Asia Holds Its Breath: Bank of Japan Raises Rates to a 31-Year High, but the Yen Barely Moves

Tuesday: A Day of Historic Decisions and No Market Reaction

Tuesday began with an event that, under normal circumstances, would have shaken currency markets to their core. The Bank of Japan raised its short-term policy rate by 25 basis points to 1.0% — the highest level in 31 years. The last time Japanese interest rates stood at this level was in 1995, when the internet was still in its infancy and many of today’s traders had not even been born.

The decision passed by a 7–1 vote. Governor Kazuo Ueda did not attend the meeting as he is currently undergoing medical treatment in the hospital. The meeting was chaired by Deputy Governor Shinichi Uchida instead. It is an unusual situation: the head of the central bank was absent during a historic policy decision.

And what happened?

Virtually nothing.

USD/JPY barely moved. The yen remained around ¥160.23 per dollar, only slightly different from levels seen before the announcement. Traders who expected a rate hike to strengthen the yen were left disappointed.

Why?

Because markets had already priced in the move over recent weeks. The real surprise would have been if the Bank of Japan had not raised rates. Since the hike was widely expected, the market reaction was essentially zero.

The yen continues to trade near the psychologically important ¥160-per-dollar level. Back in April, when the dollar first broke above ¥160, Japanese authorities intervened in the currency market. This time, they have remained on the sidelines, apparently viewing ¥160 as an acceptable exchange rate with policy rates at 1.0%.

But let’s take a closer look at what is actually happening across Asian currency markets on Tuesday, why most currencies appear frozen in place, and what traders are waiting for from other central banks.

Bank of Japan: A Historic Move Without the Drama

For Japan’s economy, raising rates to 1.0% represents a tectonic shift.

For decades, Japan lived with near-zero or negative interest rates. It was a country where money was effectively free. Corporations could borrow at around 0.1%, while investors borrowed yen and invested in higher-yielding assets abroad through the famous carry trade. The yen became the world’s preferred funding currency.

Now that era is slowly changing.

A 1.0% policy rate is still low by global standards (compared with approximately 5.5% in the U.S., 4.5% in the eurozone, and 5.25% in the U.K.), but it is no longer free money. Carry trades become less attractive. Japanese investors may gradually repatriate capital by selling foreign assets and buying yen, a process that would typically support the currency.

However, markets always look ahead.

Investors see the current rate hike as old news. The key question is what comes next. Will rates rise further to 1.25% or even 1.5% by year-end? Or is this a one-off move, with rates remaining at 1.0% for an extended period?

Analysts at MUFG noted after the decision:

“The market’s interpretation of the Deputy Governor’s comments may prove crucial, as the yen’s direction will depend on how convincingly he outlines the future path of interest rates.”

In other words, the critical factor is not today’s hike but how Deputy Governor Uchida describes the road ahead.

If he signals that the tightening cycle will continue, the yen could strengthen. If he remains cautious, the currency may stay weak.

So far, Uchida has not delivered any major surprises.

Markets are waiting.

Why Are Asian Currencies Frozen?

Aside from the Bank of Japan decision, very little is happening across Asian FX markets on Tuesday.

-

Chinese yuan (USD/CNY): little changed

-

South Korean won (USD/KRW): little changed

-

Singapore dollar (USD/SGD): little changed

-

Australian dollar (AUD/USD): down 0.2% ahead of the Reserve Bank of Australia meeting

-

Indian rupee (USD/INR): down 0.3%

Everything seems frozen.

The reason is simple: anticipation.

Traders are reluctant to open major positions ahead of Wednesday’s Federal Reserve meeting in the United States. This is the week’s most important event. The Fed’s decision and guidance will likely determine the next move for the U.S. dollar—and, by extension, nearly every major currency.

In addition, the anticipated U.S.–Iran peace agreement has not yet been formally signed. Markets expect the signing to take place in Switzerland on Friday. Until then, uncertainty remains.

Three days is a long time in global markets.

Anything can happen.

As a result, traders are sitting on their hands.

Peace With Iran: Positive for Risk Assets, Less So for Currencies

On Monday, reports of a preliminary peace agreement between the United States and Iran sparked a rally across financial markets.

