Chalco Plunges 9%: Goldman Sachs Says “Sell,” and Investors Run for the Exits

Monday: A Day of Red Numbers and Green Analysts

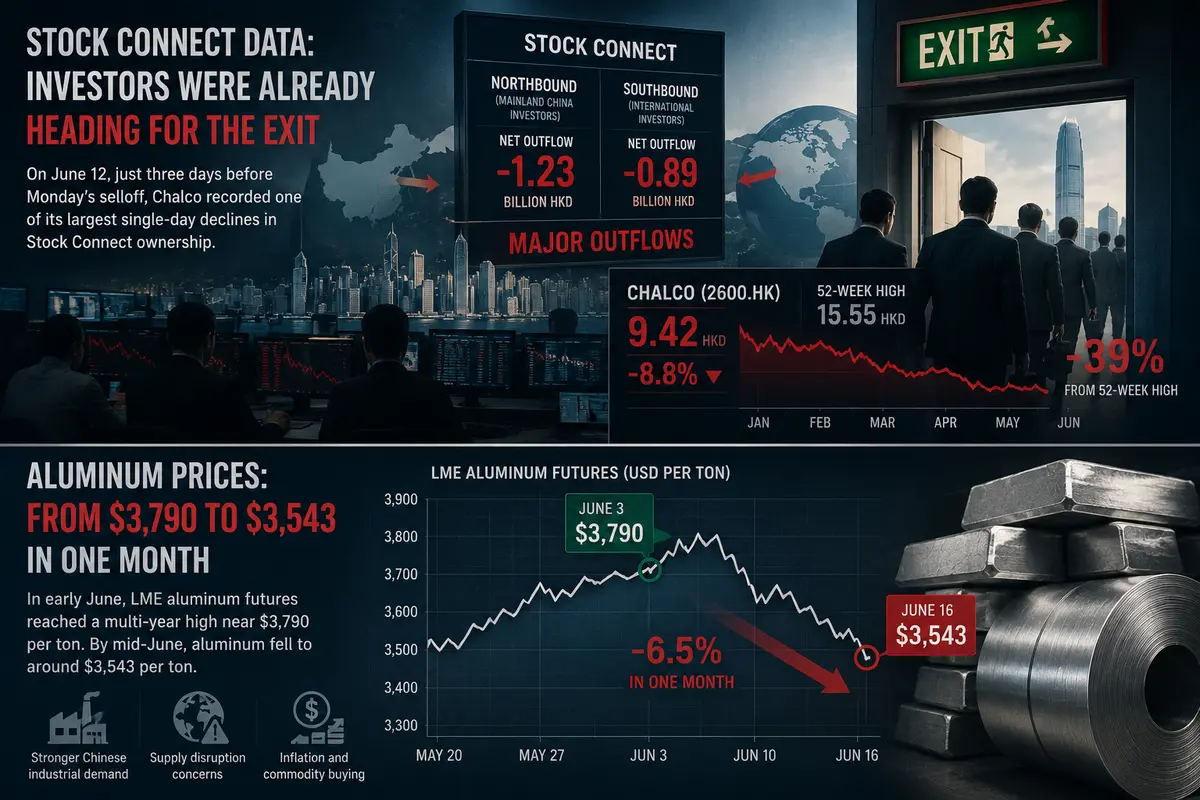

Monday was not kind to everyone on the Hong Kong Stock Exchange. Shares of Aluminum Corporation of China (Chalco) — China’s largest aluminum producer, a state-owned giant that carries much of the country’s non-ferrous metals industry on its shoulders — fell 8.8%. The stock dropped to HK$9.42 per share. At one point, losses reached 10%, before recovering slightly to around 8.8% by midday.

What happened? Why did a company that just a month ago seemed to embody China’s industrial strength suddenly become the target of a major selloff?

The answer: Goldman Sachs.

The U.S. investment bank, one of the most influential financial institutions in the world, downgraded Chalco from “Neutral” to “Sell” and cut its price target from HK$12.50 to HK$7.50. In other words, Goldman believes the stock could still fall another 20% from current levels.

