Financial Multipliers

What are Multipliers

A multiple is a financial ratio comparing a company’s financial metrics to its market value. Multiples allow investors to evaluate and compare the investment attractiveness of companies that may differ in size but operate in similar business sectors.

Shares of an obscure company might yield more profit for you than Apple or Microsoft stock. To find an undervalued security, you need to compare company multiples and identify the most promising business.

Assets can be overvalued, undervalued, or fairly priced. If a stock’s current price is below its fair value, it is profitable for investors to buy it at a discount in order to capitalize on future price growth.

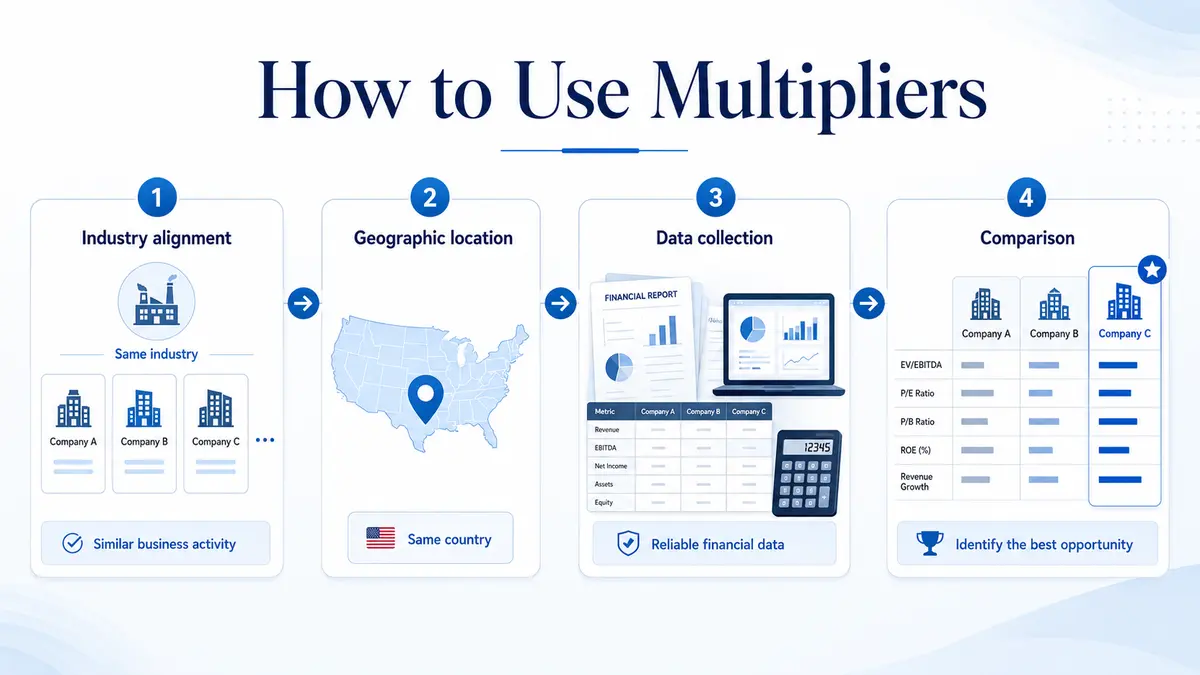

How to Use Multipliers

First, you need to select companies you are interested in investing in. However, there are a few conditions to keep in mind:

- Industry alignment: Companies must be engaged in a similar business and operate within the same industry sector. This is a mandatory condition for calculations because every industry has its own nuances, restrictions, varying tax rates, and opportunities (for example, oil companies pay high taxes).

- Geographic location: Companies must be registered in the same country. Market dynamics, legislation, and other regional factors heavily influence a company’s overall revenue.

- Data collection: Once all criteria for the companies are met, you can start calculating the multiples yourself or, more simply, find the metrics through reliable financial sources.

- Comparison: Compare the metrics and choose the most promising organization for your investment strategy.

