Bets Against the Dollar Have Fallen Apart: The Fed Refused to Let Trump “Break” the U.S. Currency

The Dream of Devaluation: How Traders Profited from a Weak Dollar

There was a wonderful moment, about a year ago, when it seemed the U.S. dollar was doomed. Not in a catastrophic sense—not like the Zimbabwean dollar or the Argentine peso. Rather, in a calm, predictable, almost comfortable way: the dollar would gradually lose value. Inflation would steadily erode its purchasing power, like a mouse nibbling away at a piece of cheese. The Federal Reserve, which newly elected President Donald Trump appeared determined to pressure, would keep interest rates low to please the White House. And investors, tired of American financial dominance, would shift their billions into euros, yuan, gold—anything but greenbacks.

The strategy had a sophisticated name: the “debasement trade.” It sounded almost scientific. In reality, it was a simple bet: the dollar would weaken because America no longer wanted a strong dollar. A weaker dollar helps exporters. Trump had long complained about the currency’s strength. Surely he would get his way. Surely the Fed would bend.

The traders who made that bet a year ago earned billions. The U.S. Dollar Index (DXY) fell to its lowest level in eight years. The euro surged to 1.20. The pound climbed to 1.35. American travelers were delighted—their dollars bought more abroad than they had in years. U.S. importers were pleased as well. Exporters complained, but few were listening.

Then something went wrong.

Inflation, which many had written off, came roaring back—not as a visitor, but as the owner of the house. Oil prices soared amid conflict in the Middle East. The U.S. economy, instead of slowing, kept growing: 172,000 jobs were added in May, while unemployment stood at 4.3%. And the Federal Reserve, which Trump had hoped to tame, showed its teeth.

Markets now price in more than a 70% probability of a Fed rate hike in December. The dollar has risen to a two-month high. And traders who bet on its decline are scrambling to close positions, locking in losses—or, at best, breaking even.

Chris Turner of ING, the Dutch bank known for its respected currency research, summed it up in a note today:

“The rise in real rates has put pressure on last year’s dollar debasement trade.”

“Confidence that the Fed would respond to the inflation shock has been a key driver behind the dollar’s recovery over the past month.”

Let’s examine how this trade worked, why it collapsed, and what may come next.

What Was the “Debasement Trade,” and Why Did It Work?

The concept was simple.

Inflation reduces the real value of money. If you have $100 today and inflation runs at 5% per year, those $100 will buy only about $95 worth of goods and services in today’s prices a year from now. That is a loss of purchasing power.

Investors dislike that. When inflation rises, they look for assets that preserve value: gold, real estate, companies with strong pricing power, and currencies issued by countries with lower inflation and higher real interest rates. The eurozone, where inflation was lower than in the United States, appeared attractive. Switzerland even more so. Japan, where deflation had been the norm for decades, also looked appealing.

The trade became obvious: sell dollars and buy euros, pounds, Swiss francs, and yen. Add a little gold for protection, although gold itself had recently behaved less like a traditional safe haven.

In 2025, the strategy worked beautifully. The dollar weakened while alternative currencies appreciated. Traders who went long the euro at the beginning of the year earned returns of 10–15% by year-end, plus interest income.

The key assumption behind the trade was that the Federal Reserve would not raise rates. In fact, markets were pricing in rate cuts during 2026—two, three, perhaps even four of them.

Why did that seem reasonable?

Because after returning to the White House in January 2025, Donald Trump launched a sustained campaign of pressure against the Fed. He publicly criticized Chair Jerome Powell, demanded lower rates, and repeatedly argued that monetary policy should support economic growth.

Many traders concluded that Powell would eventually yield. They assumed that even a formally independent central bank could not indefinitely resist a president who controlled Congress and could potentially seek legislative limits on the Fed’s authority.

History offered a precedent. President Richard Nixon pressured Fed Chair Arthur Burns to keep money easy before the 1972 election. Burns gave in. Inflation later surged into double digits, and the U.S. economy entered a period of stagflation.

The traders betting against the dollar hoped for a repeat of the Nixon-Burns story.

They underestimated two things.

The Two Factors Traders Underestimated

1. The Inflation Shock from the Middle East

In March 2026, Iran and Israel exchanged military strikes. Tensions remain despite a fragile ceasefire.

