The Euro’s Role in the World Remains Stable Despite Uncertainty

The Alternative That Never Became an Alternative

There was something almost tragicomic about it. Throughout 2024, analysts, economists, and geopolitical observers kept wondering: surely this is the moment when the euro finally makes its move.

The United States pursued such an unpredictable economic policy that even its own allies were left bewildered. Trade wars, abrupt policy reversals, public disputes within the administration—a perfect storm that should have pushed the world to look for an alternative to the dollar.

And that alternative already had a name: the euro. The world’s second-largest reserve currency. The natural contender for the throne.

But the world, as it often does, refused to behave as experts expected. It did not rush into the arms of the euro. In fact, it did not rush toward any single currency at all. Instead, investors, central banks, and major funds cast their votes for something else entirely: gold—and the currencies of small, often overlooked countries.

The euro remained roughly where it had always been, holding a share of about 20% of the global market.

These are not rumors or speculation. The figures were published on Tuesday by the European Central Bank (ECB) in its latest report. And, frankly, the numbers make for rather disappointing reading from a European policymaker’s perspective.

Because 20% is not bad. But it is not progress either. It is stagnation. And perhaps most frustrating of all, the euro’s current share remains below the level it enjoyed twenty years ago, in the early years of its existence.

Numbers That Don’t Lie

Let’s dispense with euphemisms. Twenty percent is not a commanding second place. It is a frozen picture.

The euro is neither growing nor shrinking. It is holding the line.

At first glance, given reports that the dollar is also losing ground, this could be framed as a success: the European currency weathered the storm and maintained its position. Yet the tone of the ECB report suggests disappointment rather than satisfaction. A rare opportunity was missed.

Why didn’t investors flock to the euro?

The answer is complicated, but the key reasons are fairly obvious.

First, Europe failed to offer the world anything fundamentally new. Yes, the euro is a reliable currency backed by one of the world’s largest economic blocs. But reliability alone, without a compelling growth story, does not attract capital.

Second, uncertainty originating in the United States proved contagious. Investors unsettled by America’s policy swings did not seek refuge in Europe. Instead, they sought refuge beyond the reach of any single country—in gold and broader diversification.

The ECB report states plainly that both the dollar and the euro lost market share to gold and so-called nontraditional reserve currencies.

In other words, the world is no longer choosing between Washington and Frankfurt. Increasingly, it is choosing neither—or opting for assets that are not dependent on the decisions of any single government.

Where the Euro Still Excels

Not everything is bleak.

There is one area where the euro remains strong and is even setting records: international debt financing.

Last year, euro-denominated debt issuance exceeded $1.1 trillion, the highest level since the currency’s launch in 1999.

Companies, corporations, and even some governments increasingly prefer borrowing in euros. Why? Because it is relatively cheap. Financing costs are low, and bid-ask spreads are narrow. For bond issuers, it is an ideal environment.

Yet success in debt markets is, in many ways, a victory for accountants rather than geopoliticians.

Yes, corporate treasurers like the euro. Yes, issuing debt in the currency can be advantageous. But that alone is not enough to make a currency truly global.

For that to happen, foreign central banks must hold it in their reserves. International contracts for oil, gas, and other commodities must be denominated in it. Investors must flee into euro assets during crises the way they once rushed into U.S. Treasury bonds.

That has not happened—at least not yet.

Lagarde’s Diagnosis

ECB President Christine Lagarde comes across in the report like a doctor who knows the diagnosis but cannot persuade the patient to take the medicine.

