Planning and Psychology of Exchange Trading

Exchange trading is an industry where a single trade can yield quite substantial profits. Many investors experience these winning streaks from time to time. However, to become truly successful and earn consistently, you need to deeply understand your own statistics and actively take steps to improve your performance metrics.

The reality is that any trading system involves several critical parameters beyond its basic profitability over a given period. These include:

-

Trading frequency: How often you execute setups.

-

Win/Loss/Breakeven ratio: The average proportion of profitable, losing, and zero-sum trades.

-

Risk-to-reward metrics: The average profit per trade (Take Profit) versus the average loss per trade (Stop Loss).

You cannot simply review these parameters once before launching a system; you must track them dynamically. Markets are highly fluid and constantly changing.

Over time, these structural shifts accumulate and quietly render the original versions of your trading systems obsolete.

To notice these market shifts and adapt to them, you must learn to work with your own statistics. Think of it as adjusting the gears in your trading system based on hard performance data. Your trading journal will clearly highlight both your strengths (which you should maximize) and your weaknesses (which you must figure out how to minimize).

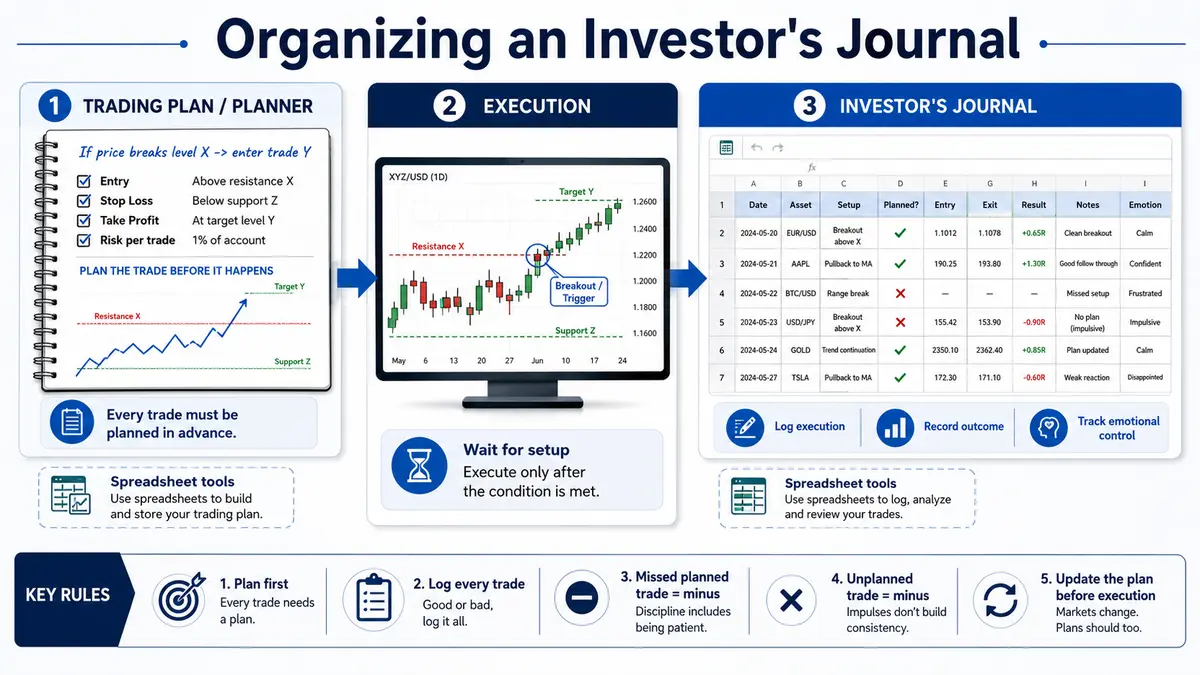

Organizing an Investor’s Journal

Microsoft Excel or Google Sheets is the best tool for keeping a trading journal. A trading plan and an investor’s journal go hand in hand: the trading plan represents your system’s blueprint, while the journal acts as the ultimate scorecard for both the system’s efficiency and your ability to execute it without emotional interference.

Furthermore, combining your plan and journal keeps you from falling into random trading (executing trades on a whim) — a trap that ruins many beginners.

You cannot map out a rigid daily trading plan before the market opens; every trading day writes its own unique, unpredictable story. However, every individual trade must be planned in advance.

