WTI Crude Oil Futures Rise in Asian Trading

Green Light in the East

Oil traders came into Wednesday with more questions than answers. The previous few weeks had been anything but straightforward. Prices jumped on geopolitical headlines, slipped on weak economic data, then bounced back again when supply concerns resurfaced. Every trading session seemed to bring a new narrative.

But when Asian markets opened on Wednesday, the message was surprisingly clear.

WTI crude futures moved higher almost from the start of trading. The gains were not spectacular, but they were steady and broad-based. By the middle of the session, prices had climbed close to 1%, reaching $94.62 per barrel. In a market that has spent much of the year struggling to find direction, that kind of move attracts attention.

What matters most isn’t the size of the gain. It’s the fact that buyers are once again willing to step in.

Markets rarely move in a straight line. Oil, perhaps more than any other major commodity, is driven by a constant tug-of-war between fear and optimism. On one side are concerns about economic growth, consumer demand, and industrial activity. On the other are supply disruptions, geopolitical risks, and tightening inventories.

This week, the balance appears to be shifting in favor of the bulls.

Adding support was a slightly weaker U.S. dollar. The Dollar Index slipped to around 99.21, a modest decline that would barely register in many markets. For oil, however, currency moves matter. Crude is priced globally in dollars, so when the dollar weakens, oil becomes cheaper for buyers using euros, yen, yuan, or other currencies. That often encourages demand and provides a tailwind for prices.

Brent crude followed the same path. The global benchmark rose to $96.78 per barrel, outperforming WTI by a small margin. The spread between the two contracts widened to roughly $2.16, putting Brent back into its traditional premium position.

For traders, that spread is more than just a number. It’s one of the clearest indicators of how regional supply and demand dynamics are evolving. And right now, it suggests that the market is gradually returning to a more normal structure after months of unusual distortions.

Why Asia Still Matters More Than Many Investors Realize

When people think about oil markets, they often focus on New York, Houston, Riyadh, or Vienna. That’s understandable. The United States remains one of the world’s largest producers and consumers. Saudi Arabia remains the most influential exporter. OPEC continues to shape supply expectations.

Yet every day begins in Asia.

And increasingly, that’s where demand tells the real story.

China remains the world’s largest importer of crude oil. India continues to expand its consumption as its economy grows. Japan and South Korea, despite slower population growth, remain major energy consumers with significant refining industries.

Together, these countries represent an enormous share of global oil demand.

That’s why Asian trading sessions can have an outsized impact on market sentiment. When traders in Singapore, Shanghai, Tokyo, and Mumbai start buying aggressively, the rest of the world notices.

On Wednesday, the buying wasn’t driven by panic or speculation. It looked more like confidence.

Some participants were covering short positions after recent declines. Others were building new long positions in anticipation of stronger demand during the summer months. Institutional investors appeared more willing to add exposure after several weeks of consolidation.

The result was a market that felt healthier than it had in some time.

Volume was solid. Momentum improved. Sellers became less aggressive.

In other words, buyers finally looked comfortable again.

