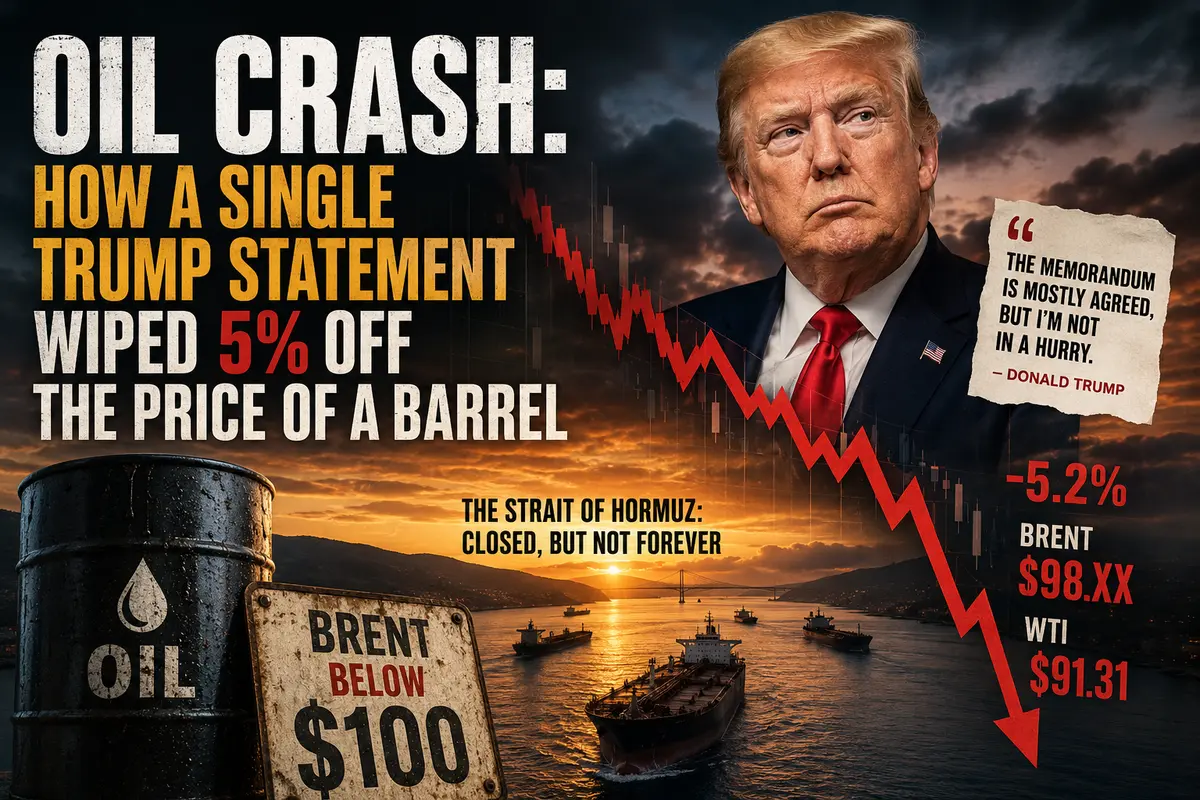

Oil Crash: How a Single Trump Statement Wiped 5% Off the Price of a Barrel

Monday morning on the oil markets began with a thunderclap out of a clear sky. But not the kind the world has grown used to over recent months — not explosions in the Strait of Hormuz, not missile strikes on tankers, not Trump’s threats to wipe Iran off the map. Quite the opposite. The thunder came from the prospect of peace. And that thunder hit oil prices with a force that neither diplomatic efforts nor market interventions had managed to achieve. Brent crude plunged below $100 per barrel, WTI broke through the $92 mark, and all of it happened within a single trading session. A five-percent drop — the kind of move usually associated with the start of a recession or the collapse of a cartel. But this time, the reason was different: hopes for the end of the most destructive oil crisis in decades.

The Psychological Threshold: $100 Falls

The $100-per-barrel mark for Brent is not just a round number. It is a psychological barrier separating “expensive but manageable oil” from “oil that kills economic growth.” The entire global infrastructure — from airlines to chemical plants, from farmers to taxi drivers — is built on the assumption that oil costs far less than $100. Once crude breaks above that level and stays there, business models begin to crack, inflation spirals accelerate, and central banks reach for loaded weapons.