If you identify a potential setup, write it down in your planner: “If price breaks through level X, execute trade Y,” and wait for that exact moment. Once the trade triggers, log the execution and its final outcome into your journal. Essentially, your initial strategy goes into the planner, while the actual result and characteristics of the trade are recorded in the journal.

Note: The absence of a planned trade must also be logged, but with a major logical minus sign. This forces you to acknowledge that you violated your own system. Unplanned trades must be logged with a minus sign as well.

Keep in mind that plans can change. However, you must update the plan first, and only then execute trades based on that new strategy before logging them in the journal — never the other way around.

Your journal is an arbitrary, custom tool designed to track your trading dynamics. To fill it out, you can access your entire transaction history under the Account History tab of your trading platform.

The Psychology of Exchange Trading

Humans are hardwired to feel emotions, but for an investor, unmanaged emotions are the ultimate financial enemy. If you cannot discipline your emotions, this business will not yield a steady income. The individuals who thrive in financial markets are those who have mastered self-control in any market condition.

Understanding human psychology is the key to decoding market movements. On the trading floor, everyday human desires and fears are magnified. Core emotions — greed, fear, and hope — exert an incredibly powerful influence on investor behavior in the fast-paced rhythm of exchange trading. Recognizing your own psychological traits, strengths, and flaws will save you from catastrophic losses. If you couple self-awareness with the ability to accurately assess the psychological state of the market crowd, long-term success is virtually guaranteed.

Greed

Greed is the primary engine that drives us to operate in financial markets. If your greed is too low, you will execute very few trades and miss out on great market setups. Ultimately, greed acts as a powerful motivator to trade, which manifests in two ways:

-

Rational motivation: Typically seen in novice investors before their first market exposure, and consistently present in the workflow of seasoned professionals.

-

Irrational motivation: Driven by a gambler’s high. While almost every investor experiences this, professionals masterfully control the thrill, whereas amateur traders become slaves to it.

Market Example: > An investor opens a long position on Tesla after a thorough analysis and sets a logical Take Profit level. The price begins to climb. If greed takes over, the investor might arbitrarily delete the Take Profit order without any objective reason, hoping for endless gains.

In reality, the market will likely hit a key resistance level and violently reverse, leaving the investor with a much smaller profit than originally planned—or worse, a loss. To counter greed, never alter your exit strategy during a live trade unless an objective, structural market shift occurs.

An internal thought like “I just want to make more money on this specific move” is never an objective reason.

Hope and Expectations

The hope for a profitable outcome is another major driver behind trade execution.

Naturally, the core purpose of any work is the financial return. However, when hope completely overrides cold calculation, you risk blinding yourself to reality during your market analysis. Hope must always remain entirely subordinate to both mathematical probability and controlled greed.

Fear

Fear grips you the moment you start losing money. In many individuals, fear triggers cognitive paralysis: they fail to cut losses in time and watch their capital evaporate.

In a critical market pivot, it is infinitely better to act decisively rather than sit idle watching your financial future vanish alongside a plummeting price ticker. Execute your plan exactly as it was written before the trade went live (and before the fear kicked in), and panic will lose its grip on your decision-making.

Common Trading Myths

The Myth of the Lucky Amateur

A successful investor is a strict realist. They soberly evaluate market conditions, suppress emotional impulses, and build actionable plans. Illusions have no place in a professional’s portfolio.

An amateur, by contrast, panics after a few bad trades and minor losses. Their perception of the equity markets quickly becomes warped by cognitive biases.

Struggling traders fill their heads with fantasies about buying, selling, and picking the perfect stock. This disconnect from reality actively blocks exchange success.

Procrastination Trait: Losers constantly invent excuses for why they aren’t succeeding or why they haven’t started investing yet. They perpetually push immediate action into the future: “Once I figure out exactly how everything works, I’ll start… Once I learn a bit more, I’ll invest… Once I get my next paycheck, I’ll set up the account…”

Do not deceive yourself. People who fall into this loop will never actually start. A successful investor identifies these internal illusions and discards them immediately, prioritizing a sober assessment of reality over wishful thinking.

