Calm Before the Storm: Asian Currencies Freeze in the Shadow of War and Looming Rate Hikes

At first glance, Asian currency markets looked almost sleepy on Wednesday. Most pairs drifted within narrow ranges, traders seemed to hit pause, and price action resembled the heartbeat monitor of a patient under heavy sedation. But this silence is deceptive. Beneath the surface calm of sideways trading lies enormous tension ready to erupt at any moment. When three forces converge at once — a war disrupting one-fifth of global oil supplies, renewed fears of Federal Reserve rate hikes, and deepening geopolitical fractures among major powers — markets do not calm down; they become paralyzed, trying to calculate where the first blow will come from.

The Heavyweight Dollar and the Ghost of Tightening

The dollar index hovering near six-week highs is the perfect barometer of global anxiety. Whenever the world starts shaking, money inevitably rushes into the dollar, and the current situation is no exception. But what makes this moment unique is that the dollar is rising not only as a safe haven, but also as a currency that could become even more profitable. Markets have once again started talking about something they tried to forget over recent months — another Fed rate hike.

This narrative did not emerge out of nowhere. Remarks by Philadelphia Federal Reserve Bank President Anna Paulson, made almost casually on Tuesday evening, became the detonator. When a senior Fed official says it is reasonable for markets to speculate about possible rate increases, it is not just rhetoric — it is a signal. Central bankers rarely speak carelessly. Behind such comments lies growing concern within the Fed over energy-driven inflation, which has begun accelerating again after the conflict with Iran disrupted supplies through the Strait of Hormuz.

Inflation caused by a supply shock is the most unpleasant type of inflation for central banks. It cannot be fought with traditional demand-cooling tools because the problem is not that consumers are buying too much, but that the product is physically disappearing from the market. Oil prices are rising not because the world is consuming more, but because tankers cannot safely pass through a war zone. Raising rates in such conditions is an attempt to suppress inflation expectations and prevent them from becoming entrenched in the minds of consumers and businesses. Yet the same measure risks choking an economy that has not fully recovered from previous shocks. The Fed finds itself trapped, and the dollar is rising precisely because of these fears — fears that the regulator may be forced into an extremely unpopular move.

