Japan Just Did It — 1% Rates for the First Time Since 1995, and the Yen Still Didn’t Move

The BoJ delivered the hike every trader expected. Then it softened the forward guidance — and gave the market an excuse to keep selling yen. This is what happens when you telegraph a move for too long.

Capital Street FX Research Desk · 16 June 2026

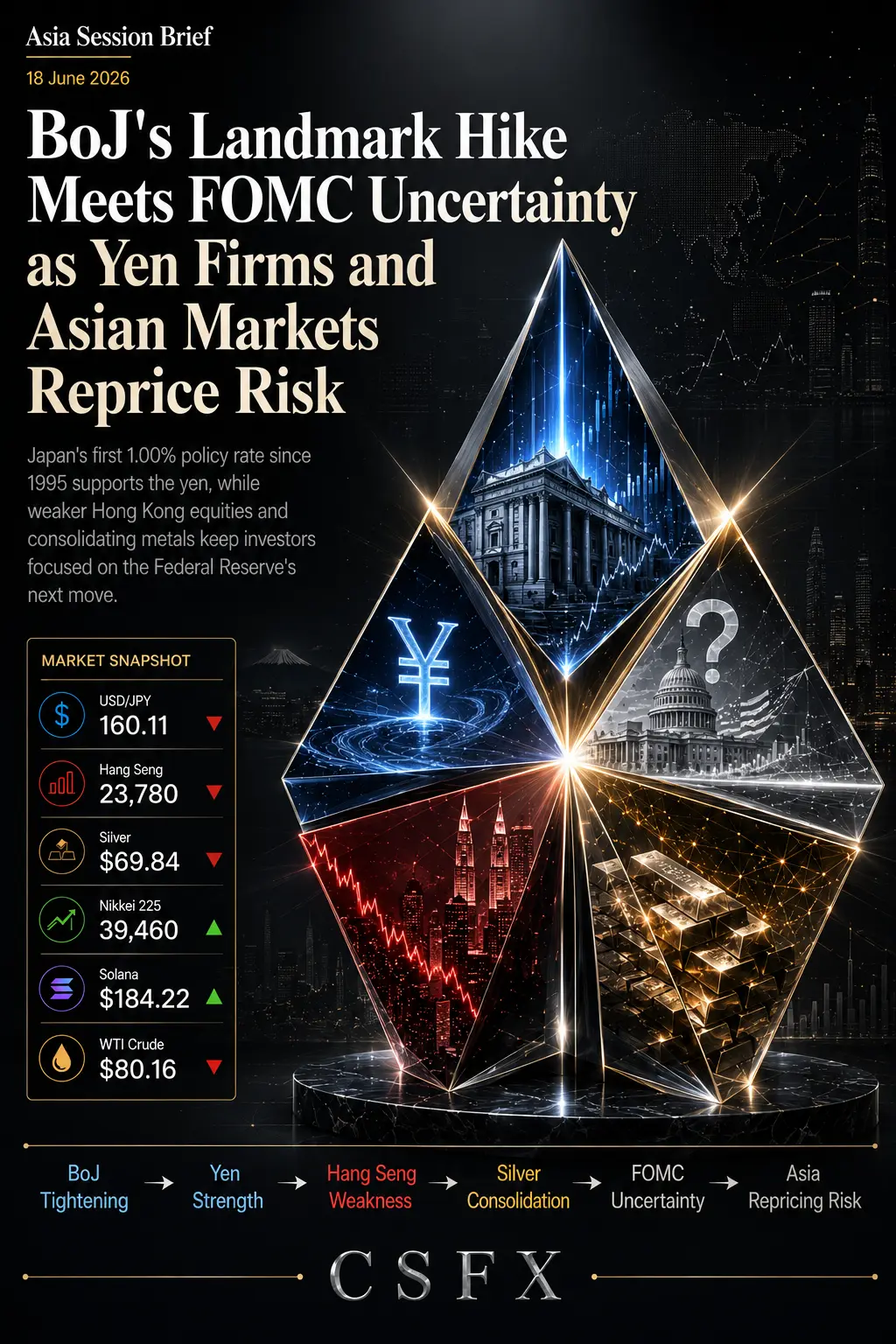

The Bank of Japan hiked its policy rate 25 basis points to 1.00% today — the first time Japan has held rates at this level since 1995. That is not a trivial number. Thirty-one years. Two lost decades. Four deflation cycles. A generation of traders who have never seen Japan do anything but hold or cut. And yet, in the immediate aftermath of the decision, USD/JPY barely moved. It ticked up, not down. Which tells you something important about what actually drives currency markets: not the decision everyone knows is coming, but the words that come after it.

Governor Ueda delivered the hike — then attached a notably dovish element. The BoJ will pause its Japanese government bond tapering schedule from April 2027. That single sentence told the market that this is a careful, deliberate central bank that is not in a hurry to do the next thing. And in a world where traders had already priced in the 1% hike weeks ago, ‘not in a hurry’ is interpreted as: stay long dollars, stay short yen. The yen remains weak. USD/JPY firmed above 159.75 in the aftermath.

Japan hiked for the first time since 1995. And the yen went down. That’s what happens when a move is telegraphed for six weeks.

