Financial Reporting

Financial reporting is a crucial organizational document containing information about a company’s financial performance, its income and expenses, property, and transactions made over a specific period (usually a quarter, half-year, nine months, and a year). For clarity, the financial report provides data for the current reporting period alongside the same period from the previous year (for example, the first half of 2026 and the first half of 2025). For investors, the report is the primary source of information used to evaluate business efficiency and decide whether to invest money in the company’s shares. Below, I’m explain how financial statements are generated and submitted.

Purpose of Creating Financial Statements

Financial statements are the foundation for making managerial decisions. The main purpose of compiling financial statements is to gather up-to-date and reliable information about the organization’s performance and financial position. Ultimately, this information helps the business owner understand which direction the organization should develop and what strategy to choose. Such information is collected for the entire calendar year in accounting registers and is reflected in the financial statements.

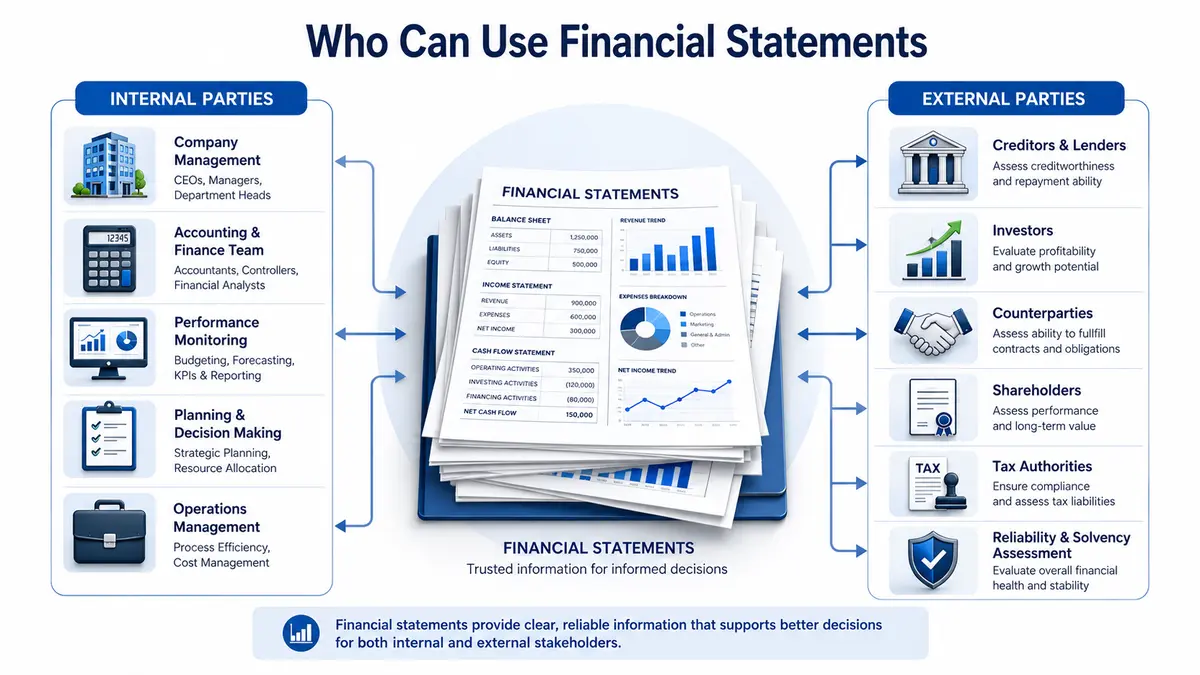

Who Can Use Financial Statements

-

Internal parties — organization employees: economists, accountants, managers, CEOs, and others who rely on reporting and accounting information to improve the company’s financial results.

-

External parties — creditors, investors, counterparties, shareholders, tax inspectors, etc. Reporting helps them assess the organization’s financial position, its reliability and solvency, and the completeness of its fulfillment of obligations to the budget and counterparties.

Components of a Financial Report

-

Balance sheet;

-

Income statement (Profit and loss statement);

-

Cash flow statement;

-

Statement of changes in equity;

-

Notes to these statements.

In addition to the main indicators, the preparers of the financial report also try to reflect all corporate events that occurred in the company over the set period, details about company management, litigation, and their future prospects and strategies.

Financial Statement Components for Commercial Organizations

-

Balance sheet — reflects the structure of the organization’s assets and liabilities;

-

Statement of financial results — shows what results the organization achieved over the year and what influenced them;

-

Statement of changes in equity — includes data on net assets, capital movement, and various adjustments;

-

Cash flow statement — shows how much money the organization received or spent within its investing, financing, and operating activities;

-

Notes to the financial statements — explain individual indicators of the listed reports.

