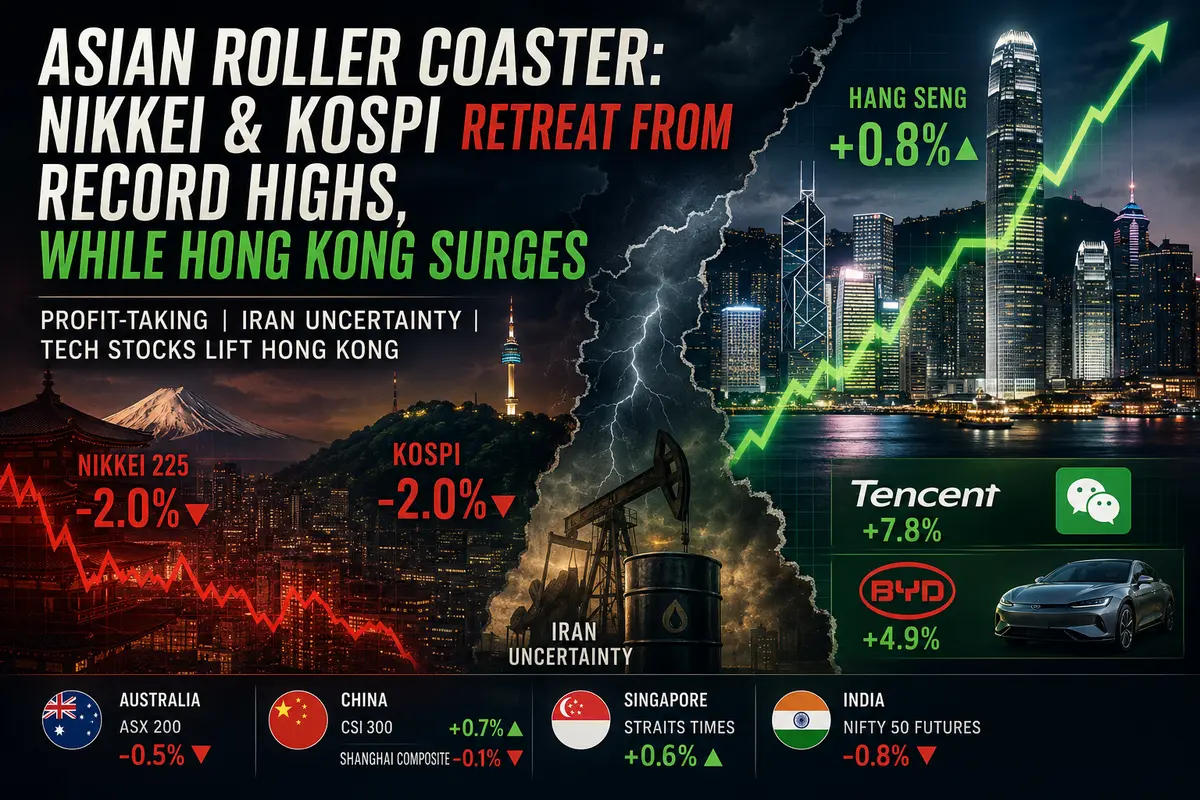

Asian Roller Coaster: Nikkei and KOSPI Retreat from Record Highs While Hong Kong Surges

Asian markets on Tuesday resembled a patchwork quilt stitched together from conflicting signals. Japan’s Nikkei 225 and South Korea’s KOSPI, which had been celebrating record highs just a day earlier, pulled back by roughly 2%. Hong Kong’s Hang Seng, by contrast, gained 0.8%, lifted by heavyweight technology stocks. Chinese indexes moved in opposite directions, Australia’s market fell following hawkish comments from the central bank, and Indian futures pointed to further losses. All of this unfolded against a backdrop of uncertainty surrounding Iran and profit-taking in the semiconductor sector. Tuesday was a reminder that markets cannot rise forever.

Nikkei and KOSPI: Profit-Taking After the May Rally

Japanese and South Korean equities were among Tuesday’s biggest casualties. Both indexes retreated about 2% from the record levels reached in previous sessions. The reason was as old as the market itself: profit-taking. After an impressive May rally fueled by optimism around artificial intelligence, investors decided it was time to lock in gains.

May was a triumphant month for Asian chipmakers. SK Hynix joined the ranks of trillion-won companies, Samsung reached fresh all-time highs after resolving a labor dispute, while Renesas and Rohm posted double-digit gains. Nvidia added fuel to the rally on Monday by unveiling new AI-related products. But every rally, no matter how powerful, eventually runs out of steam. Tuesday was the day the bulls took a breather.

