Diplomacy in Ruins: How a New Strike on Iran Restored the Dollar’s Strength and Brought Fear Back to Markets

Monday ended with explosions. By Tuesday, markets woke up in a different world — one where hopes for imminent peace, which had lifted Asian stocks and currencies just a day earlier, were shattered by the harsh reality of military force. The United States carried out strikes on targets in southern Iran. Although details remain scarce and official statements cautious, that alone was enough for the markets. The dollar resumed its climb. Oil surged alongside it. Asian currencies, which had celebrated gains on Monday morning, came under pressure by Tuesday. The geopolitical pendulum swung back — and this time, those who had rushed to believe in peace were the ones falling.

Strikes on Southern Iran: What We Know and Why It Matters

Reports of new U.S. strikes on Iranian facilities emerged on Monday. The targets were located in the south of the country — a region strategically important both for Iran’s military infrastructure and for control over the Persian Gulf coastline. Details of the operation remain classified, but the mere resumption of military action after several days of intense negotiations suggests either that diplomacy has hit a dead end or that talks are being used as cover for continued military pressure.

Iranian officials reacted immediately. Their warning was blunt and unequivocal: any attacks on the country’s military facilities would trigger retaliation. This was not rhetoric — it was a promise of escalation. Markets interpreted it exactly that way: as a signal that the conflict is far from over and that the risks of a new spiral of violence are growing by the hour.

The contrast with the mood over the weekend could not be sharper. As recently as Saturday and Sunday, Trump had spoken about a memorandum that was “mostly agreed upon,” about reopening shipping routes through the Strait of Hormuz, and about Iran transferring enriched uranium. On Monday, shortly before the strikes, he repeated the same optimistic narrative. Yet just hours later, American aircraft were bombing Iranian territory. What happened in between — whether negotiations collapsed, the strike had been planned in advance, or it was a response to actions by Tehran — remains unclear to the markets. But traders do not need the full picture. One fact is enough: the war continues, peace is postponed.

The Oil Pump: Crude Prices Surge Again

The first and most predictable consequence of the strikes was a spike in oil prices. A market that had celebrated Brent crude falling below $100 per barrel on Monday morning watched prices reverse sharply upward by evening. Analysts describe it as a “partial recovery of recent losses.” Behind that dry language, however, lies panic among importers and frantic budget recalculations by airlines, transportation firms, and petrochemical plants around the world.

Oil is once again becoming a weapon — or more precisely, fear of supply disruptions from the Persian Gulf is once again being priced into every barrel. The Strait of Hormuz, which over the weekend seemed almost open for normal shipping, once again looks like a war zone. And while Iranian officials threaten retaliation, nobody can guarantee that tankers entering the strait will emerge unharmed. The geopolitical risk premium is returning. And with it comes renewed inflationary pressure that only yesterday appeared to be easing.