Stocks rose.

Bonds gained.

Oil prices plunged.

The U.S. dollar weakened.

Asian currencies also received a modest boost.

By Tuesday, however, that momentum had faded.

Investors realized that the agreement remains a framework rather than a finalized deal. Markets want to see the actual signing ceremony, understand how the Strait of Hormuz will operate under the agreement, hear reactions from political factions within Iran, and assess whether any geopolitical obstacles could derail the process.

As a result, Asian currencies have entered a holding pattern.

Even positive news is no longer moving markets because investors want details before making commitments.

Australian Dollar and the Reserve Bank of Australia

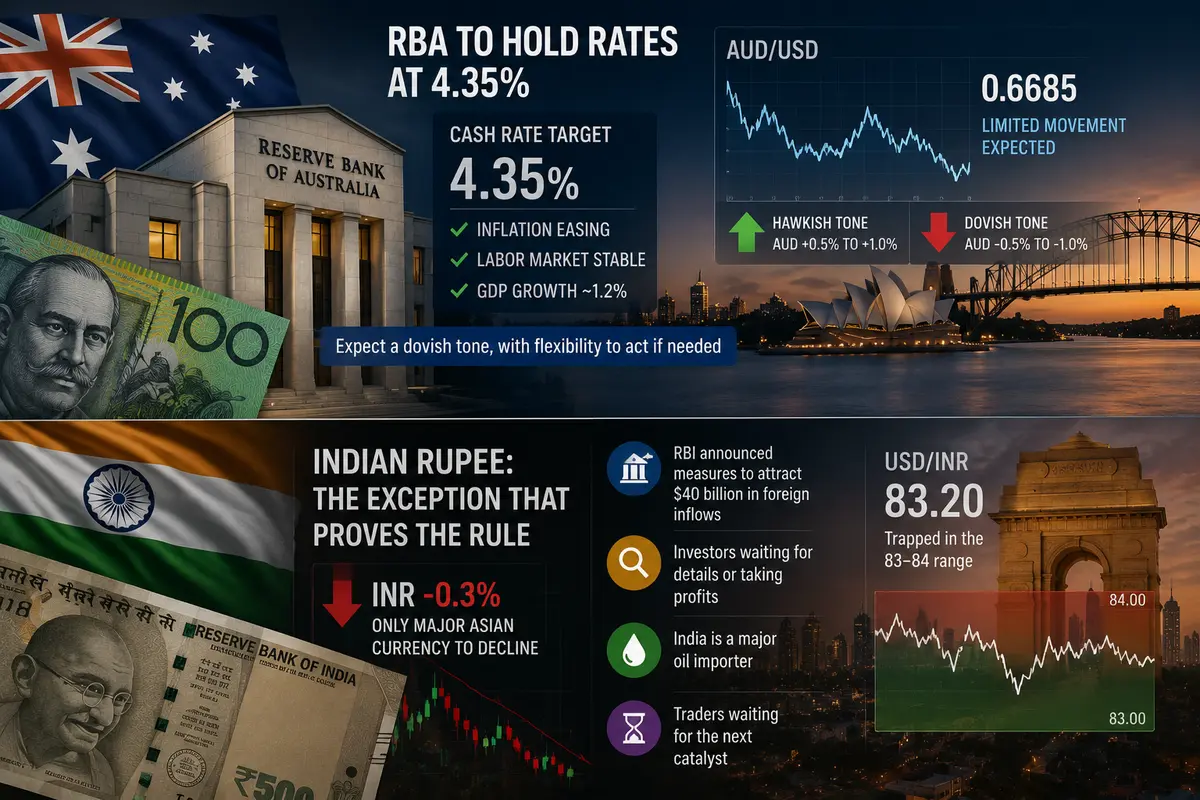

Later on Tuesday, the Reserve Bank of Australia (RBA) is scheduled to announce its policy decision.

Markets widely expect the RBA to leave interest rates unchanged at 4.35%, where they have remained since late 2025.

Why no hike?

Because Australia’s economy is slowing.

