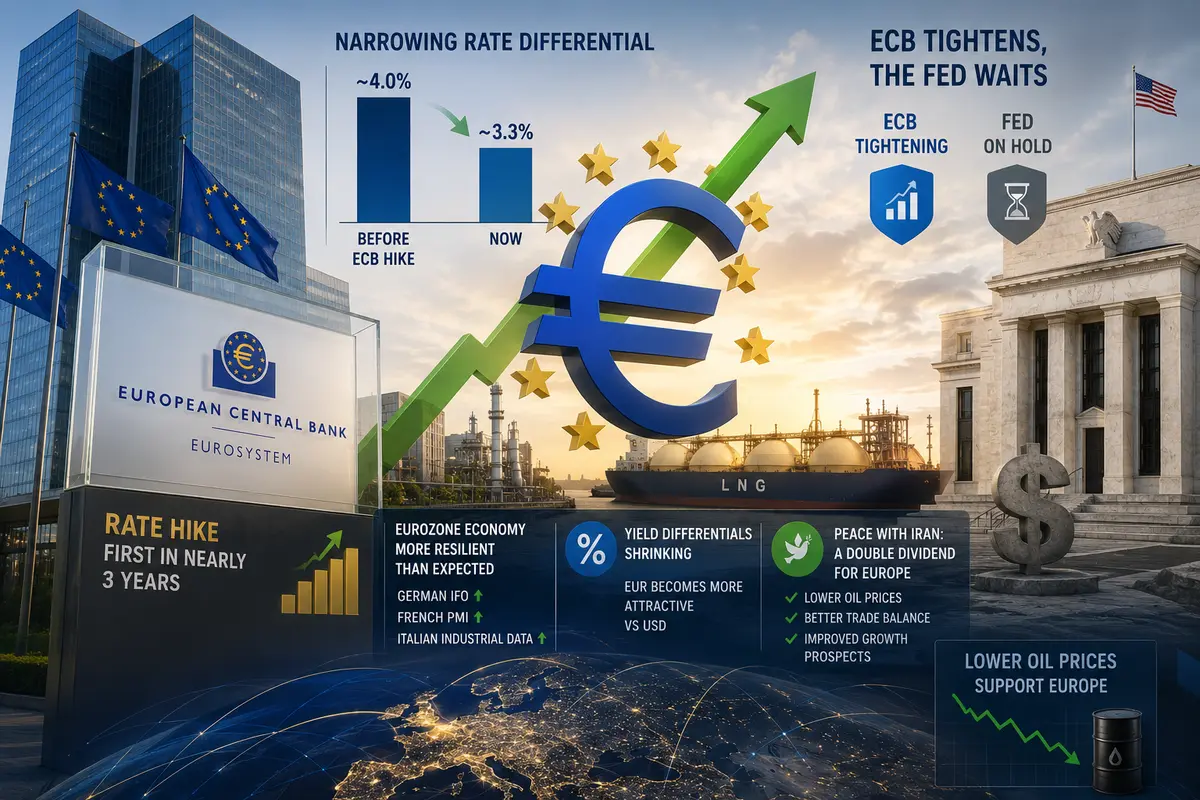

The European Central Bank finally delivered the interest-rate increase it had been signaling for months. It was the first hike in nearly three years.

Although the move was widely expected and largely priced in, the symbolism matters. The ECB is actively tightening policy while the Federal Reserve remains in wait-and-see mode.

The interest-rate differential between the United States and the eurozone is beginning to narrow. Not long ago, the gap approached four percentage points. Now, following the ECB’s move, that difference has shrunk slightly. If the ECB follows through with additional rate increases, as many analysts expect, the gap could narrow further.

As yield differentials shrink, the euro becomes more attractive relative to the dollar.

The eurozone economy, while hardly booming, has also proven more resilient than expected. German Ifo surveys, French PMI readings, and Italian industrial data have all exceeded forecasts. The results are not spectacular, but they are better than anticipated.

Geopolitics may provide an additional advantage. If peace with Iran materializes, Europe stands to benefit more than the United States because of its greater dependence on Middle Eastern energy imports. Lower oil prices improve Europe’s inflation outlook, trade balance, and growth prospects simultaneously.

