Pound on the Defensive: How Iranian Bombs and Political Calm Put Sterling Back Under the Dollar’s Shadow

Thursday brought a dose of reality to the currency market. The pound sterling, which had recently been trying to find footing for a recovery, came under pressure once again. GBP/USD slipped 0.16% to 1.3405. The move itself was modest, but the direction speaks volumes. Sterling is losing what little support it still had and is reverting to a state of near-total dependence on the dollar narrative. Several factors converged at once: geopolitical tensions flared up again, the dollar reclaimed its safe-haven crown, and Britain’s domestic political story—which had provided at least some independent driver for the pound—has largely run out of steam.

Bandar Abbas and the Retaliation: The Escalation Markets Feared

The night between Wednesday and Thursday shattered the fragile balance markets had been trying to build around negotiations with Iran. U.S. forces struck a military facility near Bandar Abbas, the strategically important port city in southern Iran located at the entrance to the Strait of Hormuz. This was not just another airstrike. It targeted the heart of Iran’s logistical infrastructure and a location that oversees access to one of the world’s most critical oil arteries.

Iran’s response was swift. The Islamic Revolutionary Guard Corps launched an attack on a U.S. airbase, describing it as a “serious warning.” This was no longer a defensive maneuver or a limited operation that could be framed as deterrence. It marked a direct escalation, with both sides exchanging blows and each new strike raising the stakes. The ceasefire that diplomats had been discussing only recently now appears little more than a fiction.

Donald Trump added to the picture by ruling out sanctions relief or the unfreezing of Iranian assets. That erased the cautious optimism seen on Wednesday and triggered broad-based demand for the dollar. Francesco Pesole of ING captured the mood succinctly: the market has returned to a “headline-driven” environment. Every new tweet, every official statement, and every update from the region has the potential to move markets sharply in either direction. In such conditions, the pound—like most currencies—struggles to find a stable footing.

The Inflation Foundation: Why the Dollar Remains Strong

However, attributing dollar strength solely to geopolitics would be a mistake. Beneath it lies a powerful macroeconomic foundation that prevents the U.S. currency from weakening even when Middle East headlines become slightly less alarming. That foundation is inflation.

Back in mid-April, when Brent crude was trading around $95–97 per barrel, markets were pricing in 5–10 basis points of Federal Reserve easing by year-end. Now, after several weeks of hotter-than-expected inflation data, the picture has flipped completely. Markets are currently pricing in approximately 18 basis points of tightening. That is a dramatic shift—from expectations of rate cuts to expectations of rate hikes. This reversal continues to support the dollar regardless of how negotiations with Iran evolve.

For sterling, this means that even temporary improvements in the geopolitical backdrop are unlikely to provide meaningful relief. The dollar is not strong simply because conflict is raging somewhere. It is strong because the U.S. economy remains overheated, inflation is proving persistent, and the Federal Reserve stands ready to maintain a hawkish stance. Until that foundation changes, sterling is likely to remain in the shadows.

