Why BofA Remains Bearish on the Euro

An American View of a Currency That Still Cannot Take Off

Bank of America, one of the world’s largest financial institutions, has not changed its view on the euro. It looks at the single European currency with caution bordering on pessimism — not catastrophic or panicked, but rather weary and pragmatic. BofA analysts see too many factors that will weigh on the euro in the coming months, and too few that could support it.

The euro is going through a difficult period. It is not collapsing, but it is not rising either. It is moving sideways around 1.16–1.17 against the dollar, sometimes slightly higher, sometimes slightly lower. Investors who just a year ago believed in a quick return to 1.20 and above are now simply hoping it will not fall to 1.10.

BofA offers no false hopes. Its analysts believe pressure on the euro will persist at least through the second and third quarters. Only toward the end of the year, if energy markets begin to normalize and eurozone growth improves, may the single currency have a chance to recover.

But what exactly is holding the euro back? Why can a currency serving an economy of 450 million people and GDP of 15 trillion euros not strengthen against the dollar? The answers lie in three areas: energy, economic growth, and geopolitics.

Europe’s Energy Curse

The first and perhaps main reason for the euro’s weakness is Europe’s energy vulnerability. BofA says directly: Europe remains more vulnerable to rising energy costs than the United States. This is not new, but under current conditions this vulnerability is becoming critical.

Natural gas prices have historically had a much stronger impact on the eurozone economy. European industry, especially Germany’s, was built on cheap Russian gas. After the start of the war in Ukraine and the subsequent break in relations with Russia, Europe shifted toward liquefied natural gas from the United States and Qatar — but it is more expensive. Much more expensive.

Now the Middle East factor has been added. The conflict between the United States and Iran, strikes on Qeshm Island in the Strait of Hormuz, threats to block shipping — all of this is pushing oil and gas prices higher. Europe, still dependent on imported energy, is being held hostage by the situation.

BofA analysts note that energy futures markets still reflect relatively optimistic expectations, especially regarding the Middle East. For some reason, markets are hoping the conflict will not expand, that negotiations will still happen, and that the Strait of Hormuz will remain open. But if those hopes fail, energy prices will surge — and the euro will fall.

For the United States, high energy prices are a problem, but not a catastrophe. America produces its own oil and gas and has become a net exporter. High prices can even benefit U.S. producers. For Europe, however, they are a pure negative. Every extra dollar per barrel of oil means billions of euros flowing out of the European economy.

America’s Growth Advantage

The second reason behind BofA’s bearish view on the euro is the difference in economic growth rates between the United States and the eurozone. And that difference is not in Europe’s favor.

U.S. macroeconomic data is expected to remain stronger than eurozone figures. This is not a short-term spike, but a structural advantage. BofA names two reasons why America will continue to grow faster than Europe.

The first is investment in artificial intelligence. The United States is the global leader in this field. NVIDIA, Microsoft, Google, Amazon, Meta — all these companies are based in America, and all are investing tens of billions of dollars in AI development. These investments create jobs, stimulate demand, support the stock market, and ultimately strengthen the dollar.

Europe is lagging in the AI race. There are individual companies — such as France’s Mistral AI, Germany’s Siemens and SAP — but their scale is not comparable to the American giants. European investors prefer putting money into U.S. AI companies rather than European ones. Capital is flowing across the Atlantic.

The second reason is fiscal stimulus. The United States has passed several fiscal support packages in recent years — the CHIPS Act, the Inflation Reduction Act, and the infrastructure law. The money has already begun flowing into the economy: factories are being built, jobs are being created. Europe is also trying to stimulate its economy, but its capacity is limited by the eurozone’s strict budget rules.

Germany, Europe’s economic heart, has been in recession for several quarters. France is balancing on the edge. Italy, Greece, and Spain are countries with huge debts and cannot afford large-scale stimulus.

While America grows, Europe stagnates. And this is reflected in exchange rates.