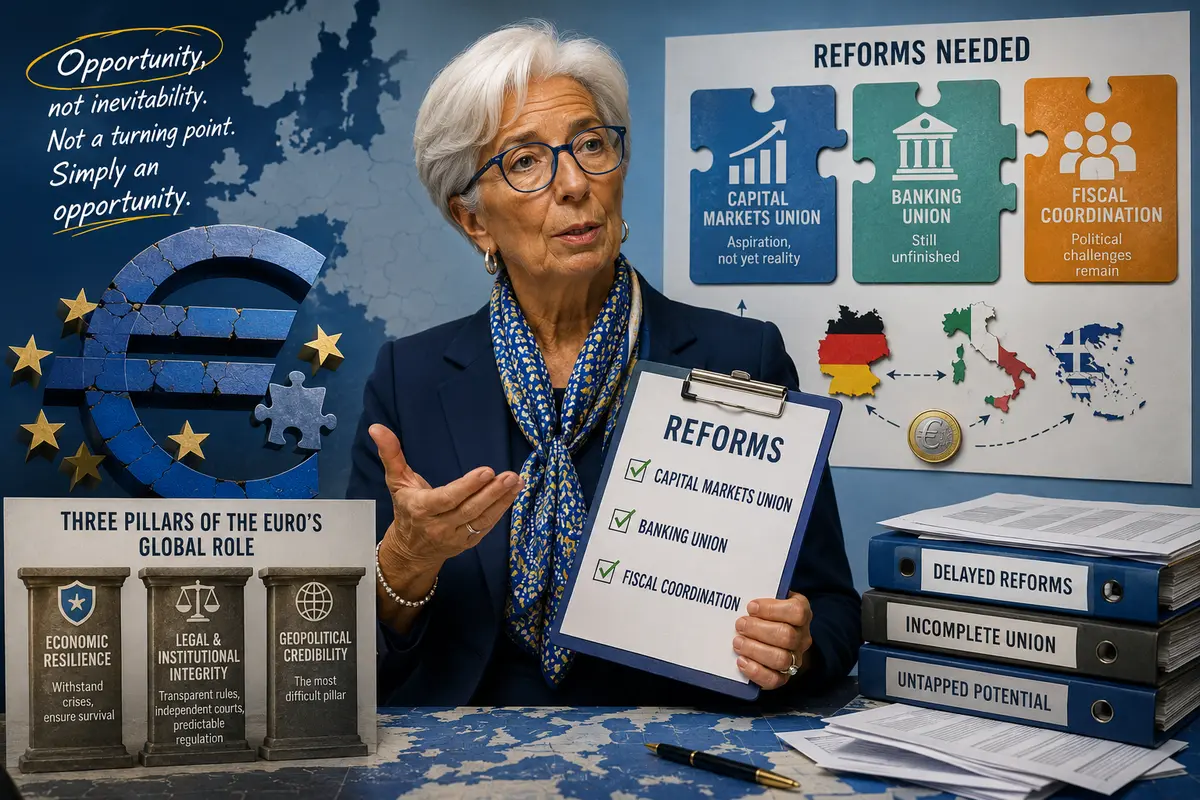

She argues that the eurozone has an opportunity to strengthen the euro’s global role.

The key word is opportunity.

Not inevitability. Not a historic turning point. Simply an opportunity.

And it will become reality only if European policymakers finally implement long-delayed financial reforms.

What reforms?

Lagarde does not go into detail in this report, but anyone who follows European economics knows the list well:

-

A genuine Capital Markets Union, still more aspiration than reality.

-

A fully completed Banking Union, which remains unfinished.

-

Greater fiscal coordination among eurozone members—a politically sensitive topic because Germany does not want to pay for Greece, while Italy does not want Berlin lecturing it on fiscal discipline.

Without these institutional changes, the euro will always remain slightly incomplete: powerful, but not dominant.

Lagarde identifies three pillars on which the euro’s global role must rest:

-

Economic resilience — the ability of the eurozone to withstand crises without raising doubts about its survival.

-

Legal and institutional integrity — transparent rules, independent courts, and predictable regulation.

-

Geopolitical credibility — arguably the most problematic pillar of all.

Geopolitical Credibility: The Weak Link

In simple terms, geopolitical credibility means that other countries listen to you not because they like you, but because you possess the power to back up your words.

The United States has long excelled at this.

China is steadily improving its position.

Europe, however, remains an economic giant and a political dwarf.

The European Union struggles to agree on a common foreign policy. Hungary blocks sanctions supported by the other twenty-six member states. Germany hesitates over military assistance to Ukraine. France often says one thing and does another.

Under such conditions, it is difficult to persuade the world that the euro is a reliable alternative to the dollar.

Because behind the euro there is no single voice.

There are twenty voices, often singing different tunes.

This also helps explain why investors chose gold over the euro in 2024.

Gold does not care whether Viktor Orbán and Emmanuel Macron are at odds, or whether Olaf Scholz and Giorgia Meloni can agree on a budget.

Gold is chaos in its purest form—but predictable chaos.

Its price may rise or fall, but the metal itself remains unchanged.

The euro, by contrast, depends on decisions made in Brussels, Frankfurt, Berlin, Paris, and Rome. And as the past year demonstrated, those decision-makers have not always inspired confidence.

Record Highs That Change Nothing

Let us return to the debt market record.

$1.1 trillion is an impressive figure, and Europe has every reason to celebrate it.

But let’s be honest: this is an achievement of financial engineering, not a breakthrough in the global monetary system.

Companies borrow in euros because interest rates are attractive. It is a pragmatic calculation.

If conditions become more favorable in the United States tomorrow, many of those same borrowers will shift back to the dollar without hesitation.

There is no loyalty in global capital markets—nor should there be. Capital seeks returns, not ideology.

Moreover, the fact that both heavyweights—the dollar and the euro—lost market share to gold and exotic currencies points to a deeper structural shift.

The world is growing tired of a monetary duopoly.

It no longer wants to choose between Washington and Brussels.

It wants to spread risk more widely.

If this trend accelerates, we could conceivably see a world ten years from now where the dollar holds 15%, the euro holds 15%, and the remainder is distributed across a broad range of smaller currencies and precious metals.

Such a world would be less predictable.

But perhaps more resilient.

A paradox.

What Europe Must Do Now

In her report, Lagarde calls for moving from words to action.

It is a compelling phrase, but behind it lies a vast landscape of bureaucracy and political obstacles.

If the euro is to strengthen its position, Europe must accomplish three major tasks:

-

Complete the Banking Union, so that a bank in Lisbon trusts a bank in Helsinki—and vice versa.

-

Create a truly unified capital market, allowing a German pension fund to purchase Italian bonds without hesitation.

-

Most difficult of all, establish a common fiscal framework—ideally including a eurozone budget with the authority to issue joint debt.

None of these reforms will happen quickly.

None will be painless.

Germany fears becoming the payer of last resort. France worries about losing sovereignty. The Netherlands and Finland fear their taxpayers will end up rescuing fiscally irresponsible southern economies.

These concerns are understandable.

But they are also what keep the euro trapped: a strong currency, yet not a leading one.

And until those fears are overcome, the euro’s role in the world is likely to remain stable.

The word stable sounds almost complimentary.

But anyone reading the ECB report carefully understands what it really means:

Stability through stagnation.

Not falling, but not rising either.

Waiting.

Watching.

Hoping for reforms that never quite begin.

The world is not waiting.

It is already moving money into gold.

And the euro watches from the sidelines, possessing all the ingredients necessary to become a truly great global currency, yet somehow postponing the decisive step until tomorrow.

A tomorrow that, as we all know, never arrives.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.