Reporting Standards

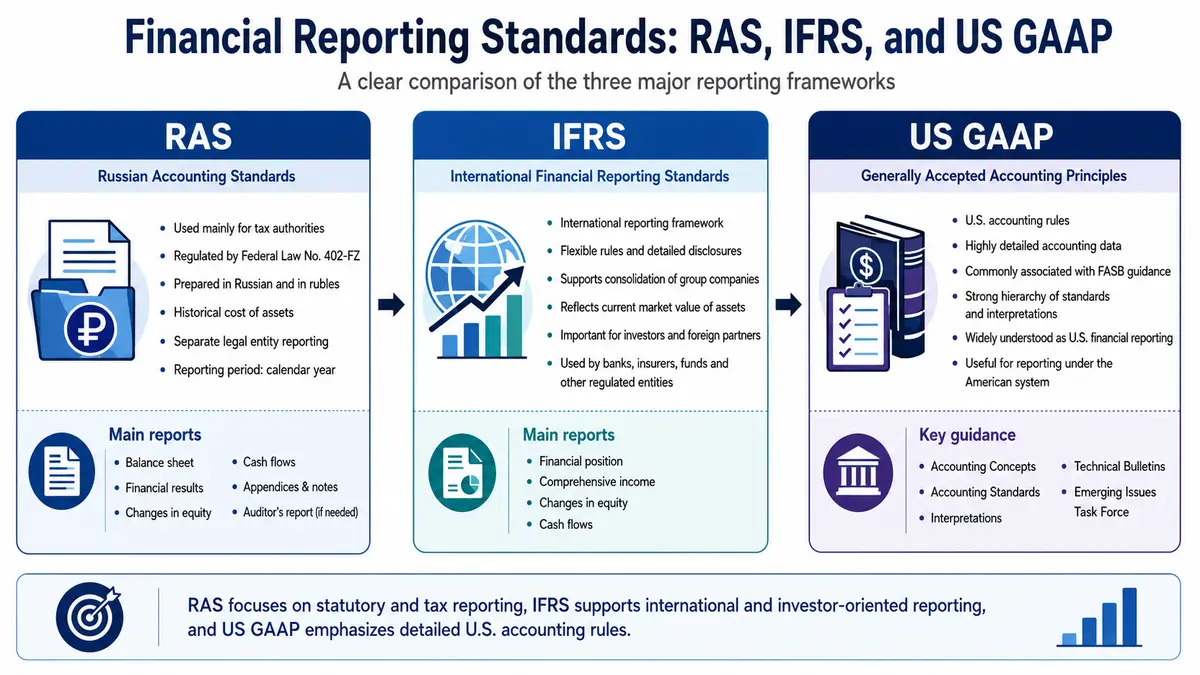

Every country has its own reporting standards. For example, in Russia, there is the RAS standard (Russian Accounting Standards); in the USA — US GAAP (Generally Accepted Accounting Principles); and in the UK — UK GAAP. To compare two companies from different countries, there are International Financial Reporting Standards (IFRS), which are used by both foreign and Russian companies.

Russian Accounting Standards (RAS)

This is reporting that is primarily formed for tax authorities and used to calculate taxes. The rules for compiling this form are established by the Federal Law on Accounting No. 402-FZ dated 06.12.11. This is a relatively brief report (less than ten pages) that indicates only the main metrics (profit, revenue, balance sheet, etc.) — without evaluating operations in terms of their overarching benefit for the company and without consolidation (each legal entity reports solely for itself). RAS relies on the historical cost of the company’s assets without adjusting for changes in market value.

It applies to companies in almost all areas of activity, except for banking system organizations. The specific accounting and reporting rules for banks are established by the Central Bank of Russia.

Features of RAS:

-

Reports are compiled in rubles and in Russian;

-

Accounting is maintained in accordance with a unified chart of accounts;

-

If a company cooperates with foreign business partners, a line-by-line translation of all forms is required;

-

The reporting period is a calendar year.

Reports included in RAS:

-

Balance sheet;

-

Statement of financial results;

-

Statements of changes in equity and cash flows;

-

Standardized appendices and explanatory notes;

-

Auditor’s report (if necessary).

International Financial Reporting Standards (IFRS)

IFRS represents the financial reporting of companies according to international standards, compiled using more flexible rules. It also contains financial indicators and can consist of dozens or even hundreds of pages of notes regarding the metrics for the reporting period. In such a report, a group of companies can, for example, consolidate the financial results of its subsidiaries and branches. It is submitted by credit and insurance companies, non-state pension funds, management companies of investment funds, mutual investment funds, Federal State Unitary Enterprises (FSUEs), joint-stock companies with federally owned shares (approved by the Russian Government), and clearing organizations. Additionally, IFRS reflects the current market value of a company’s assets.