Types of Multipliers

P/BV = Market Capitalization / Equity

This multiple shows the ratio of a share’s market price to its book value. Book value is the net asset value minus total debt. This is the money that shareholders would divide among themselves if the company were sold off after paying all debts. The multiple helps assess whether an investor is overpaying for the residual value they would receive if the company went bankrupt.

Essentially, P/BV indicates how much one dollar of the company’s equity (book) value costs on the market. It is assumed that the lower the P/BV, the greater the growth potential of the shares.

However, this multiple has one major drawback: it does not account for the company’s future earnings. For example, a loss-making company might appear to be a better investment than a highly profitable corporation if both have the same P/BV level.

Another limitation is that P/BV is not very useful for companies where human capital outweighs the value of equipment and real estate—such as software developers or media companies. Therefore, in practice, this multiple should only be used alongside other valuation ratios.

Calculation: Divide the company’s capitalization (number of outstanding shares multiplied by the stock price) by its net assets. Net assets (equity) equal total company assets minus all debts. A favorable value is less than 1 but greater than 0, indicating that the capitalization is less than the equity.

P/E = Market Capitalization / Net Income

This is the most popular ratio. It compares the value of a company with its primary performance result: profit. In the classic model, the market capitalization from the last completed trading day and the net income from the latest annual report are used for comparison.

The P/E multiple shows how many years a company needs to operate while earning the same profit to pay off its equity capital. The lower the value of this multiple, the better: it means you have an opportunity to buy shares of a promising company at a low price.

When comparing two companies, P/E demonstrates how much more investors value one dollar of net income from one company compared to the other. All else being equal, a company with a lower P/E is more attractive; there is a higher probability it is undervalued and its shares will grow faster.

There is one issue with P/E, however. Net income is a highly volatile metric. Even large companies might report a loss rather than a profit in a given quarter or year, rendering this multiple meaningless. Furthermore, profit can be manipulated using various accounting methods. While usually disclosed in annual reports, a non-professional may find it difficult to assess the impact of these changes. The next metric lacks this drawback.

Calculation: To calculate P/E, you need to know the Earnings Per Share (EPS). EPS shows how much the company earns per single share and is calculated as the ratio of net income to the number of outstanding shares. The volume of traded shares can be found on the stock exchange website or the corporation’s official website.

P/S = Market Capitalization / Revenue

The P/S multiple equals the company’s capitalization divided by its annual revenue, showing how many years of revenue the company is currently worth.

Capitalization is the market value of the company, calculated by multiplying the share price by the number of outstanding shares.

Strictly speaking, from a shareholder’s perspective, profit is more important. It is the actual money shareholders have access to after employees, suppliers, creditors, and the government have been paid. However, P/S has two distinct advantages over its “stepbrother,” P/E:

- Revenue is far less volatile compared to net profit.

- This ratio can be calculated even if the company is incurring losses and P/E becomes irrelevant.

The disadvantage of this ratio is that it does not account for operational efficiency — a loss-making company and a highly profitable one might end up having the same P/S value.

Revenue allows an investor to understand whether a product or service is in market demand. Net profit can obscure actual product demand since it is calculated after all expenses and taxes, and management can legally alter this figure through accounting adjustments. Another major advantage of P/S is that it remains useful even with negative profitability.

EV/EBITDA = Enterprise Value / Pre-tax Profit (EBITDA)

EV (Enterprise Value) is the fair value of a company, accounting for its debt burden and the cash available to pay it off. This is the price at which the company could be acquired in the event of a merger or takeover. EV is calculated by multiplying the share price by the total number of outstanding shares, adding all debt obligations, and then subtracting the company’s cash reserves.

EBITDA is the company’s earnings before interest, taxes, depreciation, and amortization. To find it, take the “Profit before tax,” add “Depreciation and amortization,” add “Interest paid,” and subtract “Interest received” using the Cash Flow Statement. EBITDA standardizes all industries and shows how much cash a company can generate before paying taxes, interest, and depreciation. This metric is more stable than net income and allows for comparing companies with differing accounting policies.

