Morgan Stanley Against the Crowd: A Bearish Dollar View in a Year When Everyone Expects Strength

A Voice from New York: “We Are Bearish”

While much of Wall Street continues to chant “the dollar is king,” and traders around the world keep buying the U.S. currency following strong employment data while pricing in a Federal Reserve rate hike in December, a very different message is coming from Morgan Stanley’s New York office.

David Adams, Head of G-10 FX Strategy, states it plainly and without hesitation: “We are bearish on the dollar.”

This is not a cautious suggestion that “a correction is possible,” nor a diplomatic warning to “remain vigilant.” It is a clear and unambiguous signal: Morgan Stanley believes the U.S. dollar is headed lower. Not necessarily today or tomorrow, but over the coming quarters—specifically during the second and third quarters of this year.

Their reasoning is straightforward. While the Federal Reserve remains on hold, other central banks—particularly the European Central Bank (ECB)—continue to tighten monetary policy. The interest-rate differential is narrowing, and when rate differentials shrink, the dollar loses one of its most important advantages.

Why the Fed’s Pause Could Hurt the Dollar

At first glance, the opposite should be true. Higher U.S. interest rates are generally positive for the dollar. Investors from around the world buy U.S. bonds because they offer attractive yields with relatively low risk. Demand for dollars rises, and the currency strengthens.

That is a basic principle taught in introductory economics courses.

Morgan Stanley, however, views the situation differently. Yes, U.S. rates remain high—but they are no longer rising. The Fed has paused. More importantly, markets have already priced in virtually all potential rate increases. From here, the next major move is more likely to be downward.

Europe, meanwhile, is moving in the opposite direction. The ECB, which lagged behind for much of the tightening cycle, is now catching up. Morgan Stanley expects the ECB to raise rates twice this year.

What happens when one central bank stands still while another continues hiking? The gap narrows. And as the gap narrows, a previously less attractive currency—such as the euro—becomes increasingly appealing. Investors begin reallocating capital from dollars into euros.

As Adams puts it, the balance of risks points toward a weaker dollar. This does not mean the dollar will collapse overnight. It simply means that the forces that previously drove it higher are fading, while the factors pushing it lower are gaining momentum.

The Euro: Biggest Winner or Potential Trap?