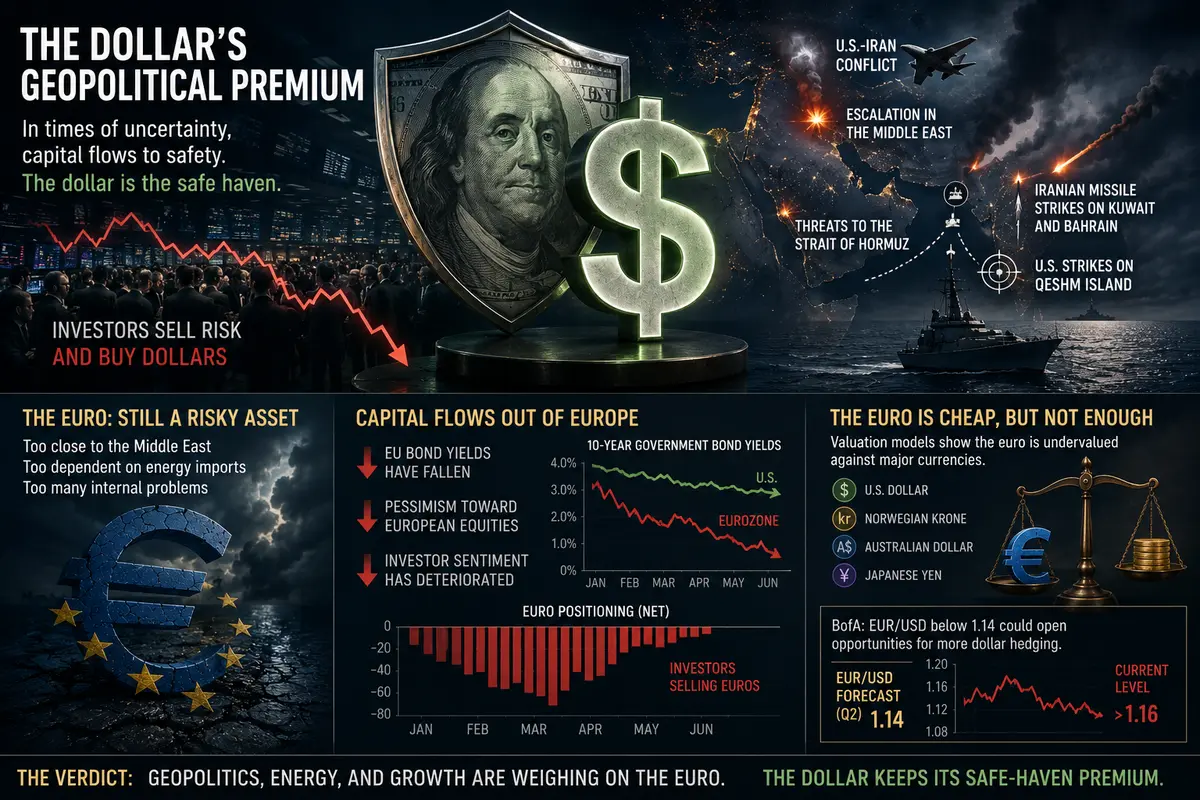

The Dollar’s Geopolitical Premium

The third reason is geopolitics. The dollar remains the world’s main safe-haven currency. When the world is unstable, capital runs into the dollar. And the world is very unstable right now.

The conflict between the United States and Iran. Escalation in the Middle East. Threats to the Strait of Hormuz. Uncertainty around negotiations. Iranian missile strikes on Kuwait and Bahrain. U.S. strikes on Qeshm Island.

All of this pushes investors to sell risky assets and buy dollars. The euro, unfortunately, is still viewed as a risky asset. It is not a safe haven. It is the currency of a region that is too close to the Middle East, too dependent on energy imports, and burdened with too many internal problems.

Investor sentiment toward Europe has already deteriorated noticeably. European bond yields have fallen since the beginning of the Middle East conflict — a sign that investors are moving away from European risk into safer assets. Surveys show growing pessimism toward European equities. Capital has recently been flowing out of the region.

BofA captures this in its models. Positioning in the euro and investor sentiment have softened in recent weeks — a mild way of saying that investors are selling the euro. And the bank’s analysts see no reason why this trend should reverse soon.

What About Valuations? The Euro Is Cheap, But That Does Not Help

The euro does have one potential advantage — it is cheap. The valuation models used by BofA suggest that the euro remains undervalued against several major currencies, including the U.S. dollar, the Norwegian krone, the Australian dollar, and even the Japanese yen, which itself is near historical lows.

In theory, undervaluation should attract buyers. If an asset is cheaper than it should be based on fundamentals, sooner or later investors should want to buy it. That is how markets work.

But in practice, fundamental factors are currently working against the euro more strongly than undervaluation is supporting it. Energy, growth, geopolitics — these three pillars are weighing on the single currency. Until they weaken, the euro will remain weak despite being cheap.

BofA, however, does not deny that valuation may eventually prevail. The bank’s analysts note that EUR/USD levels below their second-quarter forecast of 1.14 could create opportunities to increase dollar hedging. If the euro falls to 1.14, those hedging dollar risks may begin buying euros to close their positions. That could create support.

But for now, 1.14 is still some distance away. The euro is trading above 1.16. There is room to fall.

The ECB: Hawk or Dove

A separate issue is the policy of the European Central Bank. Markets expect the ECB to raise rates by 25 basis points at next week’s meeting. This would be the eighth hike in just over a year.

