Oil Calm Before the Storm: WTI Pulls Back, but Tensions Remain High

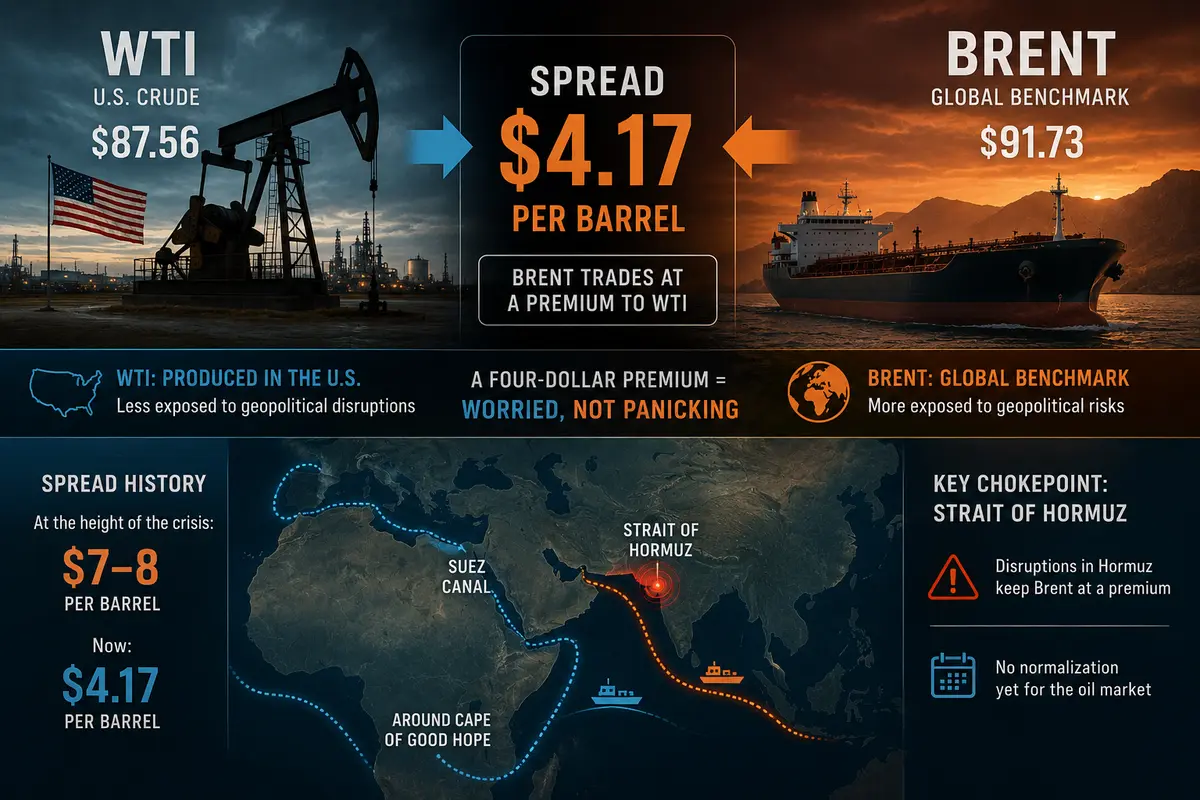

Friday’s Asian trading session brought a brief respite to the oil market. July WTI futures fell by 1.5%, dropping to $87.56 per barrel. Brent followed its U.S. counterpart lower, losing just over 1% and settling at $91.73 per barrel. At first glance, this looks like a routine correction after the sharp rally triggered by the latest strikes on Iran. But a closer look at the numbers suggests otherwise: this is not merely a pullback—it is a market holding its breath before the next move. Too much explosive risk has accumulated beneath the surface, too many unresolved questions remain, and too much depends on what unfolds over the weekend.

Down 1.5%: Profit-Taking or a Trend Reversal?

Friday’s decline in WTI fits a classic pattern. After Thursday’s surge of more than 3%, fueled by reports of strikes on Bandar Abbas and a retaliatory attack by Iran’s Islamic Revolutionary Guard Corps (IRGC), traders chose to lock in profits ahead of the weekend. Few are willing to hold long positions through Saturday and Sunday when anything could happen—from fresh military strikes to an unexpected diplomatic breakthrough. This fear of the “geopolitical weekend” is a familiar feature of every major Middle Eastern crisis.

Support at $87.27 remains intact. Prices bounced from that level, preventing bears from gaining momentum. This suggests that the underlying fundamentals have not changed: the Strait of Hormuz remains effectively disrupted, supply chains are impaired, and the global oil market remains undersupplied. A decline of 1.5% is not a trend reversal—it is simply a pause after a short sprint.