A downgrade from Goldman is more than just an opinion. It is a signal followed by hundreds of institutional funds. When Goldman says “sell,” many investors sell first and ask questions later. That is exactly what happened on Monday.

But Goldman’s call was only part of the story. Chalco also faces several fundamental challenges: rising aluminum supply in China and globally, declining metal prices, a stronger U.S. dollar weighing on commodities, and evidence that investors have been pulling money out of the stock through the Stock Connect program.

Let’s break it down.

Goldman Sachs: What They Said and Why

Goldman Sachs is not just another brokerage. Alongside Morgan Stanley and JPMorgan, it is one of America’s largest investment banks. Its analysts rarely make dramatic rating changes. Typically, recommendations move gradually from “Buy” to “Hold” to “Sell.” Cutting a price target by 40% in a single move is unusual.

So what prompted Goldman to take such an aggressive stance?

According to reports summarizing the bank’s research note, Goldman highlighted three key concerns.

1. Rising Aluminum Supply in China

China produces more than half of the world’s aluminum. Despite government promises to limit production for environmental reasons, smelters operated by Chalco and its competitors have continued running at full capacity. Inventories are growing, and when supply rises faster than demand, prices fall.

2. Increasing Global Production

China is not alone. Producers in Russia (Rusal), India (Hindalco), and the Gulf region (Emirates Global Aluminium) are all expanding output.

Analysts expect the global aluminum market to move into a surplus of roughly 1–2 million metric tons in 2026. Excess supply generally puts downward pressure on prices.

3. Falling Aluminum Prices

Aluminum futures on the London Metal Exchange (LME) retreated from around $3,790 per ton in early June to approximately $3,543 per ton by mid-June — a decline of more than 6% in a month.

For a company whose profitability is directly tied to aluminum prices, such a move matters enormously.

Goldman believes this is not a temporary correction but the beginning of a longer-term trend in which supply growth outpaces demand growth over the next 12–18 months.

Chalco’s Fundamental Problems Go Beyond Metal Prices

Even without Goldman’s downgrade, Chalco faces structural challenges.

Like much of China’s industrial sector, the company struggles with overcapacity. Beijing has spent years trying to reduce excess production, but local governments often continue supporting factories because they provide jobs and tax revenue.

Chalco is not a private company. It is state-controlled. While its shares trade in Hong Kong, Shanghai, and New York (through ADRs), the government remains the controlling shareholder.

That creates a dilemma. Chalco does not always operate according to purely market-based principles. Sometimes production continues even when profitability is weak because shutting down facilities could trigger social and economic disruptions.

This creates a vicious cycle:

-

Chalco keeps producing aluminum.

-

Supply keeps increasing.

-

Prices remain under pressure.

-

Profitability deteriorates further.

Debt Remains a Concern

Chalco also carries substantial debt.

The company’s debt-to-equity ratio exceeds 150%. During periods of strong aluminum prices, cash flow is sufficient to service that debt. But when prices decline, leverage becomes much more problematic.

In 2025, Chalco reported net income of approximately 10.5 billion yuan (about $1.5 billion). However, analysts expect profits to decline by 30–40% in 2026 as aluminum prices soften.

Should aluminum fall toward $3,000 per ton, profitability could come under severe pressure.

Stock Connect Data: Investors Were Already Heading for the Exit

Another warning sign came from the Hong Kong Stock Connect program, which allows mainland Chinese investors to buy Hong Kong-listed shares and international investors to access mainland Chinese equities.

On June 12, just three days before Monday’s selloff, Chalco recorded one of its largest single-day declines in Stock Connect ownership.

In plain English: both mainland Chinese and international investors were already pulling money out of the stock.

Why?

Because many investors had already reached the same conclusion Goldman later formalized: aluminum market fundamentals are deteriorating.

Whether they had better information or simply followed market signals, the result was clear — major investors were voting with their feet before the downgrade became official.

