Asia Frozen in Place: U.S. Strikes on Iran, Inflation, and the Dollar Keep Currencies Under Pressure

Thursday Morning: Calm Before the Storm or Quiet After the Shock?

When you wake up in Singapore, Tokyo, or Shanghai on Thursday and open the charts, you see something unusual. Asian currencies are neither falling nor rising. They are standing still — like rabbits frozen in the headlights.

The South Korean won gained just 0.2%, a move barely beyond statistical noise. The Indian rupee also rose 0.2%. The Singapore dollar, Australian dollar, and Chinese yuan were virtually unchanged. The Japanese yen remained stuck at 160.52 per U.S. dollar.

The U.S. Dollar Index (DXY) is holding near 100. It is not falling, despite inflation data released yesterday that ING analysts described as “softer than expected.” It is not rising either, even after overnight reports of new U.S. military strikes against Iranian targets. It is simply standing still — as if the entire world is holding its breath.

And that is what makes this calm so unsettling. Beneath the surface are forces capable of tearing markets apart at any moment: new U.S. strikes on Iran, the threat of a blockade of the Strait of Hormuz, oil prices that have surged but have not yet been fully reflected in currency markets, U.S. inflation accelerating to a three-year high, and the possibility of a Bank of Japan rate hike next week while its governor is reportedly hospitalized.

Traders do not know what to do. They are neither buying nor selling. They are waiting for clarity.

And there is none.

Let’s examine what happened over the last 24 hours and where Asian currencies could head next.

New U.S. Strikes on Iran: Is the Strait of Hormuz Closed?

Wednesday night brought fresh concerns. U.S. forces reportedly carried out additional strikes against Iranian targets. The Pentagon described them as a “proportional response” to earlier Iranian actions, including the reported downing of a U.S. military helicopter near the Strait of Hormuz earlier this week.

Iran, however, appears to believe that tensions have crossed a critical threshold.

Tehran has announced a halt to shipping through the Strait of Hormuz.

This is not just another narrow waterway. The Strait of Hormuz is one of the world’s most important transportation corridors. Between 15% and 20% of global oil consumption passes through it every day — roughly 17–20 million barrels.

Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar all depend on the strait to export their oil.

If Iran were to successfully block the passage — and it possesses the naval assets, missiles, and mines capable of making the route hazardous for tankers — the consequences for the global economy could be severe. Oil prices could surge to $150, $200, or even $300 per barrel. Inflation in the United States, Europe, and Asia could jump sharply. Central banks might be forced to raise interest rates aggressively even at the expense of economic growth. Recession risks would rise dramatically.

For now, Iran’s announcement remains a threat rather than a fully realized reality. Shipping continues according to tracking services, although tankers have reportedly slowed transit and insurance premiums have climbed.

For Asian currencies, the risk is twofold. First, geopolitical uncertainty drives investors toward the U.S. dollar as a safe haven. Second, a disruption in Hormuz would hit Asia harder than the United States because Asia is the world’s largest oil-importing region. China, Japan, South Korea, and India all depend heavily on Middle Eastern energy supplies.

At the moment, traders are waiting. Will the blockade become real? Will further strikes occur? Will the United Nations intervene? What will President Trump say?

Without answers, markets are unwilling to take major risks.

U.S. Inflation: Worse Than Expected — But With a Twist

Wednesday brought the highly anticipated U.S. consumer inflation report for May.

The results were mixed.

On one hand, headline inflation accelerated. The annual rate rose to 4.2%, the highest level since April 2023. Americans have not seen inflation this high in more than three years. The main culprit was energy. Gasoline prices surged amid Middle East tensions, while airfares also increased sharply.

On the other hand, core inflation — which excludes volatile food and energy prices — came in softer than expected. Monthly core CPI increased by 0.2%, down from 0.4% in April and below the 0.3% consensus forecast.

ING analysts summarized the situation clearly:

While headline inflation was boosted by rising gasoline and airfare costs, other components remained more subdued, resulting in softer-than-expected core inflation.

What does this mean for the Federal Reserve?

The picture remains complicated.

Headline inflation is uncomfortably high. Yet underlying inflation pressures may be easing. The Fed does not need to panic, but it does need to watch closely.

Markets still lean toward a more hawkish outlook. The probability of a December rate hike remains above 70%. However, if core inflation continues to slow, those expectations could ease.

For the dollar, that means the recent rally may be losing momentum. The DXY, which recently touched 100.2, is now hovering around 100.

