HSBC Expects a Weaker Dollar as Markets Change Their Reaction to Data

When Good News Stops Being Good News for a Currency

There is an old, almost cliché truth in finance: a strong U.S. economy means a strong dollar. It seems logical enough. GDP rises, and investors bring money into America. Strong employment data strengthens the dollar. Geopolitical tensions drive investors into the dollar as a safe haven. This relationship worked for decades. It was an axiom that required no proof.

But, as it turns out, even axioms can become outdated.

HSBC Asset Management, which oversees $863 billion in assets, has made a rather provocative claim. According to the firm’s strategists, the dollar is headed for weakness. Not merely a temporary correction or a short-term pullback, but a structural downward trend. Their key argument sounds almost paradoxical: the dollar no longer responds to good news the way it once did.

Joe Little, Global Chief Strategist at HSBC Asset Management, articulated the idea with remarkable precision. Historically, the combination of strong domestic growth and geopolitical tension created a powerful and sustained uptrend for the U.S. currency. Investors from around the world flocked to the dollar because America was both a haven of stability and an engine of growth. Today, that dynamic appears to be fading. The dollar still rises at times, but reluctantly, sluggishly, and with frequent reversals. Little sees this as a symptom of a deeper problem.

Something has changed. The question is: what exactly?

The Dollar That Doesn’t Want to Rise

Let’s look at the numbers. The Bloomberg Dollar Spot Index gained just 0.6% over the past month. In currency markets, six-tenths of a percent is barely a move. It’s a tremor rather than a trend.

And this happened despite the U.S. economy continuing to surprise on the upside. Job openings exceeded expectations. Consumer spending remains resilient. Industrial production is expanding. Inflation has slowed, but it has not disappeared.

In the past, any one of these factors might have boosted the dollar by half a percent, while all of them combined could have driven a multi-percent rally. Yet the dollar remains largely stuck in place. It resembles an athlete who builds momentum but cannot quite leave the ground.

Joe Little views this as a paradigm shift. Markets, he argues, no longer react to U.S. economic data as they once did. Positive news from America no longer automatically translates into dollar buying. Investors have begun asking uncomfortable questions:

-

How sustainable is this growth?

-

What happens when fiscal support fades?

-

Is the economy overheating?

-

Is the dollar already too expensive?

These are not rhetorical questions. They are grounded in reality.

The U.S. economy has indeed displayed remarkable resilience. But that resilience has come at a cost: a national debt exceeding $34 trillion, high interest rates that weigh on businesses and households, and trade conflicts and sanctions that gradually erode confidence in the dollar as the world’s universal settlement currency.

In short, good news is still good news—but it is no longer an unconditional positive for the dollar. The market senses that.

Energy Shocks and Geopolitical Fatigue

In his comments, Little highlighted two factors currently influencing the dollar: energy shocks and geopolitical tensions.

Traditionally, both would have supported the dollar. Today, however, they may be working against it.

Why? Because both have lasted too long.

Markets are tired of being afraid. They are tired of waking up every day to headlines about missile strikes, new tariffs, or political disputes. Fear eventually becomes normalized. Human beings cannot remain in a constant state of anxiety forever, and financial markets are no different.

As a result, when another confrontation occurs between the United States and Iran, investors no longer rush headlong into the dollar. Instead, they shrug and say, “Here we go again. Let’s see what happens tomorrow.” Then they continue holding assets that generate returns—stocks, emerging-market bonds, and gold.

The energy story is even more interesting.

Historically, expensive oil meant higher inflation. Higher inflation led to higher interest rates. Higher interest rates strengthened the dollar.

That chain of logic worked for decades.

Today, however, high U.S. rates create problems for the rest of the world, particularly for countries that owe debt denominated in dollars. And there are many such countries.

When the dollar strengthens because of an oil shock, emerging economies face greater debt burdens. That increases risks for the American banks that have lent to them. It also hurts U.S. exporters, who struggle to compete against cheaper products from countries with weaker currencies.

Modern markets are a complex system of feedback loops. Good news for the U.S. economy can become bad news for the dollar because it delays Federal Reserve rate cuts. And high interest rates, somewhat paradoxically, are no longer an unambiguous positive for the currency.

High rates mean expensive borrowing costs for the U.S. government. Expensive debt creates concerns about fiscal sustainability. While a U.S. default remains highly unlikely, the market cannot ignore the growing burden.

Dollar Overvaluation: A Quiet Threat

HSBC Asset Management’s third argument concerns valuation.

