Silence on the Airwaves: Why Bitcoin Fell Asleep While the AI Sector Went Crazy

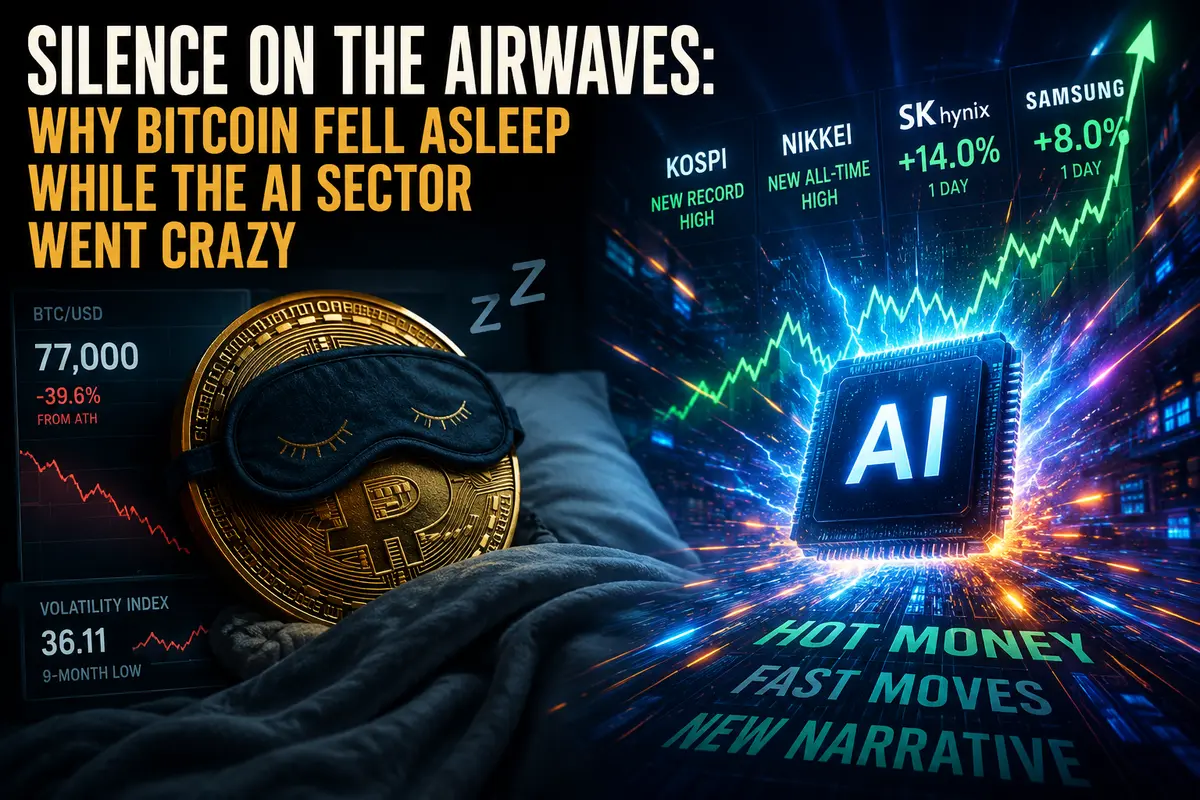

Nine months. That’s how long it has been since Bitcoin was last this boring. The Bitcoin Volmex implied volatility index — the market’s thermometer of excitement — has dropped to 36.11, its lowest level since last September. The price is stuck around seventy-seven thousand dollars, nearly forty percent below the all-time high above one hundred twenty-six thousand reached in October. And while traders in the worlds of equities and semiconductors are losing their minds over massive rallies, the crypto market has sunk into a lethargic sleep. This is not a crash, not a collapse, not capitulation. It is something more insidious — a slow fading of interest.

Hot Money Moved Into AI

To understand where the speculative capital went, you only need to look at the headlines of recent weeks. South Korea’s KOSPI is hitting record highs. Japan’s Nikkei is storming historical peaks. SK Hynix has just entered the trillion-dollar company club. Samsung is celebrating the resolution of its labor dispute and climbing higher as well. This entire fireworks show is happening in one sector — manufacturers of memory chips, AI accelerators, and related hardware. That is where the “hot money” has gone: into AI and semiconductor stocks, absorbing the same speculative capital that once fueled crypto rallies.

Orbit Markets co-founder Caroline Mauron puts it with brutal clarity: “Retail interest is flowing into other sectors in search of new trading opportunities, as confirmed by ETF outflows.” And the numbers do not lie. In May, around one billion dollars was withdrawn from U.S. spot Bitcoin ETFs, breaking a two-month streak of inflows. Institutional investors who had enthusiastically entered crypto through regulated products are now taking profits or cutting positions.