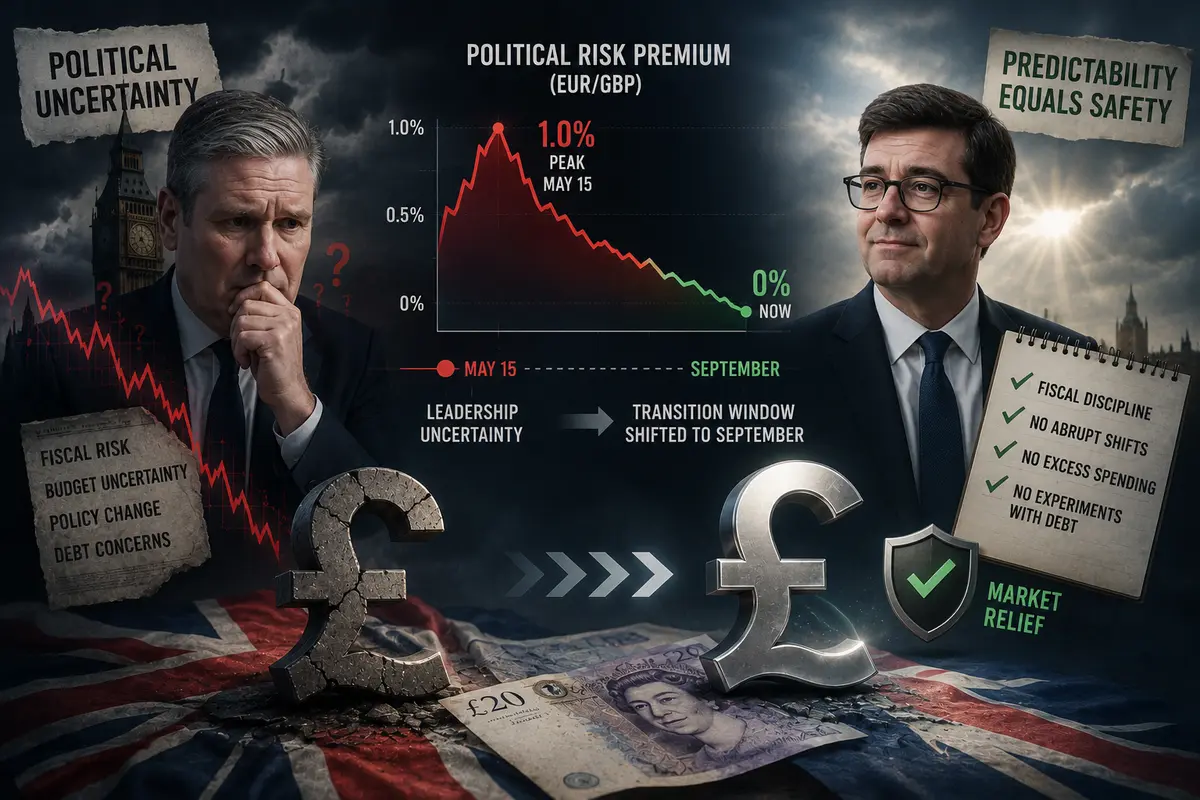

The Political Risk Premium Has Evaporated: From Starmer to Burnham

The pound did have its own narrative for a while—one that offered some independence from the dollar story. That narrative revolved around political risk.

In mid-May, speculation emerged regarding Prime Minister Keir Starmer’s leadership. The possibility of political change, uncertainty surrounding fiscal policy, and the risk of significant budgetary shifts all contributed to a political risk premium weighing on sterling.

That premium peaked at roughly 1% in EUR/GBP terms on May 15. Since then, it has fallen to zero. Why? Because leadership contender Andy Burnham adopted a market-neutral stance on fiscal policy, pledging to maintain existing borrowing parameters. Investors who had feared fiscal populism breathed a sigh of relief. No abrupt policy shifts, no excessive spending, and no experiments with public debt. Burnham turned out to be predictable—and for markets, predictability equals safety.

Moreover, the most likely window for any leadership transition has shifted toward September. That makes it difficult for the issue to be reflected in current volatility levels. Political risk has not disappeared; it has simply moved far enough into the future that markets have stopped paying attention. Once the political story fades into the background, sterling once again becomes fully exposed to the external dollar narrative.

The Bank of England and the Oil Trap

There is another factor depriving sterling of structural support: the Bank of England and its battle against inflation.

The Bank’s path toward lower inflation has been complicated by surging oil prices, which have risen by more than 50% since the start of the Iranian conflict. Higher energy costs feed directly into consumer prices, pressure businesses, and reduce policymakers’ room for maneuver.

Like many central banks, the Bank of England finds itself trapped. On one hand, inflation argues for higher interest rates. On the other, economic growth is slowing, and further tightening could significantly weaken the economy. In this environment, sterling cannot count on strong support from monetary policy. Rates may remain elevated, but they are unlikely to rise aggressively enough to attract substantial capital inflows. Without that support, the pound remains vulnerable to dollar strength.

PCE and the ECB: Events That Could Move Markets

The key event on Thursday is the release of April core Personal Consumption Expenditures (PCE) data. PCE is the Federal Reserve’s preferred inflation gauge, and it plays a crucial role in shaping interest-rate expectations.

ING forecasts monthly core PCE growth of 0.3%, below the market consensus of 0.5%. If that forecast proves accurate, the dollar could weaken slightly. However, it is unlikely to trigger a significant reassessment of Fed policy toward easing. Too many strong inflation readings have already accumulated.

Markets are also awaiting the release of the ECB’s April meeting minutes. They are expected to reinforce expectations of a rate increase on June 11. However, markets have already priced in roughly 21 basis points of tightening, suggesting the euro’s reaction may be limited. A speech by Christine Lagarde could add some intrigue, but it is unlikely to transform the broader market narrative.

ING sees support for EUR/USD around 1.1580–1.1590 but warns that this area may not hold if tensions between the United States and Iran deepen further. A test of the 1.1500 level is considered a realistic risk. For sterling, that means even a relatively stable euro is unlikely to provide protection. If the dollar continues to strengthen on the back of geopolitics and inflation, the pound is likely to decline alongside other major currencies.

Conclusion

Thursday left sterling in a vulnerable position. Geopolitical tensions remain elevated, the dollar is firmly supported, the political risk premium has evaporated, and the Bank of England is constrained in its policy options.

The pound is once again returning to the role of a follower, heavily dependent on developments in Washington and Tehran. As long as missiles continue to fly across the Middle East and the Federal Reserve keeps a firm grip on monetary policy, sterling’s best strategy may simply be to endure and wait.

Wait for geopolitical tensions to subside. Wait for the macroeconomic winds to shift. But judging by current conditions, that wait could be a long one.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.