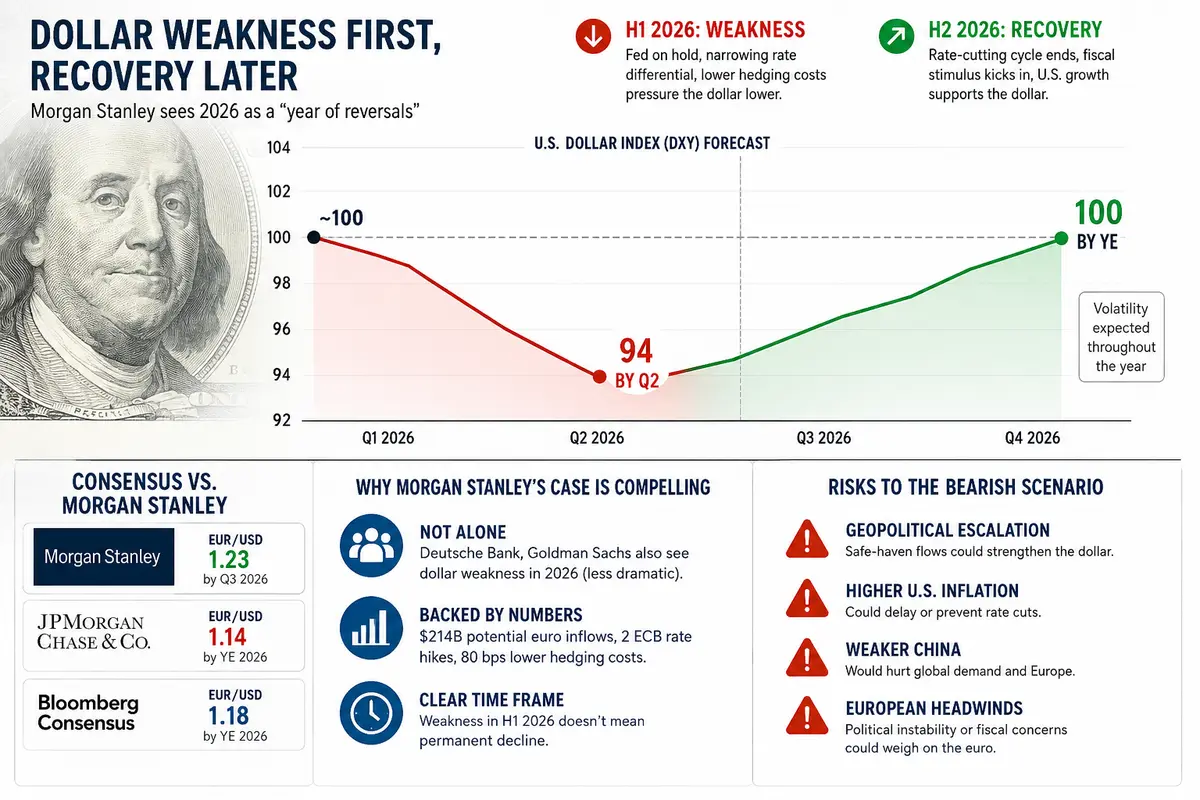

Morgan Stanley’s forecast for the euro is remarkably specific. The bank expects the common currency to rise to $1.23 per euro by the third quarter of this year.

From current levels around $1.15–$1.16, that represents nearly a 7% gain—an enormous move in foreign exchange markets.

This optimism is not based solely on interest rates. Morgan Stanley highlights another factor that receives far less media attention but could prove critical: currency hedging costs.

In simple terms, European investors hold roughly $10 trillion in U.S. assets, including bonds, stocks, and real estate. To protect themselves from fluctuations in the dollar, they hedge their currency exposure. The cost of that hedge depends largely on the interest-rate differential between the U.S. and Europe.

When U.S. rates are significantly higher than European rates, hedging becomes expensive. Under those conditions, it is less attractive for Europeans to convert dollar holdings back into euros.

But that situation is changing. European rates are rising while U.S. rates have stalled. As a result, hedging costs are falling.

Morgan Stanley estimates that an 80-basis-point decline in hedging costs could trigger approximately $214 billion of inflows into the euro. European investors may begin converting more of their dollar assets back into euros because doing so will no longer carry such a high cost.

This is a powerful technical support factor for the euro—one that is largely independent of economic growth or geopolitical developments.

And $214 billion is not a trivial amount. It is comparable to the annual GDP of a smaller European economy.

Who Else Benefits from a Weaker Dollar?

Morgan Stanley’s bearish dollar view extends beyond the euro.

The bank also expects the Canadian dollar to strengthen. With the current exchange rate near 1.39 Canadian dollars per U.S. dollar, Morgan Stanley sees potential for a move toward 1.35.

According to Adams, the Canadian dollar has already priced in substantial pessimism. Market expectations for Canada are low, making it easier for the country to surprise on the upside.

Such positive surprises could come from stronger-than-expected economic growth, a more hawkish stance from the Bank of Canada, or a recovery in oil prices—an important driver of the Canadian economy.

Morgan Stanley also expects dollar weakness to be particularly pronounced during the first half of 2026. Their forecast for the U.S. Dollar Index (DXY) calls for a decline to 94 in the second quarter, the lowest level since 2021 and roughly 6% below current levels.

But There’s a Catch: The Dollar Could Rebound Later

The story would be incomplete without noting that Morgan Stanley is not bearish on the dollar for the entire year.

Their outlook is highly time-specific.

They expect weakness during the first half of 2026, followed by a recovery in the second half.

Why?

By year-end, the Federal Reserve is likely to have completed its rate-cutting cycle. Once that process ends—and assuming the U.S. economy continues to grow—the dollar could regain support.

In addition, fiscal stimulus measures are expected to gain traction later in the year. Congress may approve new spending packages that provide additional support to economic activity and, by extension, to the dollar.

Morgan Stanley therefore sees 2026 as a “year of reversals.” The Dollar Index could fall to 94 in the second quarter and then recover toward 100 by year-end—essentially finishing the year near where it started.