Resistance at $99.43 looms overhead, separating the current range from the triple-digit prices seen during the hottest phase of the conflict. If tensions continue to escalate, that level could be tested as early as next week. If, against all expectations, there is progress in negotiations, oil could retreat much more sharply.

Brent and the Spread: A Four-Dollar Risk Premium

The price difference between Brent and WTI currently stands at $4.17 per barrel. This is a moderately elevated spread that reflects the persistent geopolitical risk premium embedded in the global benchmark. Brent, being more sensitive to disruptions in the Persian Gulf, continues to trade at a notable premium to U.S. crude.

For comparison, at the height of the crisis, when the Strait of Hormuz was first disrupted, the spread widened to $7–8 per barrel. It has narrowed since then, but it has not disappeared. A four-dollar premium is the market’s way of saying: we are still worried, but we are no longer panicking. Traders have adapted to the new reality, but they do not believe it will end anytime soon.

The spread also reflects logistical differences. U.S. WTI is produced domestically and is less dependent on shipping routes through high-risk regions. Brent, by contrast, is transported via tanker routes that pass through the Strait of Hormuz, the Suez Canal, and other strategic chokepoints. As long as Hormuz remains disrupted, Brent is likely to retain a premium. And as long as that premium exists, it is too early to talk about a normalization of the oil market.

The Dollar as a Fear Gauge

The U.S. Dollar Index was little changed on Friday, gaining a symbolic 0.04% to reach 99.01. The dollar appears stable, but that stability is somewhat deceptive. The currency remains near multi-month highs, supported by the Federal Reserve’s hawkish rhetoric and strong demand for safe-haven assets.

For the oil market, this creates a constant background headwind. A stronger dollar makes oil more expensive for holders of other currencies, reducing demand. However, at present, that effect is being overshadowed by geopolitical fears. Oil and the dollar are rising simultaneously—a classic sign that markets are being driven not by economics, but by geopolitics.

Investors do not know what tomorrow will bring. They see continued strikes on Iran, increasingly bold retaliatory actions, and stalled diplomacy. As a result, they are buying both dollars and oil—dollars as a safe haven and oil as insurance against supply disruptions. This dual hedge is likely to remain in place until the conflict is resolved.

The Strait of Hormuz: A Silence That Isn’t Silent

The primary reason oil has struggled to fall below $87 per barrel is the Strait of Hormuz. Technically, some tankers are still passing through. In reality, however, oil flows remain well below pre-conflict levels. Insurance premiums for shipping have surged. Shipowners are reluctant to send vessels into a region where U.S. destroyers and Iranian patrol boats are exchanging fire. Every tanker entering the strait does so at considerable risk.

As long as this situation persists, the global oil market will remain undersupplied. Alternative routes—through the Suez Canal or around the Cape of Good Hope—cannot fully compensate for the lost volumes. Inventories in developed economies continue to decline, while demand, particularly from Asia, is recovering after the post-pandemic slowdown. The physical reality is straightforward: there is not enough oil. Prices are reflecting that reality.

Friday Before the Storm

Friday is always a special day in the oil market. Traders reduce exposure, take profits, and move into cash ahead of the weekend. No one wants to hold large positions through Saturday and Sunday when events can emerge that completely reshape the market. And the current situation offers more reasons than usual for caution.

The weekend could bring almost anything. New U.S. strikes on Iran. Additional retaliatory attacks by the IRGC. Statements from Donald Trump that could either bury hopes for peace or unexpectedly revive them. Continued negotiations in Doha. Perhaps even a breakthrough that no one currently anticipates. Any of these scenarios could send oil sharply higher toward $99 and beyond, or lower toward $85 and below.

That is precisely why Friday’s Asian session was characterized by caution. A decline of 1.5% does not signal an exodus—it reflects preparation for uncertainty. Traders are closing positions, but they are not opening new ones. They are waiting. Waiting to see what the weekend brings. Waiting to hear what Trump says. Waiting to see what Iran does. Waiting for the Strait of Hormuz to reopen—or for it to become clear that it may not reopen anytime soon.

The oil market paused on Friday. WTI hovered around $87.50, while Brent traded near $92. These levels reflect today’s reality: the conflict continues, supplies remain disrupted, and peace has not arrived. But they also leave room for dramatic moves in either direction. If a miracle occurs, oil will fall. If a catastrophe unfolds, oil will surge.

For now, there is silence.

The kind of silence that exists only before a storm.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.