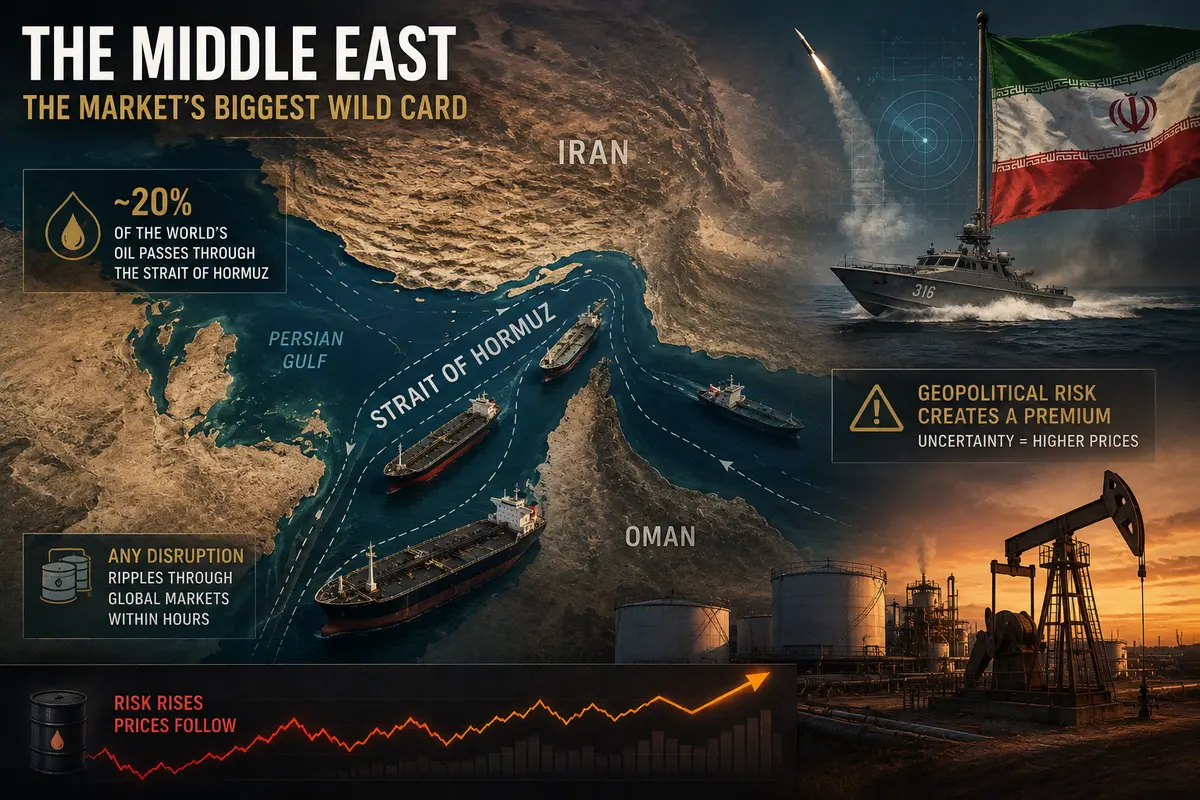

The Middle East Remains the Market’s Biggest Wild Card

Every oil rally eventually leads back to the same question:

What happens next in the Middle East?

The region remains responsible for a substantial share of global oil production and exports. Any disruption there can ripple through the entire energy market within hours.

At the center of current concerns is the Strait of Hormuz.

For anyone unfamiliar with the geography, the strait is one of the most strategically important waterways on the planet. Nearly one-fifth of global oil supplies pass through this narrow corridor connecting the Persian Gulf to international shipping routes.

If traffic through Hormuz were ever seriously disrupted, the consequences for global energy markets would be immediate.

Nobody expects a complete shutdown. The United States and its allies maintain a significant military presence in the region, and global shipping companies have contingency plans in place.

But markets don’t need an actual disruption to react.

The possibility alone is often enough.

Recent reports of Iranian military exercises near the strait reminded traders just how sensitive the region remains. While officials described the drills as routine, investors interpreted them as another sign that tensions could escalate with little warning.

That uncertainty creates what analysts call a geopolitical premium.

Simply put, buyers are willing to pay more for oil when there is a higher risk of supply disruptions. It’s insurance against future problems.

The same logic applies to developments in Yemen, where Houthi attacks against shipping routes and energy infrastructure continue to create concern. Even when physical damage is limited, every incident serves as a reminder that energy supplies remain vulnerable.

And in oil markets, vulnerability usually carries a price tag.

America’s Summer Driving Season Is Arriving

If geopolitics is one side of the equation, demand is the other.

And few seasonal trends are as reliable as America’s summer driving season.

Every year, millions of Americans take to the road between Memorial Day and Labor Day. Families travel across states. Tourists head to beaches, national parks, and major cities. Commercial traffic increases. Fuel consumption rises.

The result is predictable.

Gasoline demand climbs sharply.

Refineries respond by increasing production, which boosts demand for crude oil. Historically, this period has often coincided with stronger energy prices.

There are exceptions, of course. Recessions can weaken demand. Extraordinary events can disrupt travel patterns.