Reports included in IFRS:

-

Statement of financial position as of the reporting date;

-

Statement of comprehensive income for the reporting period;

-

Statement of changes in equity;

-

Statement of cash flows.

IFRS reporting is typically of great interest to investors and is vital when cooperating with foreign partners and counterparties.

Generally Accepted Accounting Principles (US GAAP)

GAAP stands for Generally Accepted Accounting Principles. Broadly, it is a general term applicable to any national economy that has developed specific accounting rules. Thus, in the context of Russia, GAAP would theoretically be the combination of the aforementioned laws and regulations governing Russian accounting.

However, there is another specific meaning frequently associated with the acronym GAAP. It is used in relation to US accounting rules — US GAAP. Reporting and general accounting principles within this system require a high degree of detail in accounting data. American GAAP standards involve several tiers in the hierarchy of regulatory documents, which may be prepared at different times by various professional organizations.

Companies keeping records under the US GAAP system are generally guided by documents developed by the Financial Accounting Standards Board (FASB), namely:

-

Statements of Financial Accounting Concepts (defining the basic principles of the accounting process);

-

Statements of Financial Accounting Standards (the core rulebook);

-

Interpretations supplementing the basic standards;

-

Technical Bulletins (practical examples or explanations on specific applications of accounting standards);

-

Statements of the Emerging Issues Task Force (addressing non-standard situations not covered by the documents above).

Given the traditional use of the term GAAP, it is generally understood to mean financial statements prepared specifically in accordance with the rules of the American system.

Key Indicators of Financial Reporting

While there are many metrics in any company’s financial report, there are several core indicators you should focus on during analysis:

-

Revenue — the money a company receives from selling its goods and services over a certain period. Companies may record revenue differently in their reporting: fully (at the time of sale), deferred (gradual recognition over the term of a contract), or partially.

-

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) — the company’s profit before paying loan interest, taxes, and depreciation/amortization. EBITDA demonstrates a company’s ability to service its debt and cover capital expenditures (buying equipment, transport, real estate, etc.).

-

Net profit — the difference between a company’s income and expenses. This is the amount remaining in the company’s accounts after settling with customers and paying all expense items (salaries, taxes, etc.).

-

Free cash flow — the difference between net cash flow from operating activities and the company’s capital expenditures. This represents the earned money that remains at the company’s disposal after adjusting for non-cash (paper) items.

-

Debt obligations — the amount of funds the company has borrowed from a bank or, for example, from its suppliers. Debts can be long-term (maturity over 12 months) or short-term (under 12 months).

-

Net debt — the difference between all debt obligations and the company’s highly liquid assets.

How the Report Can Be Useful to an Investor

The most important report for an investor is the IFRS report. It is created not only for submission to government agencies but also to provide investors with actionable insights. In an IFRS report, you can find the consolidated results of an entire group if the company operates as a holding.

Beyond the numbers, companies use IFRS reporting to describe what influenced the dynamics of their financial indicators and to provide forecasts for the next period.

Furthermore, financial statements prepared under international standards often calculate valuation multiples, debt load ratios, business efficiency indicators, and more. A company may also report operational indicators specific to its industry (e.g., raw material extraction volumes or utilization rates). Experts note that these are essential to review, as they strongly indicate business efficiency.

How to Analyze Financial Statements

When analyzing a company’s income statement, it is crucial to separate cash items from paper items. Cash income and expenses lead to changes in the company’s actual real funds, whereas paper items only reflect certain accounting processes without affecting cash positions.

Paper items in a report include depreciation, exchange rate differences, disposal of fixed assets, and the share in the profit of associated organizations. Some paper items are reflected in the income statement (e.g., exchange rate differences), while others, such as depreciation, can be found in the cash flow statement or the notes to the financial statements. These items significantly impact the size of the company’s stated net profit.

Example of Analyzing Apple’s Financial Report

To find a company’s reporting, you need to visit its official website. In this case, we will use Apple as an example.

-

After landing on the official website, look for the tab dedicated to investors (on various official websites, this might be named “Investors,” “Investor Relations,” “Investors and Shareholders,” etc.).

-

Once in the “Investors” section, locate the “SEC Filings” tab (an SEC filing is a financial report or other official document submitted to the Securities and Exchange Commission).

-

The “SEC Filings” tab houses all the company documents needed for gathering information. There, you can select the required document—such as annual reports (Annual Filings) on Form 10-K, or quarterly reports (Quarterly Filings) on Form 10-Q.

-

Besides selecting the document type, you can also filter by the specific time period you are interested in.

-

You can choose the format in which you want to view the report; the simplest is a PDF file.

-

Select the annual report for 2025.

Once you open the annual report (10-K), you can begin studying the company in depth. The report contains all necessary information, ranging from the company’s core operations to detailed financial metrics and ongoing litigation.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.