Gold Falls Amid Tensions Surrounding Iran

When War Stops Being Precious

Friday began on a disappointing note for precious metals markets in Asia. Gold, which has already been struggling this week, moved lower once again. Spot gold fell 0.8% to $4,440.84 per ounce, while futures declined by the same margin to $4,467. And this is happening even as the Middle East remains engulfed in conflict.

At first glance, war, missile strikes, military operations, and stalled negotiations should provide the perfect environment for gold to rally. Investors are traditionally expected to flock to the yellow metal as a safe haven. That is how it has always worked. That is what textbooks teach. That is what market logic suggests. But not today—and not this week.

The paradox has a simple explanation. The conflict between the United States and Iran, which has been ongoing for several months, has ceased to be a source of uncertainty. Instead, it has become a source of inflation. And inflation means higher interest rates. Higher interest rates, in turn, are a major headwind for gold.

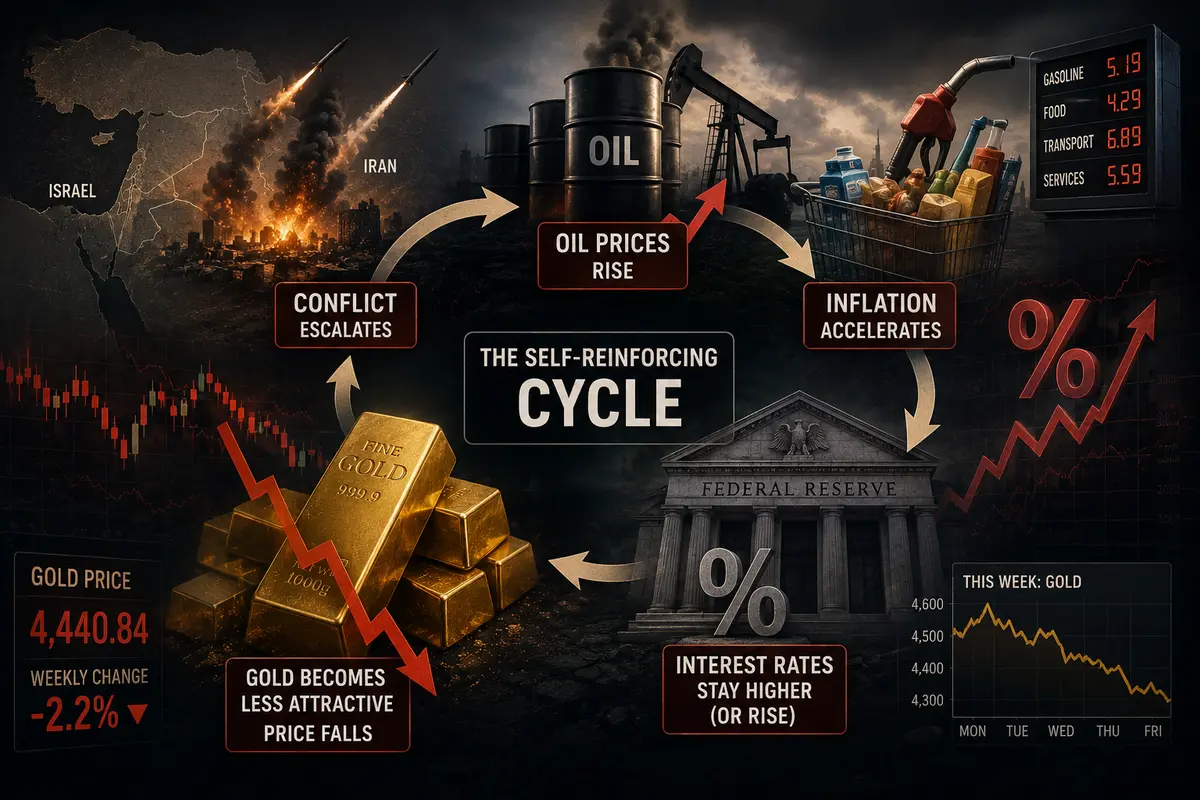

Gold is down approximately 2.2% for the week, marking its worst performance since early May. The reason is not the absence of geopolitical risks, but rather their abundance. The market is no longer afraid of war itself. It is afraid of what war does to oil prices and, through oil, to inflation and interest rates.

Let’s examine how a conflict in the Middle East has become a bearish factor for gold—and what may lie ahead for the yellow metal following the release of key U.S. employment data.

Middle East: Hope Is Gone, Long Live Inflation

Developments in the Middle East have been rapid and, for those hoping for peace, discouraging. Hopes for a U.S.–Iran agreement, which still seemed realistic earlier in the week, had all but vanished by Friday.

What happened?