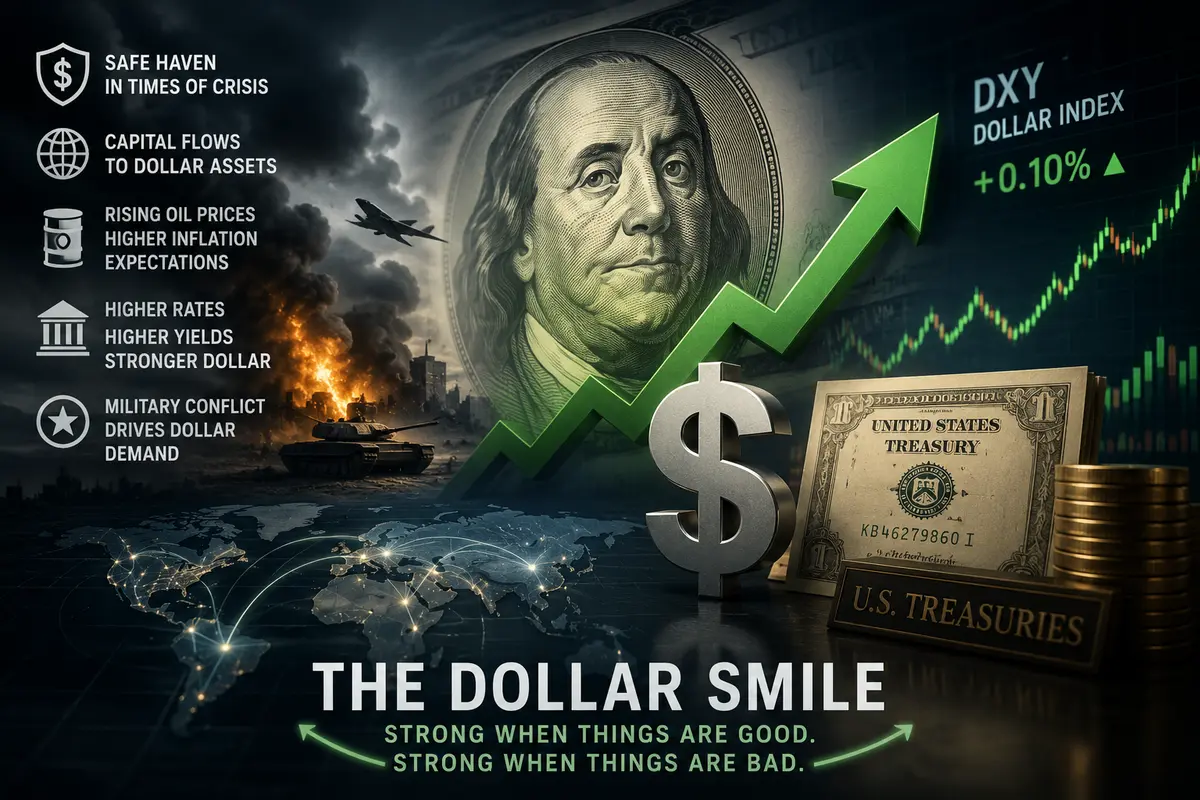

The Dollar as a Safe Haven: A Familiar Pattern

The strengthening of the dollar on Tuesday was a textbook response to geopolitical stress. When the world becomes dangerous, capital seeks shelter. And regardless of how much the financial landscape changes, the primary safe haven remains the U.S. dollar. The dollar index and dollar futures both rose by a modest one-tenth of a percent. The move itself was small, but the direction was telling. Demand for the dollar has returned.

The mechanics behind this demand are multilayered. First, investors pull money out of risk assets — emerging-market equities and high-beta currencies — and move it into dollar-denominated instruments. Second, rising oil prices reinforce inflation expectations, increasing the likelihood that the Federal Reserve will keep interest rates elevated or even raise them further. Higher rates mean higher yields on dollar assets, making the currency even more attractive. Third, military conflict involving the United States itself creates additional demand for dollars from defense contractors, logistics networks, and related industries.

Together, these forces create the classic “dollar smile” effect: the U.S. currency strengthens both when everything is going well and when everything is going terribly wrong. This is clearly the latter case.

Asian Currencies: Who Suffered Most

Asian currencies, which had rallied together on Monday amid hopes for peace, reversed course just as collectively on Tuesday. The Indian rupee, which had strengthened after comments from the RBI governor and rebounded from record lows, once again came under pressure — the USD/INR pair rose by three-tenths of a percent. For India, which imports more than 80 percent of its crude oil, the rebound in oil prices immediately renews pressure on both the trade balance and the currency. Central bank interventions — verbal or actual — only work when fundamentals are supportive. When oil starts climbing again, even the most determined central bank can merely slow the decline, not stop it.

The Chinese yuan weakened slightly, and the Singapore dollar followed. The Australian dollar, traditionally viewed as a proxy for global risk appetite, slipped by one-tenth of a percent. The move was modest, but it reflected the broader mood: investors are cautious again, pulling away from risk and rotating back into defensive assets.

The only exception to the pessimistic trend was the South Korean won. USD/KRW declined thanks to a rally in the local stock market. Korean equities rose on domestic drivers, including strength in the technology sector and optimism following the recent resolution of a labor dispute at Samsung Electronics. But the exception merely proved the rule: when geopolitics strikes the markets, most emerging-market currencies suffer.

The Bank of Japan and the Yen: Himino’s Signal

The Japanese yen was virtually unchanged on Tuesday, remaining near recent levels. But that calm may be deceptive. Deputy Governor of the Bank of Japan Ryozo Himino made remarks that could have far-reaching implications. According to him, the central bank will consider developments in the Middle East when evaluating future policy adjustments.

That is an important signal. For decades, the Bank of Japan pursued ultra-loose monetary policy regardless of external shocks. If it is now prepared to factor geopolitical risks into interest-rate decisions, that means a rate hike next month is becoming more likely. Markets are already pricing this in. The yen, which normally would weaken alongside a stronger dollar, is holding relatively stable precisely because of these expectations.

Yet there is also a paradox here. Raising rates while the global economy suffers from an oil shock and military uncertainty could prove risky. Japan’s economy depends on imported energy no less than India’s. Higher rates combined with higher oil prices would represent a double blow for businesses and consumers alike. Himino and his colleagues will be forced to balance the need to support the yen against the risk of choking economic growth.

A Peace Once Again Delayed

The U.S. strikes on southern Iran reminded markets of a brutal truth: in geopolitics, progress is not a guarantee, and hope is not a strategy. The weekend brought hope for peace. Monday brought bombs. And that sequence perfectly illustrates the nature of the current crisis. It is not linear. It does not evolve along a predictable path from escalation to de-escalation. It pulses, jerks violently, takes one step forward and two steps back.

For currency markets, such an environment is toxic. It is impossible to build long-term positions when every new headline can completely reverse the picture. It is impossible to hedge risks when nobody knows whether tomorrow will bring a peace agreement or another missile strike. All that remains is reaction. And on Tuesday, the reaction was unmistakable: a rush into the dollar. The old reliable dollar, which seems to benefit every time the world becomes a more dangerous place. Asia, which was celebrating yesterday, is nursing its wounds today. And there is still no end in sight to these swings.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.