For Asian currencies, that offers a small window of relief — but only a possibility, not a guarantee.

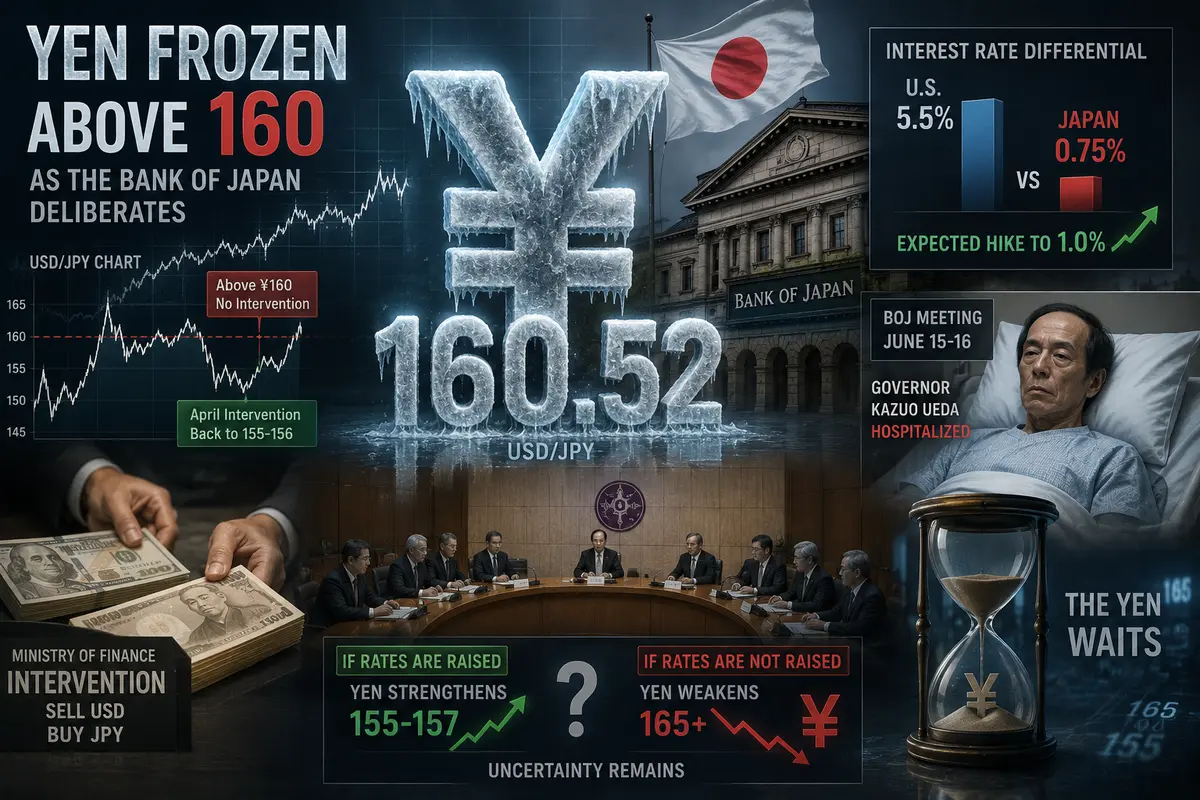

Yen Frozen Above 160 as the Bank of Japan Deliberates

The Japanese yen remains near 160.52 per dollar, almost unchanged from the previous day.

Yet beneath that stability lies enormous tension.

Back in April, when the dollar first broke above ¥160, Japan’s Ministry of Finance intervened in the foreign exchange market, selling dollars and buying yen. Tens of billions of dollars from foreign reserves were reportedly deployed. The intervention worked temporarily, pushing USD/JPY back toward 155–156.

Now the yen is once again above 160, and no intervention has appeared.

Why?

Because Japanese authorities understand that intervention is only a temporary solution. For the yen to strengthen sustainably, interest rate differentials between Japan and the United States must narrow. That requires higher Japanese interest rates.

And the Bank of Japan appears prepared to move in that direction.

Markets expect another rate increase at next week’s meeting. Japan’s policy rate currently stands at 0.75% after several hikes this year. Expectations are for a move to 1.0%.

That is still far below the U.S. rate of 5.5%, but the direction matters.

Complicating matters is the reported hospitalization of BOJ Governor Kazuo Ueda, who may miss the June 15–16 meeting. The meeting itself will proceed, and decisions can still be made collectively, but uncertainty has increased.