Oil prices, which had fallen to around $70 per barrel by the end of 2025, rebounded sharply to $90–95. Brent crude trades above $91, while WTI hovers near $88.

For the United States—a net oil importer—higher energy prices mean inflation.

Gasoline becomes more expensive. Plastics become more expensive. Shipping costs rise. Virtually everything becomes more expensive.

Consumer prices in May are expected to have risen 4.2% year-over-year, the highest rate since April 2023.

2. The Resilience of the U.S. Economy

Despite repeated recession forecasts stretching back to 2024, the U.S. economy continues to expand.

The labor market remains the clearest sign of strength: 172,000 jobs added in May, unemployment at 4.3%, real wages rising, and consumers still spending.

When economic growth is strong and inflation remains elevated, the Federal Reserve has little choice. It must raise rates.

Even if the president objects.

Failing to act risks allowing inflation to become entrenched—a far greater threat to long-term prosperity than short-term political pressure.

Powell, who has spent years demonstrating that he is not Arthur Burns, did what markets increasingly expected: he signaled that the Fed would respond to economic realities, not political demands.

Markets listened.

And they reversed course.

How Rate Expectations Flipped

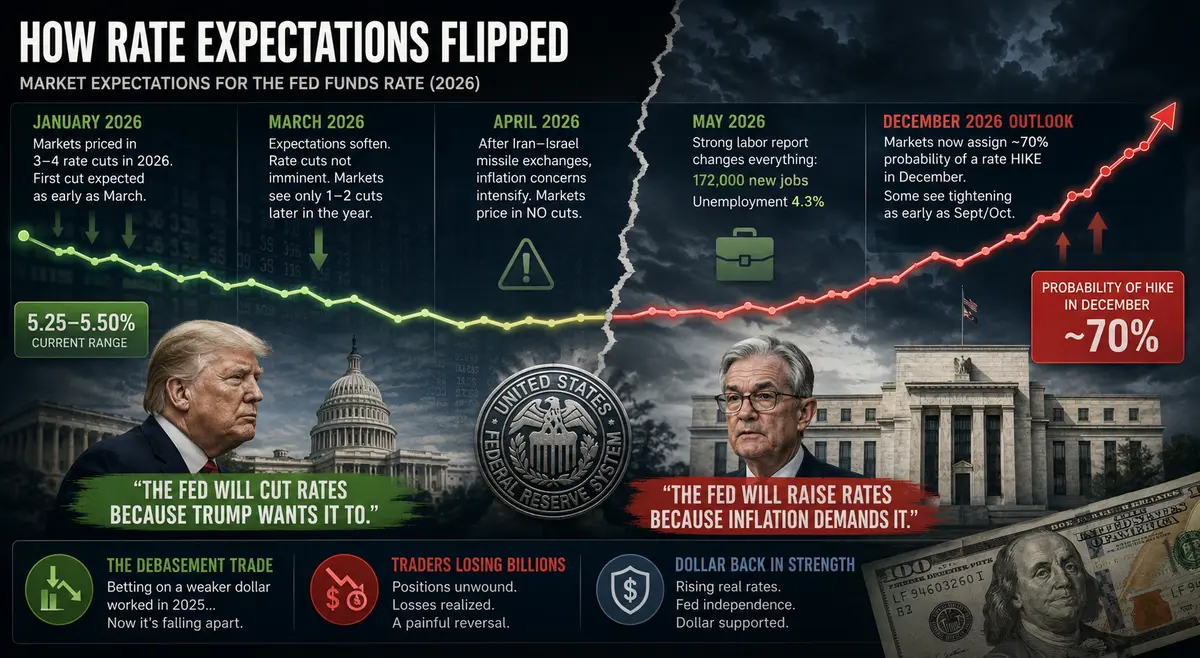

The scale of the shift is evident in federal funds futures, which reflect market expectations for Fed policy.

In January 2026, futures markets priced in three or four rate cuts during the year. The first cut was expected as early as March. By year-end, rates were expected to fall from 5.25–5.50% to around 4.0–4.25%.

By March, those expectations had softened. It became clear that rate cuts were not imminent. Markets adjusted to expecting only one or two cuts later in the year.