This multiple indicates how many years of EBITDA a company must generate to cover its actual market price. Comparisons should be made within the same industry, but companies with different tax and accounting systems can still be evaluated against each other.

It is very similar to P/E, with one crucial difference: in this form, it is highly relevant to creditors (such as bondholders) because it adjusts for the company’s debt.

Like P/E, a lower ratio means a higher likelihood that the company is undervalued.

Analysis using this multiple is widely utilized by bond buyers and institutional creditors. Debt is not inherently bad in this context; it is simply additional capital the company can leverage to generate profit, provided the debt burden isn’t excessive. The next multiple addresses that risk.

ROE = Net Income / Equity * 100%

This ratio measures how efficiently a company uses its shareholders’ money to generate profit. In other words, ROE is the return on equity, expressed as a percentage. The higher the yield, the better it is for the company and its investors.

Equity, found in the denominator, is the section of the balance sheet representing the value of shareholders’ assets. If a company were to sell all its assets at book value and repay all obligations to suppliers, banks, bondholders, and the government, the remaining amount would be its equity—the shareholders’ money.

Return on equity essentially illustrates how a company generates net profit using its own, non-interest-bearing funds.

Hypothetical example: If a small to-go coffee kiosk on the outskirts of a city earns the exact same profit as a high-end cafe equipped with expensive espresso machines, premium furniture, and decor, the kiosk is utilizing its equity much more efficiently.

ROE should consistently outpace the average annual interest rate on government bonds. Otherwise, it makes no sense for an investor to risk capital in an instrument with low, unguaranteed returns when they could buy risk-free assets for the same profit.

ROA = Net Income / Total Assets

Return on Assets (ROA) measures how effectively a company utilizes all its assets — both equity and borrowed capital — to generate profit.

You must compare this metric strictly against other companies in the same sector. In retail, the figure will naturally be higher due to rapid inventory turnover.

Conversely, in capital-intensive industries like mining, construction, or railways, ROA will be lower due to the massive cost of necessary equipment and infrastructure.

ROA reflects the absolute ability of a company’s assets to generate revenue, regardless of how those assets were financed. Profitability indirectly signals the maximum potential return investors can expect.

- Simple formula:

ROA = (Net Income / Average Total Assets) × 100% - Detailed formula:

ROA = ((Net Income + Interest Expenses × (1 - Tax Rate)) / Average Total Assets) × 100%

To calculate ROA, data is pulled from both the income statement and the balance sheet. Net income can be tracked for the reporting period or a trailing 12-month window. The total asset volume is usually taken at the beginning of the period or as a quarterly/annual average. In some cases, analysts use pre-tax profit or profit from continuing operations.

Performance metrics can be analyzed statically or dynamically, often visualized using line graphs. An increasing ROA over time indicates improving business efficiency. This should be contextualized within the company’s life cycle (inception, growth, maturity, decline). Alongside debt metrics, ROA helps justify whether a stock deserves to trade at a premium or a discount relative to its peers.

D/E = Debt / Equity

The core idea of the Debt-to-Equity multiple is to highlight the ratio between a company’s borrowed funds and its own capital. The numerator represents total debt, while the denominator represents total equity.

Since both components make up the company’s total assets, the D/E ratio allows an investor to understand exactly how the company is financing its operations.

- If D/E > 1: The company’s assets are primarily financed through debt.

- If D/E < 1: The majority of the company’s assets are funded by its own equity.

Consequently, a higher D/E ratio signals a heavier debt burden and an increased risk of bankruptcy. If you are concerned about a potential investment’s solvency, this is the multiple to check. It shows exactly how much borrowed money exists for every dollar of shareholder equity.