What the BoJ Hike Actually Means — Beyond the Headline

Here is the part that matters more than the rate decision itself. The BoJ hiked into a specific economic context: Japan’s wholesale inflation is running at 6.3% year-on-year, driven almost entirely by the energy shock from Middle East conflict. But the Bank simultaneously cut its growth outlook slightly, creating the mild stagflationary dynamic that complicates every subsequent decision. If energy prices start falling — and the Iran peace deal, if signed, would accelerate that — the BoJ’s inflation justification weakens even as its rate normalisation cycle is just beginning.

The carry trade is the mechanism that connects all of this to global markets. Investors borrow cheaply in yen, convert to higher-yielding assets — dollars, crypto, emerging market debt — and collect the spread. When Japan raises rates, that spread compresses. The borrow becomes more expensive. Over time, carry trades unwind. The historical pattern is clear: BoJ tightening cycles correlate with elevated volatility in Bitcoin, emerging market FX, and risk assets broadly. That unwind does not happen in a single session. It happens over weeks, as positions are reduced one margin call at a time. Today’s session is the starting gun, not the finish line.

The Hang Seng: When Good News Gets Complicated

The Hang Seng is underperforming this morning, and the reason is instructive. China’s retail sales data for May came in weak — below expectations — and in an index that had been running on AI optimism and Iran ceasefire relief, a domestic demand miss is a meaningful reality check. The Hang Seng’s recent surge had been built on two supports: the risk-on wave from ceasefire hopes and the China tech recovery narrative. Take away one of those supports and the index finds itself testing levels it was rallying through last week.

This does not invalidate the medium-term case for Hang Seng recovery. China’s AI infrastructure spending is real. The ceasefire-driven oil relief is real. But today’s session is a reminder that a market that has moved fast needs confirmation from the fundamentals to keep moving. Weak retail sales is not confirmation. The 25,000 level is the structural support to watch — a hold there on a day like this would actually be a constructive signal.

Silver: Where the Peace Deal and Rate Hikes Collide

Silver is having one of the more interesting sessions in recent weeks — caught between forces that are pulling in genuinely opposite directions. On the bearish side: the Iran peace deal optimism is deflating the geopolitical safe-haven premium that had inflated silver to extraordinary levels through the conflict. On the bullish side: a BoJ rate hike, if it signals the beginning of a genuine yen strengthening cycle, is eventually dollar-bearish, and a weaker dollar is mechanically supportive for dollar-priced metals.

Right now, the bearish force is winning. Silver has been retreating from its war-premium highs toward the zone around $65 to $67 per ounce where real structural support from solar and EV industrial demand sits. That industrial floor is genuine — roughly half of silver demand is now industrial, and the energy transition is not a story that reverses because of a ceasefire. But the safe-haven component that was overlaid on top of it is deflating, and that deflation has further to run until a signed ceasefire removes all residual uncertainty.

Silver has two stories: a war-premium deflating from the top, and an industrial demand floor holding from the bottom. Right now the top is winning.

Crypto: The Carry Trade Connection

Bitcoin and Ethereum are both soft in today’s session, and the explanation runs through Tokyo. The BoJ hike compresses the yen carry trade over time. Some of the capital that was deployed into crypto on the back of cheap yen borrowing will eventually come home. Not today, not all at once, but the direction of travel for leveraged crypto longs that were funded by yen carry positions is lower — or at minimum, more volatile — in the weeks following a BoJ hike.

The more interesting crypto story today is the divergence between the assets. Bitcoin, which has the deepest institutional base and the clearest ETF-flow data to track, is more likely to find support on any pullback from genuine institutional buyers who use dips to accumulate. The altcoin complex — including XRP, which has its own CLARITY Act regulatory narrative — is more vulnerable to carry-unwind pressure because its holder base is more retail and more leveraged. Watch Bitcoin’s $63,000 to $64,000 zone as the tell for the session’s direction. If that holds with volume, the carry-unwind fear is overblown for today. If it breaks, the next support is not close.

The Week’s Central Question — And Today’s Answer

Every trade this week comes back to one question: is the BoJ’s forward guidance hawkish enough to drive genuine yen strength, or dovish enough to let the carry trade live for another month? Today’s answer, from the price action, is the latter. The BoJ hiked — as expected — and then softened the message enough that traders kept their carry positions. USD/JPY above 159 after a rate hike is not what a hawkish BoJ looks like in practice. It is what happens when a central bank is careful, communicative, and very deliberate about not spooking markets.

That does not mean yen strength is off the table for this week. It means the catalyst for genuine yen appreciation is the forward guidance that comes over the next month, not today’s hike. Watch the next BoJ communication. Watch whether inflation data in Japan starts to show broadening beyond energy. And watch whether the Iran ceasefire, if signed, removes the inflationary pressure that was giving the BoJ its urgency in the first place — because a world where Japanese inflation falls back toward 2% while the BoJ is trying to normalize at 1% is a world where the hiking cycle ends quickly, and the yen carry trade lives on.

─

Live trade levels, technical analysis, and session-by-session commentary for USD/JPY, silver, Hang Seng, and crypto published daily at Capital Street FX.

Read Full Report: capitalstreetfx.com/market-analysis/daily-market-analysis/

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.