The Myth of Trading Secrets

Many struggling traders firmly believe that successful investors possess some hidden, esoteric secret or a holy grail strategy. This exact fantasy ensures that financial consultants and vendors selling “ready-to-use” black-box trading systems never run out of clients. A demoralized investor will frequently burn through their remaining trading capital buying expensive software, indicator packages, and algorithms that claim to “flawlessly” analyze the market. There are no secrets — only discipline, risk management, and statistical edges.

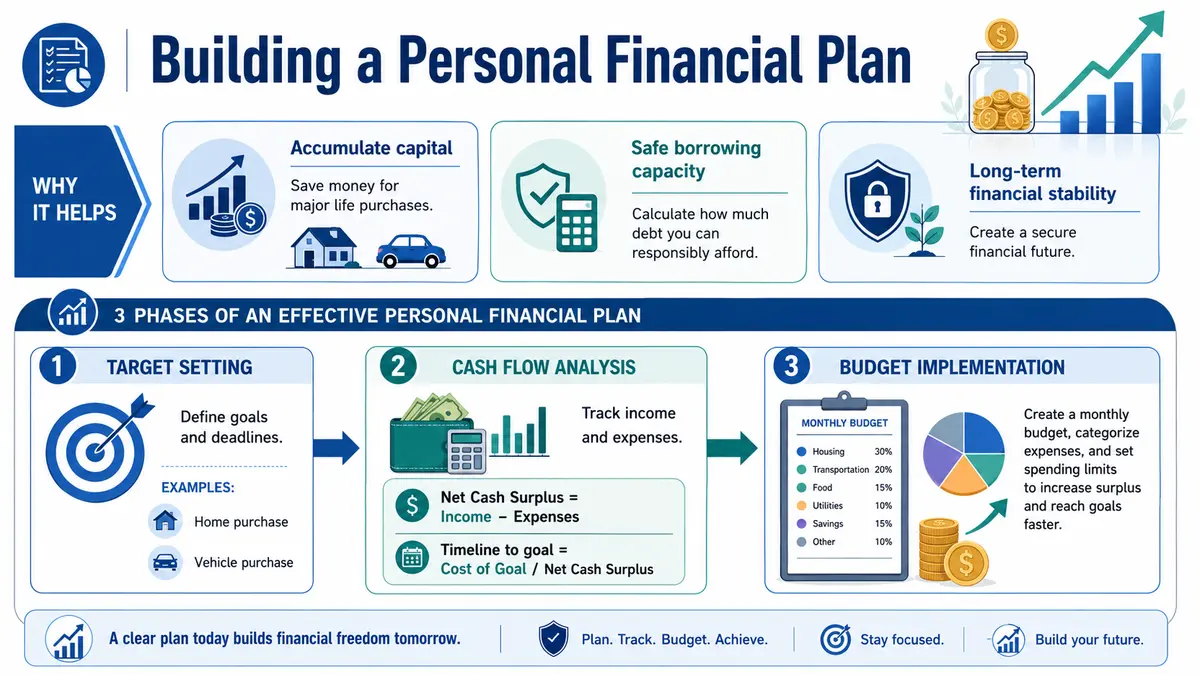

Building a Personal Financial Plan

Personal financial planning allows you to leverage your economic resources with maximum efficiency. It helps you:

-

Accumulate capital for major life purchases.

-

Calculate your actual, safe borrowing capacity.

-

Establish long-term financial stability.

Effective personal financial planning consists of three distinct phases:

-

Target setting: Explicitly defining your goals and timelines (e.g., buying a home, purchasing a vehicle).

-

Cash flow analysis: Tracking your current income and expenses. Calculate your net cash surplus (Income minus Expenses) and determine the exact timeline required to hit your goals under current conditions (Cost of Goal divided by Net Cash Surplus).

-

Budget implementation: Drafting a budget for a set timeframe (typically monthly). This involves categorizing expenses and setting strict caps on discretionary spending to optimize your net cash surplus and compress the timeline to your financial goals.