First, Hezbollah, the Iran-backed Lebanese group, rejected a ceasefire proposal with Israel. Fighting in southern Lebanon continues. Israeli forces are expanding operations, while Hezbollah has responded with rocket attacks. Diplomats who were celebrating a breakthrough on Wednesday are once again facing disappointment.

Second, Tehran stated that a ceasefire in Lebanon is a prerequisite for any broader peace agreement with the United States. In other words, as long as Hezbollah remains engaged in conflict, negotiations over Iran’s nuclear program are unlikely to proceed. And Hezbollah appears in no rush to stop fighting.

Third, the United States and Iran exchanged additional military strikes. Reports throughout the week included missile attacks involving Kuwait and Bahrain, as well as strikes near Qeshm Island in the Strait of Hormuz. Each new escalation reinforced the perception that the conflict is becoming prolonged.

The result of this week is clear: minimal progress toward peace. There are no signs that either Washington or Tehran is willing to make significant concessions. On the contrary, both sides are expanding military deployments, intensifying rhetoric, and preparing for a lengthy confrontation.

For oil prices, this means one thing: the geopolitical risk premium is likely to remain elevated and could increase further. Oil is already trading near $95 per barrel for WTI and $97 for Brent. If the conflict enters a more intense phase, prices could easily reach $100–110 per barrel.

For gold, this scenario is toxic. Expensive oil fuels inflation. And inflation—especially when economic growth remains resilient—forces central banks to maintain tighter monetary policy.

The Federal Reserve, which only a month ago was hinting at possible rate cuts later this year, is no longer sending such signals. On the contrary, several Fed officials, including Dallas Fed President Lorie Logan, have warned that inflation risks are skewed to the upside. That raises the possibility that the Fed’s next move could be a rate hike rather than a cut.

Gold, which does not generate interest income, finds itself at a significant disadvantage in such an environment. When rates are high, investors prefer bonds or cash deposits that provide guaranteed returns. Gold offers only the prospect of price appreciation. When that prospect weakens amid hawkish central bank rhetoric, investors sell.

Inflation Expectations: Gold’s Biggest Enemy

To understand why gold is falling despite the conflict, it is essential to understand inflation expectations.

When violence escalates in the Middle East, traders focus on oil. Rising oil prices increase production and transportation costs across the economy—from gasoline and food to airline tickets and consumer goods. Inflation accelerates. Investors begin pricing in higher inflation over the next six to twelve months.

How do central banks respond? By raising interest rates. Higher rates cool economic activity and help contain inflation. However, they also make non-yielding assets less attractive. Gold is one of those assets.

This creates a self-reinforcing cycle. Conflict pushes oil prices higher. Higher oil prices fuel inflation. Inflation encourages the Fed to keep rates elevated—or even raise them further. High rates weigh on gold.

Since the outbreak of the U.S.–Israel conflict with Iran in late February, this mechanism has worked consistently. Every escalation initially triggers a short-term rally in gold driven by fear, followed by a decline as markets focus on the inflationary consequences.

The same pattern emerged this week. Gold rose at the beginning of the week when news of military strikes first surfaced. By midweek, attention shifted toward inflation concerns, and prices began to decline. Friday extended those losses. The weekly result: down 2.2%.

U.S. Labor Market: Friday’s Key Event

Later on Friday, the United States will release its May Nonfarm Payrolls report.

This report is always important, but today it matters even more because markets are desperately trying to determine the Fed’s next move.

Consensus forecasts point to slower job growth. The conflict with Iran, high interest rates, and a cooling economy are all expected to weigh on employment. Economists are forecasting around 180,000 new jobs—a decline from April but still a healthy figure.

However, there is an important caveat. Over the past six months, Nonfarm Payrolls have exceeded expectations four times. The U.S. economy continues to surprise analysts with its resilience. The labor market remains its strongest component.

As a result, an upside surprise cannot be ruled out.

If payroll growth comes in significantly above expectations—220,000 to 250,000 or more—it would signal that the labor market remains overheated. The Fed would gain another argument for maintaining high rates for longer or even raising them. The dollar would strengthen, and gold could decline sharply toward $4,380–4,400.

If payroll growth disappoints, coming in around 120,000–130,000, it would suggest that economic activity is slowing more rapidly than expected. The Fed could begin preparing markets for rate cuts. The dollar would weaken, and gold could rally toward $4,550–4,600.

If the figure lands close to expectations, between 160,000 and 190,000, the reaction will likely be muted. Gold could remain trapped in the current $4,400–4,500 range while investors await the next catalyst.

Which scenario is most likely? Given the resilience of the U.S. economy and the tendency for payrolls data to beat forecasts, another upside surprise cannot be ruled out. At the same time, 180,000 is already a demanding benchmark. Labor market growth cannot continue indefinitely. Perhaps May will finally reveal signs of a slowdown.

