Inflation and the Federal Funds Rate

What is Inflation

Inflation is the general increase in the prices of goods and services, resulting in the depreciation of money and a decline in its purchasing power. Unlike seasonal price fluctuations, inflation is persistent and long-term. The nominal value of money remains unchanged — $100 a year ago is still $100 today — but its real purchasing power diminishes over time.

Example: > A year ago, $10 could pay for three public transit rides; today, it only pays for two. This is a direct manifestation of inflation.

The opposite of inflation is deflation — a decrease in the general price level of goods and services, which causes purchasing power to rise. In modern economies, deflation is rare and usually short-term, often tied to seasonal factors.

Example: > Prices for vegetables, fruits, and grains usually drop immediately after the harvest season. Prolonged deflation is characteristic of very few countries. Today, Japan’s economy frequently serves as a textbook example of deflationary pressures (historically hovering around -1%).

The inflation rate in the US is a public metric available to anyone. Inflation data is typically tracked by year and month. You can view current and historical inflation data on the Bureau of Labor Statistics (BLS) website or through various financial portals. Link: usinflationcalculator.com or bls.gov

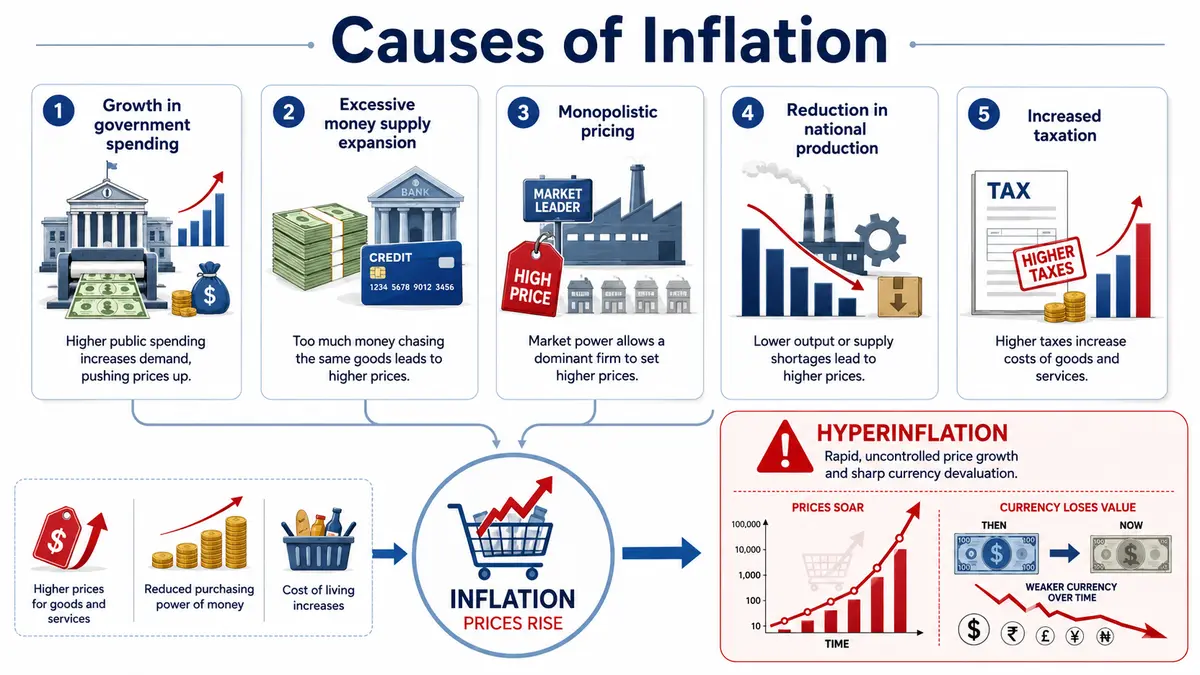

Causes of Inflation

Economic science identifies several primary causes of inflation:

-

Growth in government spending: To finance this, the government may rely on issuing more money, expanding the money supply beyond the actual needs of commodity circulation. This is most pronounced during wars and economic crises.

-

Excessive expansion of the money supply: This happens through mass lending, where the financial resources for credit come from issuing unbacked currency rather than from actual savings.

-

Monopolistic pricing: Large firms dominating a market can arbitrarily dictate prices and their own production costs, which is especially common in commodity and raw material sectors.

-

Reduction in national production: If the money supply remains stable but the real volume of goods and services shrinks, prices will rise because the same amount of money is chasing fewer products.

-

Increased taxation: The introduction of new government taxes, duties, and excises while the money supply remains stable.