BofA believes the ECB will take a hawkish stance to preserve expectations of further tightening and keep inflation expectations under control. Inflation in the eurozone, though it has slowed, remains twice the target level. The ECB cannot afford to relax.

But a hawkish ECB is a double-edged sword. On one hand, higher rates support the currency. Investors like currencies of countries with high interest rates. On the other hand, high rates hurt an economy that is already barely breathing.

BofA warns that if the ECB becomes too strict, it could worsen the eurozone downturn. And an economic downturn means a weaker euro — even with high rates. Investors would fear that the ECB is killing the economy and would move out of the euro.

On the other hand, if the ECB sounds dovish and hints at a pause in rate hikes, the euro will fall immediately because the yield gap between the euro and the dollar will begin narrowing.

In short, the ECB is caught between a rock and a hard place. Any move could turn out to be wrong. BofA does not appear to expect miracles from the ECB. The bank’s analysts believe central bank policy can support the euro only under one condition: inflation remains under control and the regulator avoids tightening beyond current market expectations.

In other words, the best thing the ECB can do for the euro is nothing. Do not surprise markets. Do not raise rates more than already priced in. Be predictable. Boring. Then investors, at least, will not panic.

What Could Save the Euro

Despite its bearish short-term view on the euro, BofA maintains a more constructive long-term forecast. The bank’s analysts expect the situation to begin improving in the second half of the year.

What could save the euro? First, normalization in energy markets. If the Middle East conflict de-escalates, if a ceasefire can be reached, if the Strait of Hormuz remains open, oil and gas prices will fall. Europe will breathe more freely. Industry will begin to recover. The euro will strengthen.

Second, improved eurozone growth. The economy may have hit bottom. Stabilizing energy prices, easing inflation pressure, and rising real household incomes could lead to a recovery in consumption and investment. By the fourth quarter, BofA hopes, the European economy will begin to show signs of life.

Third, efforts to strengthen the euro’s international role. The ECB and European politicians have long said that the euro should become a more important reserve currency. So far, these words have remained only words. But if real steps appear — for example, creating a single capital market or issuing eurobonds to finance common projects — the euro could receive support.

Fourth, progress on European reforms. BofA calls this the main upside risk for the currency. If Europe finally carries out long-delayed reforms — completing the banking union, creating a fiscal union, simplifying the regulatory environment for business — confidence in the euro will rise. And confidence means strength.

But all these “ifs” belong to the realm of fantasy for now. Europe is not showing progress in any of these areas. Reforms are stalled. The energy transition is moving slowly. Political uncertainty in France and Germany does not add optimism.

Risks: What Could Go Wrong

BofA lists three main downside risks for the euro. The first is rising energy prices. If the Middle East truly erupts, oil could move to $120–130, and gas to $2,000 per thousand cubic meters. The European economy would collapse. The euro would fall to 1.10 or lower.

The second is a more hawkish ECB. If the central bank, while fighting inflation, raises rates more than markets expect, it could trigger a recession. And the euro would fall — even despite the formal support of higher interest rates.

The third is political uncertainty in France. France is the eurozone’s second-largest economy, and its political stability is critical for the euro. Recent polls show growing support for both right-wing and left-wing radicals, creating the risk of a political crisis after the next elections. If France shakes, the euro will shake too.

BofA is not being dramatic. Its analysts are simply listing the facts. But those facts are troubling.

What It Means for Investors

For investors holding euros or European assets, BofA’s recommendation is clear: be cautious. Do not expect a rapid strengthening of the euro. Be prepared for the dollar to remain stronger in the coming months.

If you are hedging currency risks, it may make sense to increase hedging now. BofA says directly that EUR/USD levels below its second-quarter forecast of 1.14 could create opportunities to increase dollar hedging. In other words, if the euro falls to 1.14, that could be a good point to sell dollars and buy euros, because further downside may be limited.

If you are a speculator, you may consider short positions in the euro — but carefully. The market has already priced in a lot of negativity. Unexpectedly good news from Europe could trigger a sharp rebound.

If you are a long-term investor buying European assets for years ahead, current euro weakness may even be good news. You are buying a cheap currency. If the European economy eventually recovers, you could benefit twice — from rising assets and from a stronger euro.

BofA maintains a bearish short-term view on the euro. But this is not a verdict. It is simply analysis. Markets change, circumstances change, and what is true today may prove wrong tomorrow.

The euro has survived harder times. In 2000, it fell to 0.82 against the dollar. In 2008, it rose to 1.60. It survived then. It will survive now. The only question is how long the recovery will take — and at what cost.

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.