Brent’s drop below $100 on Monday was not just another move on a chart. It was a signal to the market that the worst may be over. That the insane days when oil stormed past $110, $120, even $130 per barrel could be behind us. That the Strait of Hormuz, blocked by war, might reopen. That tankers stranded off the Iranian coast may finally begin moving again. That peace — fragile, uncertain, but possible — is already starting to be priced in.

Brent had not traded below $100 for three weeks. Historically, that is not a long time, but during wartime every week feels like a month. The fact that oil returned to pre-crisis levels within just a few sessions shows how much fear had been embedded in prices. Fear is fading — and prices are falling.

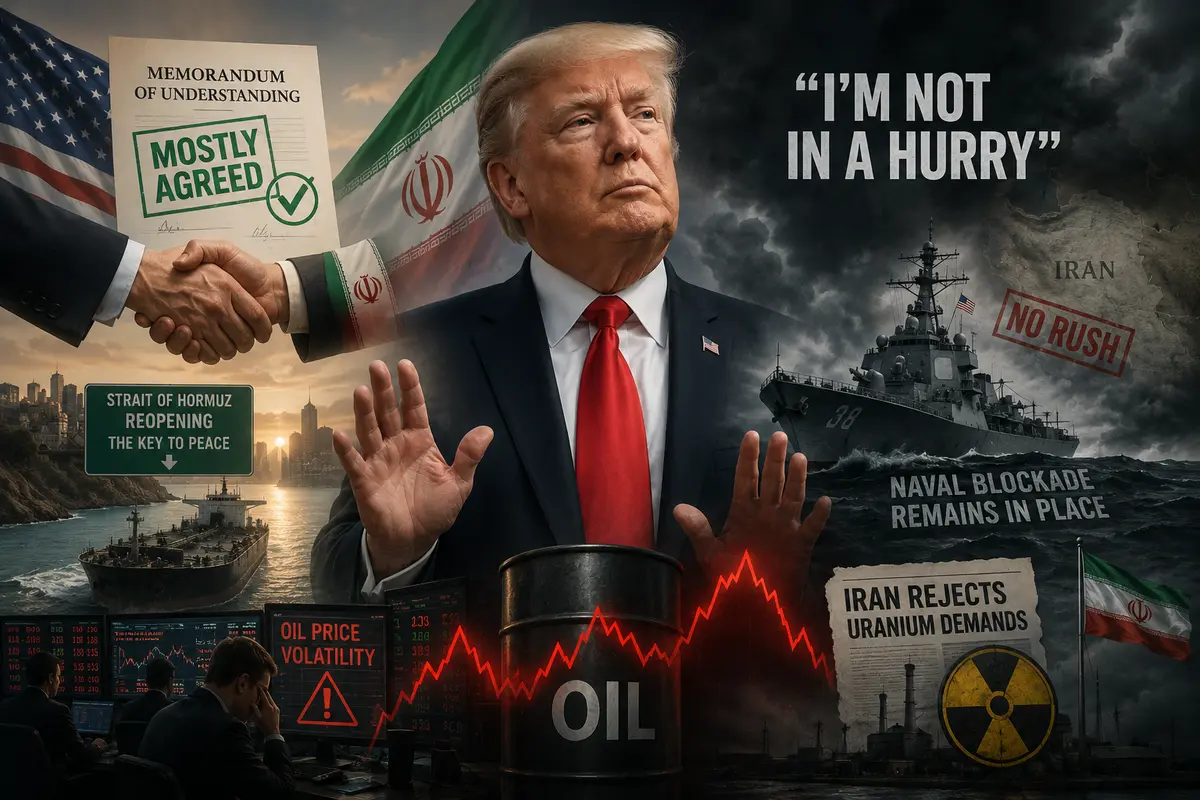

Trump: “The Memorandum Is Mostly Agreed, but I’m Not in a Hurry”

Over the weekend, Donald Trump did what he does best — moved markets with a few sentences. A memorandum of understanding for a peace agreement with Iran was “mostly agreed,” he said. The key objective of the deal: reopening the Strait of Hormuz, the vital oil artery whose closure triggered the global energy crisis. Messages from Pakistani mediators confirmed progress. The picture looked almost optimistic.

But Trump would not be Trump without adding darker shades to the picture. Almost immediately after announcing progress, he clarified that he was in no rush to finalize the agreement. The naval blockade of Iran would remain in place until a deal was reached. Iranian state media, for their part, denied Trump’s claims that an agreement was nearly complete. Most importantly, Tehran largely rejected U.S. demands to hand over its stockpiles of enriched uranium — still the key stumbling block in negotiations.