The decline in South Korea was particularly notable because it coincided with disappointing macroeconomic news. Consumer inflation in May reached a 26-month high, exceeding expectations. This immediately strengthened expectations that the Bank of Korea could raise interest rates again before year-end. Higher rates are generally unfavorable for equities, especially technology stocks, which are highly sensitive to borrowing costs. Korean investors responded to the inflation data by selling.

The Iran Factor: Tehran Suspends Communication Through Intermediaries

Geopolitical developments added another layer of nervousness to markets on Tuesday. Late Monday, reports emerged that Tehran had suspended communications with the United States through intermediaries. The news came as a cold shower for investors who had begun to believe that a diplomatic breakthrough might be within reach. If Iran is unwilling to engage even through third parties, the prospects for a settlement become increasingly uncertain.

However, President Trump, as usual, prevented markets from falling into outright pessimism. He stated that negotiations were continuing and that he expected a deal to be reached within the coming week. This is a classic Trump strategy: preventing negative sentiment from taking hold, always leaving room for hope, and always promising a breakthrough just around the corner. Markets, having learned from experience, reacted cautiously. Investors were not fully convinced, but neither did they panic. The result was a mixed performance across regional markets.

The Iran factor continues to influence oil prices, which in turn affect inflation expectations and interest-rate forecasts. It is a feedback loop that keeps markets on edge. Until the situation is resolved, every positive economic development will come with an asterisk: “provided Iran doesn’t…”

Hong Kong in the Green: Tencent and BYD Lead the Charge

Against the backdrop of declines in Japan and South Korea, Hong Kong stood out as a rare bright spot. The Hang Seng gained 0.8%, driven largely by two companies that have not given investors much reason to celebrate lately.

Tencent surged nearly 8% after the Financial Times reported that the company plans to launch an integrated AI agent within WeChat. The implications could be enormous. WeChat is far more than a messaging app—it is an ecosystem through which hundreds of millions of Chinese users communicate, make payments, order food, and shop online. An AI-powered assistant embedded within WeChat could transform it into the next generation of super-apps, helping users with everything from booking rides to making investment decisions. Investors clearly liked the idea.

BYD rose nearly 5%. China’s leading electric-vehicle manufacturer reported its first increase in sales in eight months, ending the longest decline streak in its history. The improvement was driven by overseas deliveries, which offset continued weakness in the domestic market. For BYD shareholders, it was the first meaningful sign of hope in quite some time.

Australia: Hawkish Remarks Weigh on Equities

Australia’s ASX 200 fell 0.5% after Reserve Bank of Australia board member Ian Harper warned that persistent inflation remains a serious challenge. His comments reinforced concerns that additional interest-rate hikes may be necessary. The RBA has already raised rates by 75 basis points since the start of the year, and investors fear that the tightening cycle may not be over.

Higher rates put pressure on Australian equities, which are particularly sensitive to borrowing costs due to the significant weight of banking and resource companies in the market. Investors worry that further tightening could slow economic growth and weigh on corporate earnings.

China: Mixed Signals Continue

Chinese markets delivered a mixed performance. The blue-chip CSI 300 rose 0.7%, while the Shanghai Composite edged slightly lower. The divergence reflects broader uncertainty surrounding China’s economy. On one hand, the property-sector crisis persists and consumer demand remains sluggish. On the other, the government continues to promise stimulus measures, while the technology sector is showing signs of renewed momentum.

Singapore’s Straits Times Index gained 0.6%, while India’s Nifty 50 futures fell 0.8%. The broader picture is one of indecision. Markets are struggling to find direction amid a flood of contradictory signals and lingering uncertainty.

A Day of Reality Check

Tuesday served as a reality check following May’s powerful rally. The Nikkei and KOSPI pulled back from record highs as investors took profits. Hong Kong advanced on strong company-specific stories. Meanwhile, uncertainty surrounding Iran continued to weigh on sentiment.

Markets are waiting for a resolution—either a diplomatic agreement that would ease tensions around the Strait of Hormuz or a new escalation that could send risk assets lower again. Until greater clarity emerges, investors are likely to remain cautious, continue taking profits, and avoid building large positions.

Tuesday showed that the momentum behind May’s rally has faded. Whether this marks the beginning of a broader correction or merely a pause before another leg higher will depend largely on what happens in the Persian Gulf over the coming days.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.