For Europe, peace could be a double dividend.

What Technical Indicators Suggest

For traders focused on chart analysis, the technical picture is becoming increasingly interesting.

The Dollar Index has broken below support around the 100 level and is currently consolidating near 99.8–99.9. The next significant support area lies around 99.5. A break below that level could open the door toward 99.0 and lower. Resistance remains near 100.2, this week’s high. To re-establish an upward trend, the dollar would need to reclaim that level.

Meanwhile, EUR/USD has broken above resistance at 1.1550 and is trading in the 1.1580–1.1600 range. The next resistance levels are around 1.1620 and then 1.1650. Key support sits near 1.1550, followed by 1.1500.

From a technical perspective, the dollar appears overextended while the euro still has room to appreciate. Fundamentally, however, everything depends on whether an agreement with Iran materializes and how inflation data evolve in the coming weeks.

Sterling, the Australian Dollar, and the Yen

The British pound also strengthened on Friday, though not as dramatically as the euro. The move came despite weak UK GDP data showing a 0.1% contraction in April, the first monthly decline since August.

Ordinarily, weaker growth would be negative for a currency. However, softer economic activity also reduces the likelihood of additional rate hikes from the Bank of England.

Even so, sterling gained roughly 0.5% against the dollar during the week, largely because of broad-based dollar weakness rather than domestic strength.

The Australian dollar, often viewed as a proxy for global risk appetite, also advanced. Australia is a major commodity exporter, and reduced geopolitical tensions support global trade and economic activity.

The Japanese yen was one of the few major currencies that did not benefit significantly from dollar weakness. Like the dollar, the yen is considered a safe haven. Moreover, the Bank of Japan continues to maintain extremely accommodative monetary policy, limiting the yen’s attractiveness for yield-seeking investors.

Risks: What Could Go Wrong?

Of course, this entire wave of optimism could unravel quickly.

If negotiations with Iran collapse, if Trump’s comments prove premature, or if military tensions flare up again over the weekend, the dollar could regain strength while the euro and other risk-sensitive currencies retreat.

A second risk is inflation. Producer-price data suggest that inflationary pressures remain present. If higher producer costs ultimately feed through into consumer prices, the Federal Reserve may have little choice but to tighten policy further, even at the risk of slowing economic growth.

A third risk concerns the ECB itself. If policymakers become too aggressive with rate hikes, they could undermine the eurozone’s fragile recovery, eventually weakening the euro.

Yet as markets headed into the weekend, investors chose to focus on the positive. They watched developments in Washington and Tehran and hoped for the best. The dollar declined. The euro climbed. Oil prices fell. Bonds rallied.

What Comes Next? The Weekend Will Decide

The next few days could prove decisive.

If a genuine peace agreement between the United States and Iran is signed this weekend, markets may extend their moves on Monday. The dollar could fall another 0.5–1%, EUR/USD could advance toward 1.1650–1.1700, and Brent crude could slide toward $88–89 per barrel.

If talks collapse and the announcement turns out to have been little more than political theater, markets could quickly reverse course. The Dollar Index might rebound toward 100.2–100.5, while EUR/USD could retreat toward 1.1500 or lower.

A third possibility is a partial agreement or temporary ceasefire. In that case, markets may hold onto their recent gains without extending them significantly. The dollar could stabilize around 100, while EUR/USD remains in the 1.1550–1.1600 range as traders await further developments.

For now, optimism remains cautious.

Traders have reduced long-dollar positions and covered short-euro positions, but many remain reluctant to make major new bets until the situation becomes clearer.

The weekend promises to be a tense one — at least for currency traders.

A peace deal with Iran could reshape not only currency markets but also broader geopolitical dynamics. Or it could change very little if it proves to be another false start.

We may find out on Monday. Or Tuesday. Or perhaps even this weekend.

Until then, investors will be watching the headlines closely. In the Middle East, even a “historic peace agreement” can sometimes be little more than a pause between conflicts. But occasionally, a pause is enough.

Enough for markets to catch their breath.

And enough for the dollar to step aside, if only temporarily.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.