This dual rhetoric — “peace is close, but I’m not rushing” — creates a highly volatile mix for oil traders. On one hand, the very fact that both sides are sitting at the negotiating table discussing concrete terms instead of exchanging threats is enormous progress. On the other hand, disagreements over Iran’s nuclear program are fundamental. They cannot be erased with the stroke of a pen. And as long as they persist, every glimmer of hope could quickly turn into a new wave of escalation.

WTI and Brent: A Synchronized Collapse

WTI crude plunged 5.2% to $91.31 per barrel. U.S. crude mirrored Brent’s trajectory, confirming that the current move is driven by a broad macroeconomic factor rather than local issues affecting a particular benchmark. The spread between Brent and WTI, which widened to $7–8 at the peak of the crisis, has begun to narrow. This signals that the geopolitical premium embedded in Brent — the global benchmark most sensitive to Middle Eastern supplies — is gradually evaporating.

The synchronized decline is important for another reason: it rules out alternative explanations. If only WTI had fallen, analysts could point to uniquely American factors — rising production, growing inventories, export bottlenecks. If only Brent had dropped, one could blame local issues in the North Sea or Europe. But when both benchmarks fall together and by almost identical amounts, it means only one thing: the market is reassessing the fundamental global balance of supply and demand. And such a reassessment is only possible if traders believe Iranian and broader Middle Eastern oil may soon return to world markets.

The Strait of Hormuz: Closed, but Not Forever

Despite the euphoria triggered by Trump’s comments, the reality in the Strait of Hormuz remains harsh. Flows through the strait are still far below prewar levels. That is precisely what analysts describe as the price floor. Even if negotiations succeed, even if the memorandum is agreed, even if peace is around the corner — tankers do not resume operations overnight. Mines must be cleared, insurance procedures restored, crews brought back, and logistics chains rebuilt.

This gap between diplomatic progress and physical reality is what creates a floor under oil prices. Crude cannot collapse back to the pre-crisis $40–50 range while the strait remains effectively shut. But it can fall from the stratospheric $110 levels to a more grounded $98. Monday’s decline reflected not an immediate improvement in physical supply conditions, but a reduction in the “fear premium” that markets had priced in for a complete collapse of negotiations.

Last Week: Prelude to the Selloff

Monday’s crash did not emerge out of nowhere. It was the continuation of a move that began last week. That was when Trump first hinted at progress in negotiations, and oil prices started drifting lower. Over the weekend, optimism strengthened, rumors of a deal gained detail, and the opening of Asian trading on Monday unleashed a wave of selling.

It is important to understand that oil markets had become overloaded with long positions over recent months. Every trader, every hedge fund, every speculator had been betting that the war would drag on, the strait would remain closed, and oil prices would continue climbing. Once a signal of a possible reversal appeared, mass liquidation began. This was not just selling — it was a panicked rush for the exits, amplified by margin calls and stop-loss orders. In such conditions, a five-percent drop in a single session is not the limit. If news continues to improve, oil could fall even further. If negotiations deteriorate, prices could rebound just as violently.

Who Benefits from Cheaper Oil

Falling oil prices are a blow to producers, from Saudi Arabia to American shale companies. But for the overwhelming majority of the global economy, they are a blessing. India, which imports more than 80% of its oil, gains a chance to strengthen the rupee and curb inflation. Japan and South Korea, both resource-poor economies, can breathe easier. European airlines and transport companies, suffocating under high fuel costs, finally see light at the end of the tunnel. Even American consumers, who had been paying record prices at the pump, get some relief.

Oil falling below $100 is also a powerful disinflationary force — one that may achieve what central banks could not: reducing inflation expectations without further interest rate hikes. If the trend continues, the global economy may get a rare chance at a soft landing after the turbulence caused by the Iranian crisis.

Monday showed that oil markets desperately want peace. Every word suggesting progress in negotiations is now instantly converted into percentage losses in crude prices. But the fragility of the moment is obvious. Trump is not in a hurry. Iran rejects U.S. demands over uranium. The naval blockade remains in place. The actual reopening of the Strait of Hormuz is still far away.

And while diplomats bargain, oil will continue swinging between hope and fear, between $90 and $110 per barrel. Monday brought hope. But hope, in geopolitics, is the most unstable commodity of all. Tomorrow’s headline could once again send crude soaring. For now, oil is falling, and a world exhausted by soaring costs is getting a brief moment of relief.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.