Today, the stock trades roughly 39% below its 52-week high of HK$15.55.

A 39% decline in just a few months is not a correction. It is a collapse.

Aluminum Prices: From $3,790 to $3,543 in One Month

To understand the scale of the challenge, consider the aluminum market itself.

In early June, LME aluminum futures reached a multi-year high near $3,790 per ton.

The rally was driven by:

-

Expectations of stronger Chinese industrial demand.

-

Concerns about supply disruptions linked to Middle East tensions.

-

Broader inflation-related commodity buying.

By mid-June, however, the picture had changed dramatically.

U.S. inflation data came in less alarming than expected. Geopolitical fears eased. China’s economy failed to deliver the acceleration many investors had anticipated.

As a result, aluminum fell to around $3,543 per ton.

For a commodity that often moves only 1–2% in a month, a decline of more than 6% is significant.

Why the Dollar Matters

Aluminum, like most commodities, is priced in U.S. dollars.

When the dollar strengthens, aluminum becomes more expensive for buyers using other currencies. Demand tends to weaken, putting downward pressure on prices.

Recent strength in the dollar has been supported by solid U.S. labor-market data and expectations that the Federal Reserve may keep interest rates elevated.

That has added another headwind for both aluminum prices and Chalco shares.

What Happens Next?

Analysts are divided.

Goldman Sachs remains firmly bearish, with a HK$7.50 target and a “Sell” rating.

Other banks, including Morgan Stanley and Citi, maintain more neutral views. They acknowledge the challenges but argue that much of the bad news is already reflected in the share price. Their targets generally fall in the HK$10–11 range.

Chinese brokerage firms remain more optimistic. Many continue recommending the stock as a “Buy,” believing Beijing could step in through subsidies, import restrictions, or demand-stimulus measures.

However, there is a catch.

China is currently focused on addressing its property-sector debt problems and slowing economic growth. Resources are limited, and Chalco is far from the only industry facing difficulties.

The Long-Term Case vs. The Short-Term Reality

Investors need to answer a simple question:

Do they believe in long-term aluminum demand?

Aluminum remains a critical material for:

-

Automobiles and lightweight vehicles

-

Aerospace manufacturing

-

Construction

-

Packaging

-

Renewable energy infrastructure

-

Electric vehicles

Over the long run, demand is likely to grow alongside the global economy and the energy transition.

But over the next 6–12 months, supply appears to be growing faster than demand.

That means:

-

Aluminum prices may remain under pressure.

-

Chalco’s earnings could decline.

-

The stock may continue struggling.

Goldman is effectively betting that this imbalance lasts longer than the market currently expects.

The Entire Aluminum Sector Is Under Pressure

Chalco was not the only aluminum company in the red on Monday.

-

Rusal shares declined roughly 4%.

-

Hindalco fell around 3%.

-

Alcoa futures pointed lower by about 2%.

The weakness was sector-wide.

Traders are increasingly pricing in a significant aluminum surplus during the second half of the year.

What could reverse the trend?

A major demand surprise.

For example:

-

A large-scale Chinese infrastructure stimulus program.

-

Accelerated renewable-energy spending in Europe and the United States.

-

Faster-than-expected electric vehicle adoption.

For now, however, none of those catalysts appear imminent.

What Should Investors Do?

If you own Chalco shares, the decision is not easy.

Do you sell now after a nearly 40% decline from the highs? Or do you hold and wait for aluminum prices to recover?

Goldman says sell.

But Goldman is not infallible.

The bank has made high-profile mistakes before. Markets are cyclical, and aluminum is no exception. Every downturn is eventually followed by recovery.

The real question is whether investors are willing to wait — and whether they can tolerate the volatility along the way.

Chalco is not a speculative startup that could disappear overnight. It is a state-backed industrial giant. Beijing is unlikely to let it fail.

That said, investors should not expect quick gains.

On Monday, the stock fell nearly 9%. Goldman Sachs pushed the red button. Investors rushed for the exits.

The only question now is: who follows them, and who stays behind to buy at the bottom?

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.