The journey, however, could be highly volatile.

Consensus vs. Morgan Stanley: Who Is Right?

An important caveat is that Morgan Stanley’s forecast is not the market consensus.

Many major financial institutions have a different outlook. JPMorgan, for example, expects the euro to decline toward 1.14 by year-end—a forecast that points in the opposite direction. Bloomberg’s consensus estimate is closer to 1.18.

Who is right?

Only time will tell.

Still, Morgan Stanley presents several compelling arguments.

First, they are not alone. Other major institutions, including Deutsche Bank and Goldman Sachs, also expect some degree of dollar weakness in 2026, albeit less dramatic.

Second, their thesis is grounded in quantifiable factors: $214 billion in potential euro inflows, two expected ECB rate hikes, and an 80-basis-point decline in hedging costs.

Third, they clearly distinguish between short-term and long-term dynamics. A weaker dollar in the second quarter does not imply a permanent decline.

Risks to the Bearish Scenario

Like any forecast, Morgan Stanley’s outlook faces significant risks.

1. Geopolitical Escalation

The biggest risk is geopolitics.

If tensions in the Middle East intensify—or if Iran and Israel move from limited exchanges to a broader conflict—the dollar would likely strengthen as investors seek safety. The euro, viewed as riskier, would probably weaken.

2. Higher U.S. Inflation

Another risk is inflation.

If upcoming consumer-price data come in above expectations, the Federal Reserve may be unable to consider rate cuts. Markets could even begin pricing in further tightening, directly contradicting Morgan Stanley’s assumptions.

3. A Weakening Chinese Economy

If China’s economy deteriorates rather than recovers, global demand would suffer.

Lower commodity prices and weaker trade activity would hurt Europe, whose economy remains closely linked to China. In such a scenario, the euro could fall while the dollar gains.

4. Europe’s Own Problems

Europe also faces internal challenges.

Adams himself notes that the ECB has only limited tolerance for excessive euro appreciation. A stronger euro can hurt European exporters.

Political uncertainty—particularly around French elections and fiscal concerns—could also undermine confidence. If investors become concerned about instability in Europe, capital could flow back into the dollar.

What Does This Mean for Ordinary People?

Amid all the discussion of rates, hedging costs, and central-bank policy, it is easy to forget why these issues matter.

They matter because they affect everyday people.

If Morgan Stanley’s forecast proves correct and the dollar weakens during the second and third quarters, several consequences follow:

-

For American tourists: Bad news. Your dollars will buy fewer euros, pounds, and yen, making overseas travel more expensive.

-

For U.S. importers: Also bad news. Goods from Europe, Japan, and China become more expensive in dollar terms, potentially adding inflationary pressure.

-

For U.S. exporters: Good news. American products become more competitive abroad, potentially boosting sales and profits.

-

For investors holding European assets: Positive news. Currency appreciation could enhance returns when converted back into dollars.

-

For investors holding dollar assets only: Largely neutral. If you do not intend to convert into other currencies, exchange-rate fluctuations may have limited impact.

Final Thoughts: A Forecast Worth Watching

Morgan Stanley has made a bold call.

In a world where many analysts expect the dollar to remain strong—or at least stable—the bank is forecasting a decline of roughly 5–6% during the first half of the year.

They have attached specific numbers to that view:

-

Euro at 1.23

-

Dollar Index (DXY) at 94

-

Roughly $214 billion of potential euro inflows

-

Two ECB rate hikes

-

Significantly lower hedging costs

This is not a speculative guess. It is a framework built on measurable factors and a coherent macroeconomic narrative.

That does not mean it will be correct.

Markets are unpredictable. Geopolitical shocks can emerge without warning. Inflation may surprise. China may disappoint. Europe may encounter fresh political challenges.

Morgan Stanley’s outlook should therefore be viewed not as certainty, but as one plausible and well-reasoned scenario among many.

What seems increasingly likely, however, is that 2026 will be a volatile year for currency markets—a year of sharp turns and shifting narratives.

And at the center of that story is David Adams and his team at Morgan Stanley, watching a crowd that continues to chant “the dollar is king” while calmly repeating a very different message:

“We are bearish.”

Only time will determine who gets the last word.

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.