The Dollar and Gold: An Old Relationship

On Friday morning, the U.S. Dollar Index slipped by 0.01%. The move was almost imperceptible but still telling. The dollar appears to be pausing ahead of the payrolls release as investors avoid taking large positions before such a significant report.

For gold, this provides temporary relief. A weaker dollar generally supports higher gold prices.

However, the relief is unlikely to last. Once the data is released, the dollar will probably resume moving decisively—either higher or lower—depending on the outcome.

Fundamentally, the dollar remains strong. The U.S. economy continues to outperform Europe and Japan. Interest rates in the United States remain among the highest in the developed world. Geopolitical uncertainty continues to drive capital toward the dollar as a safe haven.

As a result, any pullback in the dollar is likely to attract buyers. And any rally in gold may continue to face selling pressure—at least until the inflation outlook and Fed rhetoric begin to change.

Other Precious Metals: Silver and Platinum Also Under Pressure

Gold was not the only precious metal to suffer this week.

Silver, often referred to as gold’s “poor cousin,” fell 1.7% on Friday to $72.63 per ounce. Weekly losses reached 3.5%.

Silver is particularly vulnerable because it serves both as a safe-haven asset and as an industrial metal. It is widely used in electronics, solar panels, and soldering. When economic growth slows, industrial demand weakens, limiting silver’s ability to benefit from its safe-haven status.

Platinum declined 0.9% on Friday to $1,880.76 per ounce. Weekly losses totaled 0.9%, meaning platinum outperformed both gold and silver, though that offers little comfort.

Platinum remains heavily dependent on the automotive industry, where it is used in diesel catalytic converters. The long-term shift toward electric vehicles continues to weigh on demand. In the short term, however, platinum generally follows broader precious metals trends.

As a result, all three major precious metals are ending the week in negative territory—an unusually unified market move.

Technical Outlook: Where to Find Support

From a technical perspective, the $4,440 level is psychologically important for spot gold.

Below that lies the first significant support zone near $4,400. If prices break lower, the next support levels are around $4,350 and then $4,300.

Resistance is located near $4,500, followed by $4,550 and $4,600.

Daily technical indicators suggest that gold has exited overbought territory and is currently trading in neutral conditions. This means there is room for both further downside and renewed upside momentum.

Trading volumes on Friday morning were below average as traders waited for the payrolls report. Once the data is released, a sharp move in either direction should be expected.

Scenarios for the Near Future

Bullish scenario for gold: Payrolls are weak (120,000–150,000). The Fed begins preparing markets for rate cuts. The dollar weakens. Gold rallies toward $4,550–4,600, with $4,650 as the next target.

Bearish scenario for gold: Payrolls are strong (220,000–250,000 or higher). The Fed maintains a hawkish stance. The dollar strengthens. Gold declines toward $4,350–4,400, with the possibility of testing $4,300.

Neutral scenario: Payrolls are close to expectations (160,000–190,000). Gold remains range-bound between $4,400 and $4,500. Markets wait for the next catalyst, whether it comes from the European Central Bank meeting next week or fresh developments in the Middle East.

Most analysts lean toward the neutral scenario, albeit with a slight bias toward the bearish one. The U.S. economy remains resilient, the labor market is still strong, and payrolls could once again exceed forecasts. If that happens, gold will likely remain under pressure.

Of course, geopolitics could still alter the picture. A major new escalation in the Middle East could trigger a fear-driven rally in gold, temporarily overriding inflation concerns. Such episodes, however, tend to be short-lived. Once fear subsides, markets typically return to focusing on inflation and interest rates.

Conclusion: Gold Awaits Its Verdict

Friday is shaping up to be a crucial day for gold. The Nonfarm Payrolls report could either halt the decline, accelerate it, or leave the market without a clear direction.

One thing, however, is becoming increasingly clear. The old formula—“war equals higher gold prices”—no longer operates in its pure form. The prolonged conflict in the Middle East has changed the market’s perception. The conflict is no longer viewed as a shock but as a background condition. And that condition is pushing oil prices, inflation, and interest rates higher—while pressuring gold lower.

For investors holding gold, the best course of action may be patience. Gold remains a defensive asset. It is unlikely to become worthless, unlike shares of an overheated technology company. But neither should investors expect explosive gains while the Federal Reserve remains reluctant to cut rates.

Patience. And more patience. Along with diversification—gold should be part of a portfolio, not the entire portfolio.

For now, Asia is trading, gold is falling, and the Nonfarm Payrolls report is only hours away.

Who will win this battle—the dollar or the yellow metal?

We will find out soon enough.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.