The logic behind this exodus is simple and ruthless. Bitcoin is trapped in a range. It cannot break resistance and move to new highs. Meanwhile, the AI sector is posting double-digit gains within days. SK Hynix gained fourteen percent in a single session. Samsung rose eight percent. What kind of returns would Bitcoin need to compete with those moves? The answer: returns it simply cannot deliver right now.

Volatility Sellers as Market Anesthesia

But fading retail interest is only half the story. The other half lies in the mechanics of the market itself, and here the situation becomes even more paradoxical. Bitcoin has become a victim of its own success — success in attracting large institutional players who operate very differently from retail traders.

Rajiv Sawhney of Wave Digital Assets explains it just as bluntly as Mauron: “Bitcoin has no native yield, so for miners, sovereign investors, and large funds, selling volatility has become a way to generate income from their holdings.” Gold pays no dividends, but at least it shines. Bitcoin pays nothing. And for those holding massive positions, that is a problem. A billion-dollar asset simply sits there, generating no cash flow. So what does smart money do in this situation? It starts selling the one thing it has in abundance — volatility.

Selling Bitcoin options has become one of the market’s dominant strategies. Miners who need cash to pay electricity bills sell calls. Funds that need yield for investors sell puts. Sovereign investors who entered Bitcoin as a strategic reserve are also happy to collect option premiums. And the result is clear: every time the price attempts a sharp upward move, option sellers suppress the spike. Every time it tries to fall, the same process happens in reverse. The market is being artificially sedated by the very players who were supposed to bring maturity and stability.

The Effect of Suppressed Volatility

This phenomenon is self-reinforcing. As volatility falls, options become cheaper. As options become cheaper, sellers are forced to sell even more contracts to generate the same income. And as they sell more, they suppress price movement even further. A feedback loop emerges, dragging Bitcoin into an increasingly narrow range.

For traders accustomed to the wild swings of the crypto market, this is an unfamiliar and frustrating reality. Strategies that worked during the era of high volatility — breakout trading, trend following, scalping sharp moves — no longer generate profits. The market becomes boring, and a boring market loses its audience. Retail traders migrate to wherever the action is: AI stocks, Korean and Japanese indices, anywhere but sitting around watching Bitcoin move sideways.

Forty Percent Below the Peak: A Price That Cannot Wake Up

Seventy-seven thousand dollars is not a price that should inspire despair. Just two years ago, Bitcoin would have celebrated euphorically at these levels. But context changes everything. Being forty percent below an all-time high is too deep a drawdown to be called simple consolidation before another breakout. It is a serious correction, and the market needs time to digest it.

Bulls hoped that spot ETFs would become the catalyst pushing Bitcoin toward new highs. To some extent, that did happen — the ETF launch triggered a powerful rally. But then inflows dried up, and by May they had turned into outflows. Institutional demand proved not to be infinite. Now the market is searching for a new narrative, a new story capable of attracting capital back in. So far, it has not found one.

The Iranian negotiations, which could have become such a catalyst, are sending mixed signals. On one hand, hopes for peace reduce inflation expectations and should theoretically support risk assets, including Bitcoin. On the other hand, declining geopolitical risk premiums remove one of Bitcoin’s key arguments as a hedge asset. The result is a closed loop where every macro factor can be interpreted both positively and negatively.

Competition for Attention

Bitcoin is experiencing what can only be described as an identity crisis. It is no longer the exciting new asset promising to reinvent the financial world. It is more than fifteen years old now. It has survived multiple boom-and-bust cycles. It still has a loyal community of believers, but attracting fresh capital now requires either new all-time highs or a compelling new narrative. At the moment, it has neither.

Meanwhile, the AI sector is writing a new story every single day. Every Nvidia earnings report, every new SK Hynix record, every breakthrough in generative AI acts like a magnet for capital. And crypto, with volatility sitting at a nine-month low, simply cannot compete for the attention of investors looking for growth right here, right now.

This does not mean Bitcoin is dead. It means Bitcoin is asleep. And like any sleeping giant, it can wake up at any moment. Perhaps the trigger will be an unexpected regulatory breakthrough. Perhaps a new wave of institutional adoption. Perhaps some geopolitical shock that once again pushes the world toward defensive assets. But until those triggers arrive, Bitcoin is likely to remain trapped in its narrow range — sedated by volatility sellers and abandoned by the hot money that has migrated into AI.

This is not the end. It is simply a pause. But it is a pause that has already lasted nine months.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.