The firm’s strategists believe the dollar is significantly overvalued. This is not a new claim—analysts have been discussing dollar overvaluation for years. But overvaluation matters because it creates vulnerability.

When an asset is expensive, it does not take much to trigger a correction.

That catalyst could come from anywhere.

For example, if the Federal Reserve signals that its rate-hiking cycle is definitively over rather than merely paused, the dollar could begin to decline. If geopolitical tensions ease, the dollar could weaken. If China and Europe show signs of sustained growth, investors may shift capital away from the dollar in pursuit of higher returns elsewhere.

Little believes the broader weakening trend that began to emerge last year remains intact. Strong U.S. data may occasionally push the dollar higher, but in his view, the overall direction remains downward.

The main risk to this outlook would be a renewed acceleration in U.S. inflation. If oil prices were to surge to $120 per barrel and consumer prices followed, the Fed might be forced not only to maintain high rates but to raise them further.

In that scenario, the dollar could enjoy a second wind.

Even then, however, Little expects any rally to be limited. Markets are increasingly looking beyond the dollar. The world is searching for alternatives. Even the strongest currency has its limits.

What It Means for Emerging Markets

For emerging markets, a weaker dollar is like a breath of fresh air.

The dollar is the world’s reserve currency. Debt, contracts, and savings are often denominated in it. When the dollar weakens, it becomes easier for poorer countries to service their debts.

A weaker dollar also encourages capital to flow out of the United States in search of higher returns. Emerging markets are natural destinations for that capital.

HSBC Asset Management expects emerging-market currencies to benefit from dollar weakness. Local stock and bond markets could benefit as well.

An important concept here is undervaluation.

The bank’s strategists argue that many emerging-market currencies remain undervalued relative to the dollar. Based on fundamentals such as economic growth, trade balances, inflation, and interest rates, these currencies appear cheaper than they should be.

As the dollar weakens, that undervaluation may begin to correct itself.

The first beneficiaries are often the countries that suffered most during previous periods of dollar strength:

-

Latin America: Brazil, Mexico, Argentina

-

Southeast Asia: Indonesia, the Philippines, Thailand

-

Central and Eastern Europe: Poland, Hungary, the Czech Republic

These markets share an attractive combination of relatively high real interest rates and comparatively low currency valuations.

There is, however, another side to the story.

Countries that depend heavily on exports to the United States may face challenges. As the dollar weakens, Americans become less wealthy in terms of global purchasing power. They may buy fewer imported goods, from Chinese smartphones to Vietnamese clothing and Mexican auto parts.

HSBC appears to believe that the positive effects of capital inflows will outweigh any export-related headwinds.

