Asian Currencies Stabilize After a Dollar-Driven Selloff

A Chance to Catch Their Breath

Thursday brought a welcome pause to Asia’s currency markets. After several days of relentless pressure from the U.S. dollar—rolling through markets like a tank—things finally calmed down. Asian currencies, which had been losing ground day after day, stopped falling. They are not rising yet, but they are no longer sliding either. For now, they have dug in and are waiting.

The U.S. Dollar Index (DXY), the main gauge of the dollar’s strength against a basket of six major currencies, also held steady. Just a day earlier, it had climbed to a two-month high. Two months may not sound like much, but in the currency market, that is a meaningful stretch. The dollar has not been this strong since the spring, when markets were gripped by another round of anxiety over the Federal Reserve and inflation.

Now comes a pause. Traders are taking a breath, reassessing positions, and scanning economic calendars for the next major catalyst. And there are plenty of them ahead. Any one of them could tip the balance further in favor of the dollar—or spark a recovery in battered Asian currencies.

So what happened over the past few days? Why has the dollar suddenly become so strong? And why do Asian currencies remain under pressure despite this temporary stabilization?

There are several reasons, all tightly intertwined in a knot that analysts around the world are trying to untangle.

The Middle East: A Ceasefire That Solves Little

The first and most obvious driver of dollar strength is geopolitics.

The Middle East has been on edge all week. Iran and the United States exchanged airstrikes. Missiles were launched toward Kuwait and Bahrain. U.S. forces struck Iran’s Qeshm Island—the strategic outpost guarding the Strait of Hormuz, through which roughly one-fifth of the world’s oil supply passes.

In such an environment, investors do what they always do: they flock to the U.S. dollar.

The dollar remains the world’s premier safe-haven currency. When uncertainty rises and markets become fearful, investors seek shelter in dollars. Better than the euro, which faces its own challenges. Better than the pound, still dealing with the long shadow of Brexit. Better than the yen, which has its own ongoing battle with the psychologically important 160 level.

The dollar is the financial equivalent of a bunker.

Then, on Thursday morning, news emerged that briefly allowed markets to exhale. Washington announced a ceasefire agreement between Israel and Lebanon. Just hours earlier, few believed such an outcome was possible. Negotiations had been difficult, with both sides accusing each other of violating commitments. Then suddenly, a breakthrough.

Yet the relief was limited.

Diplomats emphasized that the agreement depends on a cessation of hostile actions by Hezbollah. And Hezbollah remains an unpredictable actor, not always responsive even to its own backers. As a result, investors have been reluctant to rush back into risk assets. Instead, they are waiting to see whether the ceasefire holds.

Moreover, an agreement between Israel and Lebanon does not eliminate broader regional tensions. Iran remains hostile. U.S. military operations continue. Kuwait and Bahrain, both targeted earlier in the week, have yet to respond. Qeshm Island remains a flashpoint.

There are simply too many hotspots for markets to relax completely.

That is why Asian currencies have stabilized—but have not yet started to recover. This is a pause, not a reversal.