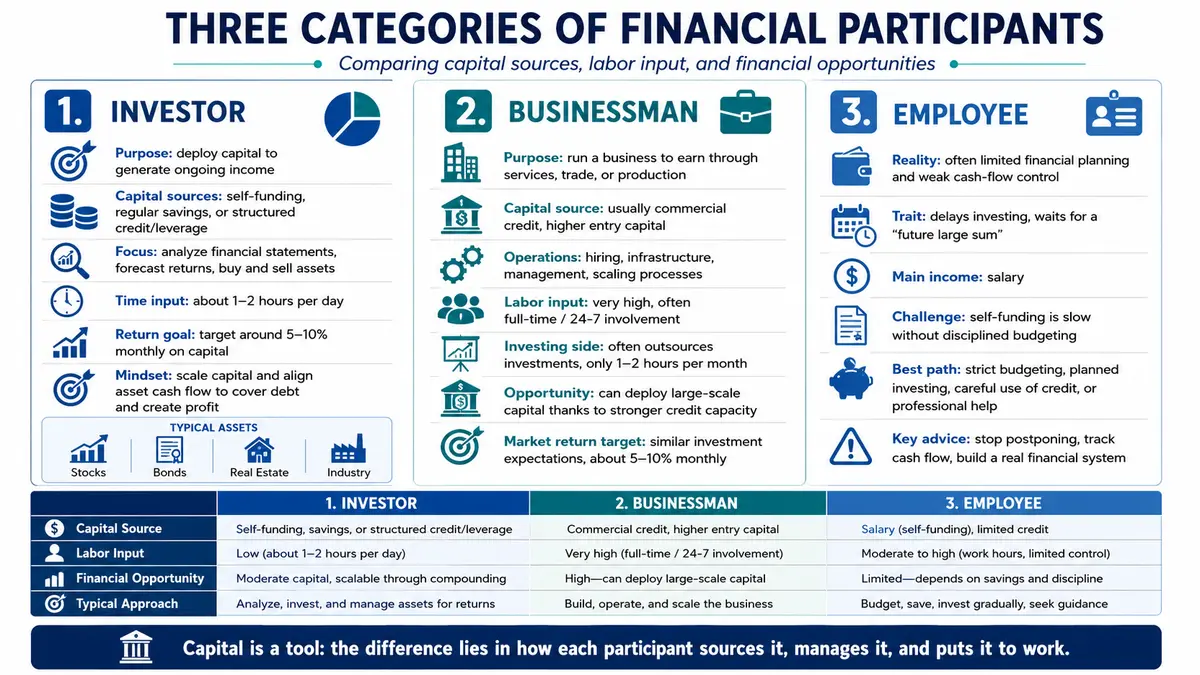

Three Categories of Financial Participants

In the broader economic landscape, individuals generally fall into one of three distinct financial archetypes. Let’s break down the labor inputs, opportunities, and profit expectations for each group.

1. The Investor

At its core, investing is the deployment of capital to generate ongoing income. This is split into financial investments (purchasing equities, bonds, or assets) and real investments (deploying capital into industry, construction, or real estate). Simply put, investing is placing capital where it can actively multiply.

Anyone can become a private investor — whether you are a middle manager, a healthcare professional, a teacher, a student, or a retiree. You do not need a specialized financial degree. For most, it is a highly effective way to build a reliable stream of secondary income.

Investment capital generally stems from two sources:

-

Self-funding: Investing via personal savings or regular allocations from a salary. In practice, this is often challenging for beginners, as very little disposable income remains at the end of the month without disciplined budgeting.

-

Credit financing: Acquiring investment capital through structured loans or leverage. If your potential asset returns safely outpace the interest rate on the debt, leverage becomes a powerful tool to accelerate wealth creation.

Full-time investors who do not rely on a traditional job manage their cash flows entirely by allocating borrowed capital across diverse asset classes to maximize yield.

-

Labor Inputs: Finding prospective investments (analyzing corporate financial statements), forecasting returns, sourcing optimal credit options across various institutions, and executing the purchase/sale of securities. When optimized, an investor spends a maximum of 1 to 2 hours per day on these tasks.

-

Profit Expectations: Active investors generally target returns of 5% to 10% per month on deployed capital. For instance, if you aim to generate a steady monthly net profit of $1,000, you should be prepared to deploy an investment capital base of at least $10,000.

-

Mindset: An investor never caps their earning potential. Their mindset focuses entirely on scale: finding new ways to secure low-cost capital and moving it into high-performing assets.

How Investors Handle Debt: An investor meticulously aligns their cash flows so that asset appreciation, dividend yields, and distributions completely cover loan obligations while leaving a healthy net profit spread. The underlying corporate businesses they own essentially pay off the investor’s debt.