For financially robust companies, this indicator generally hovers around 1 to 1.5. A value significantly above 1.5 suggests the enterprise may be risking its financial independence. However, an excessively low level of borrowed funds might indicate missed growth opportunities — the company isn’t leveraging external financing to scale production or launch new products.

Current Ratio = Current Assets / Current Liabilities

This is the current liquidity ratio. It measures a company’s capacity to pay off its short-term obligations (debts due within one year) using its short-term assets, such as cash and accounts receivable.

- Current assets: Assets the company uses and plans to liquidate within a year (e.g., cash in bank accounts, accounts receivable, warehouse inventory).

- Short-term liabilities: Debts the company must clear within a year (e.g., accounts payable, short-term loans, taxes).

Example: Suppose “North” company has current assets of $124,911 million and its short-term liabilities are $51,100 million.

Current Ratio = $124,911 / $51,100 = 2.4

A healthy multiple usually sits between 1 and 2. A higher result implies strong liquidity and solid financial resilience. If the ratio drops below 1, it points to inefficient asset management and potential liquidity crises. However, standard norms can vary by sector; retailers, IT firms, and construction companies often operate comfortably under different benchmarks due to their unique operational models.

A healthy surplus of current assets over liabilities generally signals financial stability. However, if current assets spike suddenly, it could be a red flag for operational inefficiency — such as an inability to sell manufactured goods, leading to overstocked warehouses. A low Current Ratio strongly suggests an investor should deeply investigate the company’s cash flows and immediate debt burdens.

EV/CFO = Enterprise Value / Cash from Operations

The Enterprise Value to Cash Flow from Operations (EV/CFO) ratio evaluates a company’s operational cash flow buffer against its total enterprise value. Put simply, it estimates how long it would take the company to buy back all outstanding shares and settle all debts using only the cash generated from its core business operations.

A lower EV/CFO value generally makes a company appear undervalued compared to peers with higher EV/CFO ratios.

However, this metric is highly industry-dependent. There is no universally “good” number. In the consumer goods sector, an EV/CFO of 10.0x might be considered dangerously high, whereas, in the software industry, 10.0x might be seen as extremely cheap. All valuation multiples are relative, and deep qualitative analysis is required before concluding a firm is cheap, fairly priced, or a bubble.

Comparisons must be strictly limited to direct competitors with similar operational characteristics.

This multiple is excellent for identifying current trading multiples, comparing peer valuations, and setting target prices in equity research reports or private acquisitions. Its primary advantage is its reliability in evaluating stable, mature businesses with predictable capital expenditures.

The main drawback is that it fails when comparing companies with drastically different capital intensities. If two companies generate the exact same operational cash flow, but one requires massive ongoing capital investments to sustain it, EV/CFO will misleadingly favor the capital-intensive business. Furthermore, it ignores depreciation and amortization, artificially understating a company’s actual capital drain — a major flaw when analyzing asset-heavy industries like hospitality or airlines.

D/EBITDA = Debt / Pre-tax Profit (EBITDA)

This ratio determines how many years it would take a company to entirely clear its debt obligations if it directed 100% of its net cash flow toward repayment. A higher value indicates a crushing debt burden and a severely elevated risk of default.

Both Debt and EBITDA are pulled directly from corporate financial statements.

While there is no hard legal limit, international financial practice generally considers a Debt/EBITDA ratio of ≤ 3 to be healthy and “normal.” Companies pushing a ratio of 4 to 5 (depending on the industry) are heavily leveraged. They typically struggle to service their current debt and will find it extremely difficult to secure new loans.

In the real world, Debt/EBITDA is heavily scrutinized by rating agencies, corporate credit analysts, investment bankers, and executive management. It provides a rapid, clear snapshot of a company’s financial resilience when stacked against industry averages.

A common variation of this metric is Net Debt/EBITDA, which subtracts the company’s liquid cash and cash equivalents from the total debt pool before calculation, providing an even more accurate picture of true leverage.

Foundations and Principles of the Securities Market

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.