If rates are raised, the yen could strengthen toward 155–157 per dollar.

If not, the currency could weaken toward 165 and beyond, potentially forcing another round of intervention.

For now, the yen waits.

And so does everyone else.

Chinese Yuan: Stability Under Pressure

The offshore Chinese yuan (USD/CNH) is virtually unchanged.

At first glance, that seems encouraging. Despite Middle East tensions and rising oil prices, the yuan has avoided significant losses.

But this stability reflects active management by China’s central bank rather than market strength.

The People’s Bank of China continues to guide the currency through its daily fixing mechanism, limiting excessive fluctuations.

Fundamentals remain challenging.

China’s economic recovery has been slower than expected. Exports rose 19.4% in May, a strong figure, but many analysts worry that it reflects front-loaded purchasing driven by geopolitical concerns rather than sustainable demand.

Imports climbed 27.4%, partly due to higher energy costs, putting pressure on the trade balance.

Meanwhile, capital outflows continue. Foreign investors are selling Chinese stocks and bonds, converting yuan into dollars, and moving funds abroad.

For now, the PBOC remains in control.

But if Middle East tensions escalate further, oil prices continue rising, and the dollar strengthens again, maintaining yuan stability will become increasingly difficult.

Indian Rupee, Korean Won, and Singapore Dollar: All in the Same Boat

The Indian rupee weakened by 0.2%.

The move was small but meaningful. India imports nearly 80% of its oil consumption. Higher energy prices worsen the country’s trade balance and weigh on the rupee. Even recent measures by the Reserve Bank of India cannot fully offset an external oil shock.

The South Korean won also weakened by 0.2%.

South Korea is even more dependent on imported energy than India. The country lacks significant domestic oil, gas, and coal resources. Every increase in oil prices translates directly into higher import costs and additional pressure on the won.

The Singapore dollar was essentially unchanged.

As a trade- and finance-driven city-state, Singapore often serves as a barometer for Southeast Asia. The fact that the currency has not weakened significantly is encouraging. Yet it has not strengthened either.

Everyone is waiting.

The Australian dollar also remains stable.

Unlike most of Asia, Australia benefits from rising commodity prices. As a major exporter of coal, iron ore, and natural gas, higher energy prices can provide an offsetting economic boost.

Still, uncertainty dominates.

Too many risks remain unresolved.

What Comes Next: PPI and Jobless Claims

Thursday brings two important U.S. economic releases.

First, the Producer Price Index (PPI) for May.

If producer prices exceed expectations, concerns about inflation pressures flowing from producers to consumers will intensify, potentially supporting the dollar.

If PPI comes in softer, the dollar could weaken modestly.

Second, weekly jobless claims.

This remains one of the most closely watched indicators of labor market health. If claims stay low, it will reinforce the view that the U.S. economy remains strong and support hawkish Fed expectations. If claims rise meaningfully, markets may begin pricing a more cautious Federal Reserve.

ING analysts noted that inflation should ease somewhat in June due to falling gasoline prices but remains vulnerable to continued energy market volatility.

The key word is vulnerable.

As long as Middle East tensions persist, oil prices may remain elevated.

Elevated oil prices can sustain inflation.

Persistent inflation can force tighter monetary policy.

And tighter monetary policy can strengthen the dollar.

It is a self-reinforcing cycle.

Conclusion: Asian Currencies Are Waiting for a Signal

Thursday morning finds Asian currencies in a state of paralysis.

They are neither falling nor rising.

They are waiting.

New U.S. strikes on Iran and the threat of a Strait of Hormuz blockade have created an atmosphere of extreme uncertainty. U.S. inflation data delivered mixed signals. The Bank of Japan may raise rates, but leadership uncertainty has complicated the outlook.

Traders have reduced positions, cut risk, and sought shelter in the dollar.

But without a new catalyst, they are unwilling to commit to major new bets.

That catalyst could come from U.S. PPI data.

It could come from next week’s Federal Reserve meeting.

Or, most likely, it could come from the Middle East.

If Iran actually blocks the Strait of Hormuz, oil prices could surge, the dollar could strengthen sharply, and Asian currencies could come under severe pressure.

If tensions ease, markets may experience a temporary relief rally.

For now, however, there is only silence.

A heavy, tense silence that can feel worse than any shout.

Because in silence, all anyone can do is wait.

And waiting is often the hardest part of trading — and of life — especially when billions of dollars are at stake and war once again dominates the headlines.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.