2. The Businessman

An entrepreneur or businessman operates a commercial enterprise to capture profits through services, trade, or manufacturing.

-

Capital Sourcing: Unlike an investor who can start small with micro-savings via self-funding, a business carries an incredibly high barrier to entry. Launching even a modest small business often requires a minimum upfront capital injection of $50,000 to $100,000. Consequently, self-funding is rarely enough; almost all businesses are built on commercial credit.

-

Operational Profile: Unlike a pure investor who simply allocates capital, a businessman must directly manage operations, handle recruitment, build infrastructure, and scale business processes. Most business owners seek investment portfolios because their primary business eventually hits a growth ceiling, faces labor constraints, or yields surplus cash that is better off compounding in the markets rather than sitting idle.

-

Labor Inputs: Running a business requires a intense commitment—often 24 hours a day, 7 days a week. However, on the investment side of their wealth, a businessman’s time commitment is incredibly low (often just 1 to 2 hours per month). This is because they typically outsource portfolio management to institutional investment firms.

-

Expectations & Leverage: Their target market returns match the investor’s (5% to 10% monthly), but businessmen possess the corporate credit profiles to deploy capital at a scale many individual investors cannot match.

3. The Employee

Compared to investors and businessmen, regular corporate employees who lack financial education frequently find themselves in a precarious economic position.

-

The Reality: In 90% of cases, structured financial planning is entirely non-existent. There is very little functional understanding of how cash flows are generated or directed.

-

The Trait: The employee often behaves as a passive dreamer, operating under the illusion that they will magically accumulate a massive lump sum in the distant future before they begin to invest. Without fixed planning, this milestone is rarely achieved.

-

The Fix: Because self-funding out of a standard paycheck yields slow results, an employee’s fastest path to market exposure involves strict budgeting, utilizing calculated credit lines, or partnering with established investment firms to automate their wealth accumulation.

If you are currently operating within the employee framework, you must immediately drop the habit of putting off your financial setup. Every day spent hesitating is a day of compounded returns lost. Learn to treat capital as a tool, track your cash flows, and build a definitive framework for your capital.

Immediate Financial Planning Steps

-

Establish a rigorous budget: Identify exactly where every dollar of your income goes. Build a comprehensive budget mapping your fixed monthly outlays against income, and explicitly allocate a set percentage toward immediate savings and investments.

-

Aggressively clear toxic debt: If you carry high-interest consumer debt or credit card balances, crush them immediately. High interest charges act as a severe drag on your net worth. Build a structured repayment plan to free up your cash flow for asset accumulation.

-

Build a liquid emergency fund: Establish a financial safety net capable of covering 3 to 6 months of essential living expenses. Keep these funds in a highly liquid, low-risk vehicle (like a High-Yield Savings Account) to ensure you never have to liquidate your long-term investments during an unexpected life emergency.

-

Analyze asset classes: Dedicate time to studying primary investment vehicles: equities, corporate and government bonds, index funds, and real estate. Align these tools with your personal risk tolerance.

-

Diversify systematically: Never concentrate all your capital in a single asset or sector. Broadly allocate your funds across different asset classes and global markets to insulate your aggregate portfolio from sharp market drawdowns.

-

Automate your allocations: The most reliable way to scale wealth is through regular, long-term capital deployment. Set up automated monthly or quarterly transfers into your investment accounts to harness the power of dollar-cost averaging.

-

Commit to continuous education: Investing is an ongoing learning curve. Allocate time to study market structures, corporate financial reports, and macroeconomics. Deeper knowledge directly translates to superior financial decisions.

-

Scale your risk profile gradually: Markets are inherently volatile. If you are a beginner, start with conservative, low-beta instruments. As your experience, capital base, and market literacy grow, you can systematically scale into more aggressive, high-yield asset classes.

Planning for the Future

Clearly define your long-term financial milestones — whether that means buying a home, funding an education, securing an early retirement, or achieving total financial independence. Break these goals down into clear, actionable steps.

Review and adjust your personal financial plan at least once a year to keep it perfectly aligned with your evolving career trajectory and life milestones. Financial success is never an accident; it is the natural byproduct of patience, daily discipline, and continuous learning. Start executing today, regardless of your current income bracket. Every small, calculated financial decision you make right now compounds significantly over time.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.