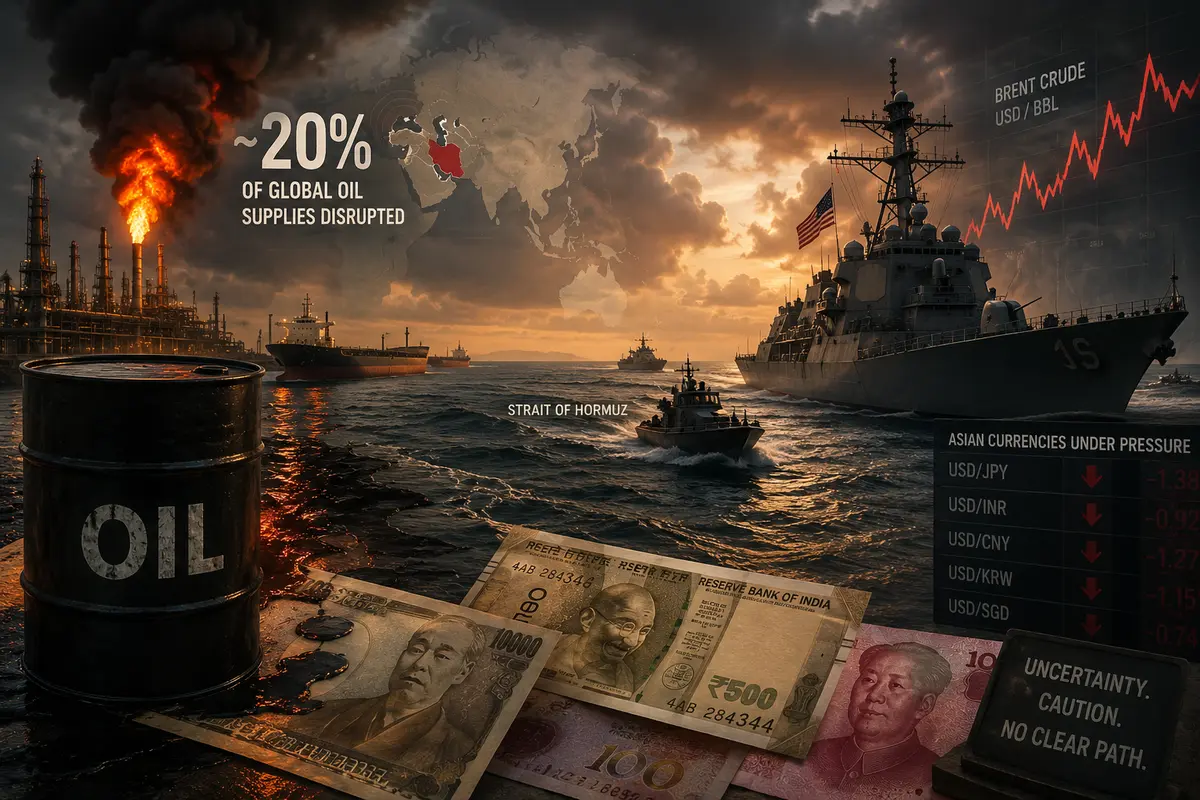

The Oil Fire Fueling the Currency Storm

The war involving Iran has ceased to be background noise and has become the central character in the currency drama. Analysts say one-fifth of global oil supplies has been disrupted — a figure that sounds like dry statistics, but carries very real physical consequences. Refineries across Asia, from Gujarat to Osaka, are receiving less crude. Benchmark oil prices have surged to levels that seemed unimaginable at the start of the year. And although Washington tried to calm markets this week with statements about progress in negotiations, traders are no longer buying the narrative.

The short-term pullback in oil prices following diplomatic optimism turned out to be exactly what it should have been — temporary. Prices retained nearly all of their previous gains. Traders, hardened by bitter experience from past escalations, understand that there is a massive gap between announcing progress and achieving an actual ceasefire. And as long as Iranian patrol boats and American destroyers remain within direct sight of each other in the Strait of Hormuz, any accident could send prices sharply higher again.

This uncertainty is paralyzing Asian currencies. Importers are afraid to lock in long-term contracts, exporters have no idea what exchange rate to use for revenue projections, and central banks from Tokyo to Delhi are sitting atop powder kegs of foreign reserves, reluctant to spend them on interventions amid total uncertainty.

The Yen: A Ray of Hope Amid Broad Weakness

Against this bleak backdrop, the Japanese yen appears to be one of the few islands of relative stability. Its modest strengthening against the dollar stands out from the broader weakness across Asian currencies. The reason lies in growing market confidence that the Bank of Japan may finally move toward a rate hike in June.

This would mark a tectonic shift for the Japanese economy, which has spent decades under ultra-loose monetary policy. But energy inflation caused by the Persian Gulf conflict is hitting Japan particularly hard. A country that imports nearly all of its energy resources now finds itself on the front line of the price shock. Imported inflation is accelerating, and the Bank of Japan — which spent years desperately trying to generate inflation of any kind — now risks getting it in its most painful form for consumers: through soaring gasoline, electricity, and heating costs.

Under these conditions, a rate hike is no longer merely a theoretical exercise but increasingly an inevitability. The market senses this. Bets on a June BOJ hike are rising, giving the yen the support that other Asian currencies currently lack. The paradox is that the yen is strengthening not because Japan is thriving, but because its central bank is being forced to act in crisis conditions.

The Rupee in Freefall and the Silence of Asia’s Tigers

The Indian rupee continues its agonizing decline, marking a seventh consecutive record low. The level of 96.784 represents another painful milestone, with the psychological barrier of 100 rupees per dollar already looming on the horizon. Traders are openly questioning the Reserve Bank of India’s ability to continue defending the national currency. And this is not merely speculative pressure — it is rational calculation.

India, which imports more than 80 percent of its oil, has become one of the most vulnerable victims of the energy crisis. When markets see the central bank burning through reserves on interventions while the currency keeps falling anyway, a snowball effect begins: speculators intensify pressure, knowing reserves are not infinite.

Other Asian currencies remain trapped in sideways trading, but this is the calm before the storm. The Australian dollar has slipped slightly, while the Singapore dollar and South Korean won remain frozen in place. China’s yuan posted marginal gains, though these appear driven more by administrative support from the People’s Bank of China than by genuine market strength.

Asia’s currency market now resembles a theater moments before the curtain rises — everyone knows something dramatic is about to happen, but no one knows where the lightning will strike first. Will it be another Fed rate hike, an escalation in the Strait of Hormuz, or a fresh wave of trade confrontation? Nobody knows. But one thing is obvious to anyone watching the charts: this period of sideways consolidation will not last much longer.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.