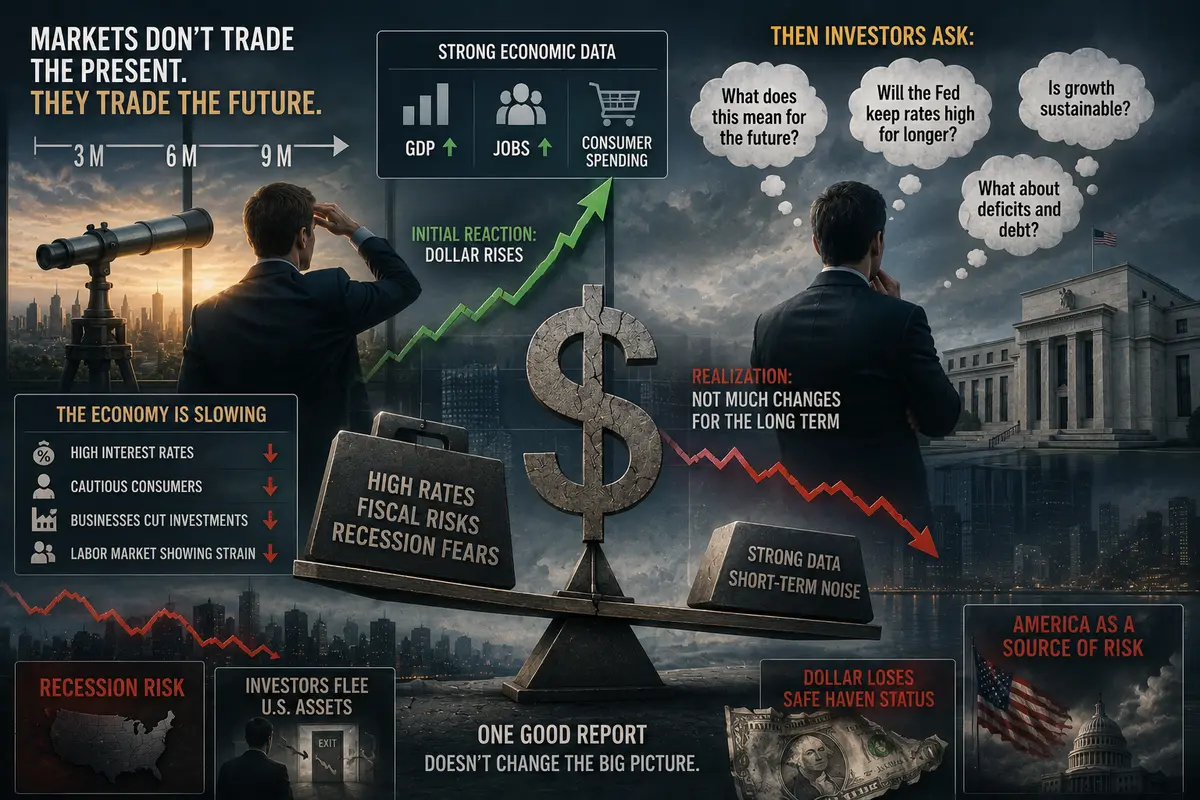

Why Markets Have Changed Their Response to Data

Let’s return to Little’s central argument.

Why do strong U.S. economic reports no longer automatically push the dollar higher?

The answer lies in expectations.

Markets do not trade the present; they trade the future—three, six, or nine months ahead.

The prevailing consensus today is that the U.S. economy is slowing. Not collapsing, but gradually losing momentum. High interest rates are beginning to have their intended effect. Consumers who borrowed heavily during the era of cheap money are becoming more cautious. Businesses are scaling back investments. Even the labor market is showing the first signs of strain.

As a result, when strong economic data is released, the dollar may initially rise. But then investors step back and ask: what does this mean for the long-term outlook?

Often, their answer is: not much.

A single positive data point does not overturn the broader slowdown narrative.

In fact, data that is too strong can sometimes hurt the dollar. Strong growth may force the Fed to keep rates elevated for longer. Elevated rates increase concerns about America’s fiscal position and raise fears that tighter monetary policy could eventually trigger a recession.

And a U.S. recession would be deeply negative for the dollar because investors would flee American assets.

The irony is striking: the dollar has become less of a safe haven precisely because America itself is increasingly perceived as a source of risk.

What If HSBC Is Right?

Suppose, for a moment, that Joe Little and his team are correct.

The dollar enters a long-term decline. Energy shocks fade. Geopolitical tensions ease. Markets return to something resembling normality.

What would that mean?

For Americans traveling to Europe, it would mean a stronger euro and more expensive vacations. Imported goods—from wine to automobiles—would cost more. Inflation could receive a fresh boost from a weaker currency.

For European exporters, it would be welcome news. A weaker dollar makes their products more competitive in the U.S. market. German cars, French wine, and Italian shoes would become relatively more attractive.

For investors in emerging markets, it could create opportunities. As local currencies appreciate against the dollar, wealth measured in dollar terms increases, encouraging consumption and investment.

For global equities, a weaker dollar is generally positive. Cheaper money tends to support asset prices, particularly for multinational companies that generate substantial revenues outside the United States.

There would also be losers.

Commodity-exporting nations whose products are priced in dollars may see revenues decline in local-currency terms. Countries such as Russia, Brazil, and South Africa could face challenges, although many other factors would influence the outcome.

Wait or Act?

HSBC Asset Management’s forecast is not an instruction to buy or sell anything. It is simply a worldview expressed by highly experienced professionals responsible for managing enormous sums of money.

They could be wrong.

Markets are unpredictable. Geopolitical events can overturn even the most sophisticated models.

Yet one thing seems increasingly clear: the world is changing.

The dollar is no longer the only magnet for global capital. The euro, despite its struggles, remains relevant. The Chinese yuan is gradually expanding its role in international trade and finance. Gold is returning to favor as a neutral safe-haven asset not tied to any government.

In this new environment, the dollar will likely remain the world’s strongest and most important currency.

But it may no longer be the only game in town.

For now, the dollar sits in place—responding to economic data with unusual hesitation, waiting for something.

Perhaps a signal from the Federal Reserve.

Perhaps peace in the Middle East.

Perhaps simply the passage of time.

Time, as we know, can heal.

But in the world of currencies and confidence, it can also destroy.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.