Hyperinflation is a rapid, out-of-control rise in prices that leads to a sharp devaluation of currency. Various economic sources define it as price growth exceeding 50% to 100% per month, or a cumulative increase of over 100% across three years.

Because inflation devalues a country’s currency, a nation with a high inflation rate will see its currency depreciate over the long term against the currency of a country with a lower inflation rate.

The Federal Funds Rate

The Federal Funds Rate (the US equivalent of a central bank key rate) is the primary tool of the Federal Reserve’s monetary policy. It plays an informational and signaling role, indicating the overall direction of the country’s economic strategy.

Depending on how the Federal Reserve manages this target rate, monetary policy can be classified as “tight” (restrictive) or “loose” (accommodative). This benchmark dictates the interest rate at which depository institutions trade federal funds with each other overnight.

The target range for the Federal Funds Rate is established by the Federal Open Market Committee (FOMC) eight times a year according to a set schedule. However, in emergency situations, the Fed can intervene and adjust the rate before a scheduled meeting.

Changes to this rate directly influence lending and economic activity. In the long term, it helps the Fed achieve the ultimate goals of its monetary policy: price stability, maximum employment, and low, manageable inflation.

You can view the current target rate directly on the Federal Reserve’s official website. Link: federalreserve.gov

Federal Reserve Rate Decisions

The FOMC dictates the target federal funds rate eight times a year. Decisions are heavily weighed during four key quarterly meetings, alongside four interim meetings held in between.

Following each meeting, the Federal Reserve publishes a press release outlining its rate decision. After the main quarterly meetings, the Fed also releases its Summary of Economic Projections, and the Federal Reserve Chair holds a live press conference to explain the decision, provide commentary, and answer questions from financial journalists.

Effects of the Federal Funds Rate

The influence of the target rate on the broader banking sector is known as the “monetary policy transmission mechanism.” By conducting either “stimulative” or “restrictive” policy, the Federal Reserve essentially manages the cost of money in the US economy.

Changes to this rate dictate the trajectory of bank loan and deposit interest rates.

However, this transmission is not a strict 1-to-1 ratio: in the corporate lending segment, about 60% to 80% of the rate change is passed on to businesses, while in the retail sector (consumer loans and deposits), usually only 20% to 40% of the shift is reflected.

Commercial Banking and Lending

A commercial bank (e.g., Chase, Bank of America, Wells Fargo, Citibank) is a credit institution that executes financial operations for businesses and individuals. These services include processing payments, attracting deposits, issuing loans, providing credit cards, and offering installment plans.

From a bank client’s perspective, lending means borrowing money under specific, individualized terms outlined in a contract. This agreement explicitly states the interest rate, the loan term in months, the exact monthly payment amount, the due dates, and any rules regarding early repayment.

Popular Types of Loans

-

Personal loans

-

Mortgages (Home loans)

-

Auto loans

-

Credit cards

-

Installment plans (Buy Now, Pay Later)

Types of Loan Collateral

-

Unsecured personal loans: The most common form of consumer borrowing in the US. This is highly popular among the public because it requires no physical collateral.

-

Co-signed loans: A loan guaranteed by a co-signer, usually a relative or close friend of the primary borrower. In modern practice, this is becoming less popular, as few people want to assume financial and legal responsibility for someone else’s debt.

-

Secured loans (Asset-backed): The collateral is usually a vehicle or real estate (like a Home Equity Loan). Because unsecured personal loans are relatively easy to obtain for those with good credit, secured loans are mostly limited to traditional auto loans and mortgages. However, the massive advantage of a secured loan is the borrowing limit. A bank is willing to lend significantly more money against hard collateral — often five times or more than they would issue for a standard unsecured loan.

The Total Cost of a Loan

The total cost of a loan (often reflected in the APR — Annual Percentage Rate) encompasses all payments the borrower must make, the sizes and deadlines of which are known the moment the contract is signed. Financial institutions are legally mandated by the Truth in Lending Act to disclose the total cost of the loan before the borrower signs the agreement. Banks must provide a clear breakdown of exactly what makes up the final payout.

Calculating the Real Annual Cost of a Loan:

-

Determine the exact amount you want to borrow. Let’s use $10,000 as an example, using a calculator from a site like Bankrate.com.

-

Determine the loan term. It is often safest to calculate based on a longer term, such as 5 years (60 months), so the monthly payment remains minimal and doesn’t heavily strain your budget.

Link: Bankrate.com

-

Taking a $10,000 loan over 5 years (60 months) results in a monthly payment of roughly $259.40. Multiply that monthly payment by the total number of payments ($259.40 × 60) to find the absolute total cost of the loan over 5 years = $15,564.