Inflation remains above target but is no longer accelerating at an alarming pace. The labor market remains stable without showing signs of overheating. Quarterly GDP growth was approximately 1.2%, below that of economies such as the United States and India.

The RBA is therefore expected to maintain a relatively dovish tone, likely emphasizing that inflation is gradually easing while retaining flexibility to act if necessary.

For the Australian dollar, that implies limited movement.

A slightly more hawkish statement could lift AUD by 0.5–1.0%.

A slightly more dovish tone could weaken it.

Given the broader market calm, however, dramatic moves appear unlikely.

Indian Rupee: The Exception That Proves the Rule

The Indian rupee declined by roughly 0.3% on Tuesday, making it the only major Asian currency to post a noticeable move.

Yet the decline appears driven more by technical factors than macroeconomic developments.

Last week, the Reserve Bank of India announced measures designed to attract approximately $40 billion in foreign capital inflows. Such measures should theoretically support the rupee.

However, investors seem to be waiting for additional details—or perhaps simply taking profits after previous gains.

India is also one of the world’s largest oil importers. Monday’s 5.5% decline in oil prices was positive for the rupee, but that benefit may already be reflected in market pricing.

For now, traders are waiting for the next catalyst.

Overall, the rupee remains trapped within the 83–84 per dollar range and will likely stay there for the rest of the week.

Chinese Yuan: Standing Still Alongside Everyone Else

The Chinese yuan (USD/CNY) was also largely unchanged on Tuesday.

The People’s Bank of China set the daily fixing at 6.89, about 0.1% stronger than the previous day. While technically a positive signal, the market largely ignored it.

China’s economy continues to recover, but only gradually.

Exports rose 19.4% in May, a strong result. Imports increased 27.4%, reflecting elevated energy costs and expensive oil imports.

If oil prices continue to decline, import costs could ease and China’s trade balance could improve, providing support for the yuan.

For now, however, the market is simply waiting.

And so the yuan remains frozen.

Wednesday’s Federal Reserve Meeting: The Main Event

Then comes Wednesday.

The Federal Reserve’s policy meeting.

Chair Kevin Warsh is expected to hold his first post-meeting press conference since taking office, and markets are eager to hear his views.

Most analysts expect the Fed to leave interest rates unchanged.

That part is predictable.

What is not predictable is what Warsh will say.

According to CME FedWatch pricing, markets currently assign roughly a 49% probability to a rate hike in December, down from 69% a week earlier. The decline reflects softer-than-expected core inflation data and optimism surrounding the Iran peace process.

If Warsh delivers a dovish message—suggesting inflation is moderating and the Fed can afford patience—the dollar could weaken sharply.

In that scenario, Asian currencies could gain 0.5–1.0% in a single session.

If he sounds hawkish—emphasizing persistent inflation risks and a willingness to tighten further—the dollar could strengthen, putting pressure on Asian currencies.

At the moment, nobody knows which path he will choose.

Warsh has historically been viewed as a hawk, but leaders often adapt their messaging once they assume new responsibilities.

Markets are waiting.

Conclusion: The Calm Before the Storm

Tuesday’s Asian currency markets are defined by silence.

The Bank of Japan raised rates to 1.0%, the highest level in 31 years, yet the yen barely reacted.

Most other Asian currencies are equally motionless.

Traders are waiting for two major catalysts:

-

Wednesday’s Federal Reserve meeting

-

Friday’s expected signing of the U.S.–Iran peace agreement

Without fresh catalysts, markets see little reason to take significant risks.

The yen, yuan, won, rupee, and Singapore dollar all remain trapped in narrow ranges.

The Australian dollar slipped slightly ahead of the RBA decision.

The Indian rupee weakened modestly.

But these are local fluctuations rather than meaningful trends.

For now, all eyes are on the Federal Reserve.

And until then, the market remains quiet.

A heavy, tense silence.

Because in financial markets, silence often precedes the biggest moves.

And waiting is sometimes the hardest part—not only in trading, but in life.

Especially when billions of dollars are at stake.

And when the future still hangs between hope and uncertainty.

For now, nobody knows.

Everyone is waiting.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.