But under normal economic conditions, summer tends to be supportive for oil.

This year appears no different.

Air travel remains strong. Consumer spending has held up better than many economists expected. Employment remains relatively healthy. While growth has slowed compared with previous years, it has not collapsed.

That combination creates a favorable environment for energy demand.

Investors know it.

Traders know it.

And increasingly, oil prices are beginning to reflect it.

Inventories Will Be the Next Major Test

One of the most closely watched data points this week will be U.S. crude inventory figures.

The reason is simple.

Inventory data tells traders whether supply is keeping pace with demand.

When stockpiles fall, it often suggests that consumption is strong or production is insufficient. Both scenarios are generally supportive for prices.

When inventories rise unexpectedly, the opposite is true.

Current forecasts point toward another drawdown in U.S. crude stocks.

If those estimates prove accurate, it would mark another week in a growing pattern of declining inventories.

That would strengthen the bullish argument considerably.

Markets can ignore headlines for a while. They can even overlook geopolitical noise if conditions remain stable.

But inventory data is harder to dismiss.

It’s real.

It’s measurable.

And it often reveals what’s actually happening beneath the surface of the market.

The Technical Picture Is Improving

From a chart perspective, oil bulls have reasons to feel encouraged.

WTI continues to trade comfortably above the major support zone near $86.35 per barrel.

That level has been tested repeatedly over recent weeks.

Every time sellers pushed prices toward it, buyers appeared.

That kind of behavior matters because it establishes confidence. Traders begin to view the area as a floor, a place where demand consistently outweighs supply.

Resistance remains near $96.04 per barrel.

That’s the level everyone is watching.

The market has approached it multiple times and failed to break through.

A decisive move above resistance would likely trigger another wave of buying as momentum traders jump into the market.

And beyond that?

The obvious target is $100 per barrel.

Round numbers have a special psychological effect on financial markets. They attract attention from traders, investors, analysts, and media outlets alike.

Crossing the $100 threshold wouldn’t change the fundamentals overnight.

But it would change sentiment.

Sometimes that’s enough.

Technical indicators are generally constructive as well. Several moving averages have turned higher, while trend-following models increasingly point toward upward momentum.

The market isn’t overheated yet.

But it’s beginning to look stronger than it has in months.

Three Paths for Oil From Here

Looking ahead, the market appears to face three realistic scenarios.

The first is the bullish case.

Under this outcome, geopolitical tensions intensify and supply concerns grow. Any serious disruption involving the Strait of Hormuz or regional infrastructure could push oil sharply higher.

In that environment, prices above $110 per barrel become entirely possible.

The second scenario is less dramatic but perhaps more likely.

Demand remains healthy. The global economy slows but avoids recession. Asian consumption improves, and U.S. summer travel supports fuel demand.

In that case, oil could gradually climb toward $100 per barrel by late summer.

Not an explosive rally.

Just a steady grind higher.

The third scenario is the bearish one.

China’s recovery disappoints. Europe weakens further. American consumers begin cutting back spending.

Demand softens.

Inventories rebuild.

Support levels fail.

If that happens, WTI could revisit $80 per barrel or even lower.

At the moment, markets seem to assign the lowest probability to this outcome.

But oil traders know better than anyone that sentiment can change quickly.

The Market Never Sleeps

Wednesday’s Asian session gave oil bulls something they haven’t had in a while: confidence.

WTI is climbing. Brent is climbing. Technical indicators are improving. Seasonal demand trends are supportive. Inventory expectations remain constructive. Geopolitical risks continue to hover in the background.

Taken together, that’s enough to keep buyers interested.

But oil has always been a market that rewards caution.

A single headline can reverse an entire week’s gains.

A surprise inventory report can erase bullish momentum in an afternoon.

A geopolitical incident can add ten dollars to a barrel overnight.

That’s the nature of the business.

For now, the signal is green.

The buyers are in control.

The market is looking higher.

Whether that optimism survives the next round of economic data, inventory reports, and geopolitical headlines remains to be seen.

But one thing is certain.

As traders in Asia were reminded on Wednesday morning, oil never stands still for long. And neither does the market that trades it.

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.