In April, after the first missile exchanges between Iran and Israel, inflation concerns intensified. Markets began pricing in no cuts at all.

Then came the May labor-market report released on Friday: 172,000 new jobs and unemployment at 4.3%.

Suddenly, expectations flipped completely.

Markets now assign roughly a 70% probability to a December rate hike. Some investors even see a possibility of tightening as early as September or October if inflation accelerates further.

That is an extraordinary reversal.

In six months, markets went from saying:

“The Fed will cut rates because Trump wants it to.”

to:

“The Fed will raise rates because inflation demands it.”

And traders who bet on dollar debasement have lost billions along the way.

Chris Turner’s View

Chris Turner, ING’s Head of FX Strategy, is known for measured analysis rather than sensational predictions.

His latest note reads almost like an obituary for the debasement trade.

He argues that rising U.S. real interest rates—nominal rates adjusted for inflation—have undermined the strategy. Confidence that the Fed will respond to inflation has become a central pillar supporting the dollar.

For investors, the implication is clear: portfolios may need to be reassessed.

The weak-dollar trade is no longer working, at least over the next six to twelve months. The dollar is likely to remain supported.

Turner does not claim that the dollar has become invincible. The debasement trade is not dead—it is merely dormant.

If inflation falls, if the Fed changes its tone, or if political pressure somehow succeeds in altering policy, the dollar could weaken again.

But as of June 2026, the wind is blowing in the opposite direction.

Why Interest Rates Matter More Than the President

The central lesson is simple:

Real interest rates matter more than political rhetoric.

Trump can advocate a weaker dollar. He can criticize Powell. He can threaten institutional reforms.

But as long as inflation remains elevated and economic growth continues, the Fed retains both the mandate and the ability to tighten policy.

No one—not even Trump—wants a repeat of the 1970s: stagflation, double-digit inflation, unemployment above 10%, gasoline shortages, labor strikes, and social unrest.

That is not the backdrop any president seeking reelection wants to recreate.

As a result, the Fed is likely to continue fighting inflation, even if that means higher interest rates, slower growth, and a stronger dollar.

And traders betting on dollar debasement may continue to suffer until conditions change.

What It Means for Ordinary People

Behind the currency-market drama are tangible consequences for people who never trade foreign exchange and never hold millions in euros.

For Americans, a stronger dollar is positive when traveling abroad. Their money buys more euros, pounds, and yen. European vacations become cheaper.

For consumers who buy imported goods—from smartphones to automobiles, from clothing to furniture—a stronger dollar helps reduce import costs and eases price pressures.

For U.S. exporters, however, the picture is less favorable. Their products become more expensive for foreign buyers, potentially reducing sales and profits.

For Europeans, American goods become more expensive as the euro weakens. Travel to the United States also becomes costlier.

For investors holding dollar-denominated assets, a stronger dollar can boost returns when profits are converted into foreign currencies.

In short, the dollar is once again reclaiming its status as king—at least for now.

What Comes Next?

The outlook for the coming months suggests further dollar strength.

The DXY index, currently hovering around 100, could rise to 102–103 by the end of summer and potentially reach 105 by year-end if inflation remains stubborn.

The euro, which recently attempted to break above 1.20, could retreat toward 1.10–1.12.

The pound could fall toward 1.25–1.28.

The yen, already weak, could slide to 165–170 per dollar, potentially forcing new interventions by the Bank of Japan.

There are risks, of course.

If inflation data comes in below expectations, the dollar could weaken temporarily. If geopolitical tensions in the Middle East escalate, the dollar may strengthen further as investors seek safety.

The biggest uncertainty remains Fed policy itself. If markets prove wrong and the Fed does not raise rates in December, the dollar could decline sharply as investors unwind positions built around higher-rate expectations.

For now, however, momentum favors a stronger dollar.

Trump appears to have lost the battle for a weaker currency.

The Federal Reserve has reinforced its independence.

Investors who bet on dollar debasement are counting their losses.

And the dollar, as if nothing had happened, is climbing back onto the throne.

The old Wall Street saying remains as relevant as ever:

Never fight the Federal Reserve—even if the president is on your side.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.