-

Subtract the principal loan amount ($10,000) from the total cost ($15,564) to find the pure cost of borrowing the money over those 5 years = $5,564.

-

Divide that borrowing cost ($5,564) by 5 years to find the cost per single year = $1,112.80.

-

Finally, divide the 1-year cost ($1,112.80) by the principal amount ($10,000) to find the real annual cost percentage = 11.13% per year.

This formula is incredibly simple. You can now independently calculate the true cost of any loan amount over any timeframe.

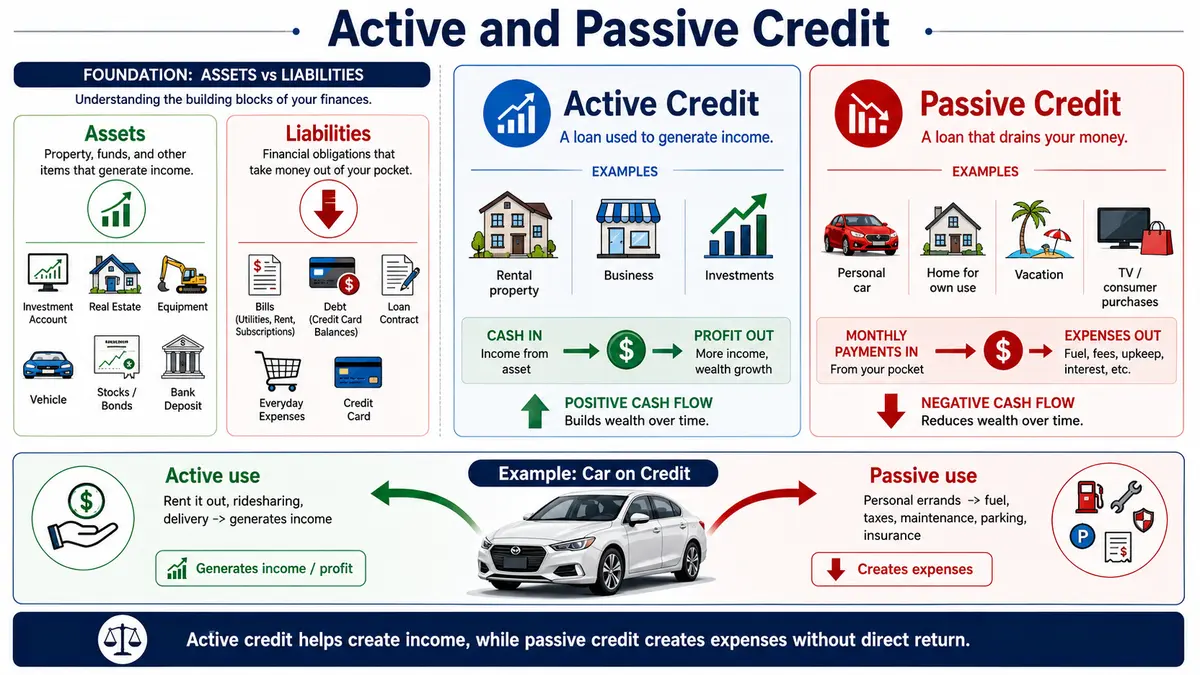

Active and Passive Credit

To properly understand active and passive credit, you first need to understand what an “Asset” and a “Liability” are in personal finance.

-

Assets: Property, funds, and any other items that actively generate income. This includes cash in investment accounts, commercial equipment, transport vehicles, real estate, accounts receivable, raw materials, intellectual property licenses, high-yield bank deposits, and stocks or bonds.

-

Liabilities: The totality of all your financial obligations. This is the exact opposite of an asset; it is anything that pulls money out of your pocket.

Active Credit: A loan that you use to make money; it generates income for you.

Examples include borrowing money to buy a rental property, starting a business, or investing in high-yield securities. You are leveraging bank funds to extract a profit, effectively managing your financial flow.

Passive Credit: A loan that drains your money. Examples include financing a car for personal use, taking a mortgage on a house you will live in yourself, borrowing money for a vacation, or financing a new TV. Because these funds do not generate any monetary return, they act entirely as liabilities.

Example: > When you buy a car on credit, the vehicle can act as either active or passive credit.

If you rent it out (for ridesharing, delivery services, etc.) and generate a profit, it is an active credit — it brings in income.

If you use the car strictly for personal errands, it becomes a liability. You are financially obligated to maintain it out of your own pocket: paying for gas, taxes, maintenance, parking, potential traffic tickets, and mandatory Auto Insurance.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.