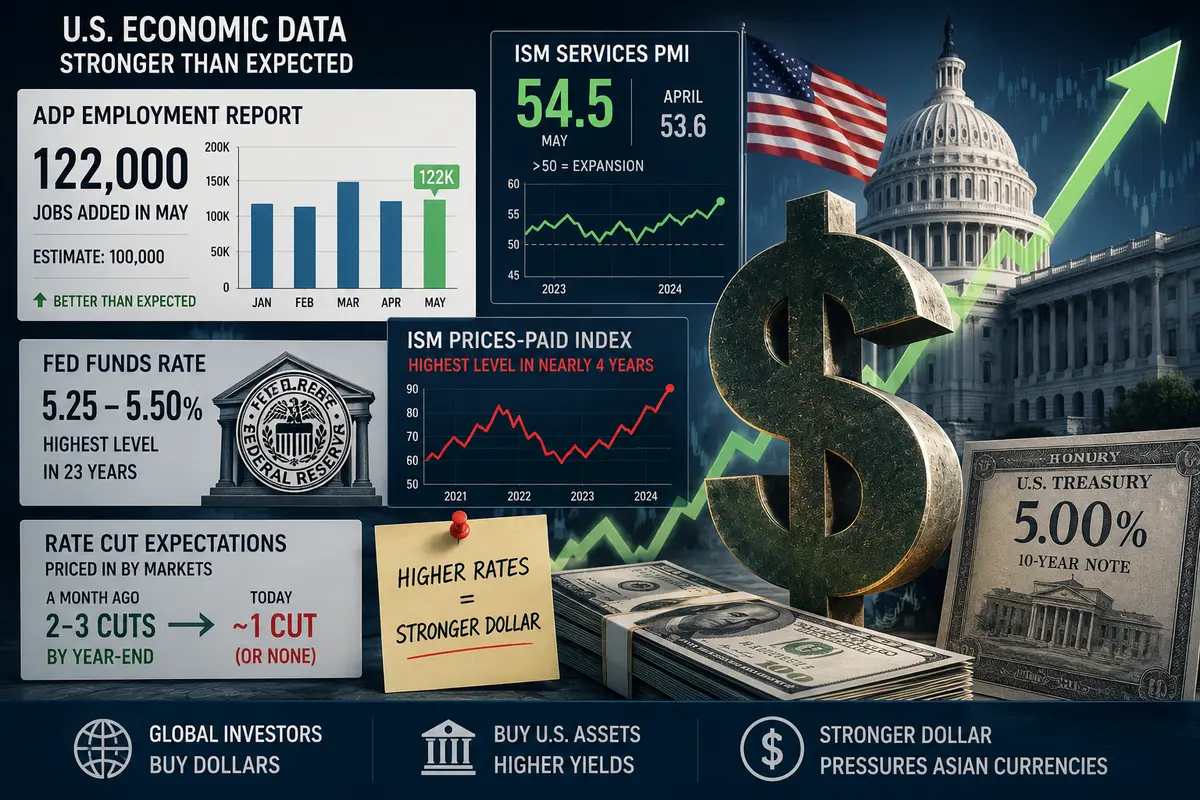

The Fed and U.S. Economic Data: Stronger Than Expected

The second major source of dollar strength is the latest U.S. economic data.

Wednesday’s numbers were strong—very strong.

First came the ADP employment report, often described as a smaller preview of the official nonfarm payrolls report. According to ADP, U.S. employers added 122,000 jobs in May. While not a spectacular number, it exceeded expectations. Markets had anticipated roughly 100,000.

The labor market continues to show resilience despite high interest rates, inflation concerns, and geopolitical uncertainty.

Next came the Institute for Supply Management’s (ISM) Services PMI. The index rose to 54.5 from 53.6 in April. Any reading above 50 indicates expansion—and this expansion appears to be accelerating.

The services sector, which accounts for the majority of the U.S. economy, remains healthy. Consumers are still dining out, traveling, and spending on everyday services. The economy is not merely surviving—it is growing.

However, the most concerning detail for those hoping for imminent Federal Reserve rate cuts was buried deeper within the same ISM report.

The prices-paid component—a measure of what businesses are paying for goods and services—jumped to its highest level in nearly four years.

That suggests inflationary pressures are not fading. In fact, they may be intensifying.

For the Federal Reserve, this is unwelcome news. The Fed’s primary mission is price stability. If inflation remains stubbornly high, interest rates may need to stay elevated for longer—or even rise further.

Markets understand this perfectly well.

A month ago, traders were pricing in two or three rate cuts before year-end. Today, expectations have shrunk to perhaps one cut, and even that remains uncertain. Some analysts now openly discuss the possibility that the Fed may not cut rates at all this year. A few pessimists have even begun mentioning the possibility of another hike.

For the dollar, this is music to its ears.

Higher interest rates make U.S. assets more attractive. Investors around the world buy dollars to invest in U.S. Treasury securities yielding around 5% annually. Demand for dollars rises—and Asian currencies inevitably come under pressure.

The Yen: Dancing on the Edge

No currency has attracted more attention in this drama than the Japanese yen.

On Thursday, USD/JPY traded around 159.97—just shy of the crucial 160 level.

That number matters.

Back in April, Japanese authorities described 160 as a “red line.” At the time, they spent a record $73 billion on currency intervention to push the exchange rate lower. It worked—but only temporarily.

Now the yen is back at the same level.

Traders can sense the tension. They know the Japanese government cannot spend tens of billions of dollars every few months indefinitely. Tokyo’s reserves are substantial, but they are not unlimited.

Eventually, the Ministry of Finance will have to either tolerate a weaker yen or develop a more aggressive strategy.

Bank of Japan Governor Kazuo Ueda hinted at one possible direction on Wednesday. He stated that policymakers may need to consider raising interest rates if inflation risks become more significant than risks to economic growth.

The wording was cautious, but the message was clear:

The Bank of Japan is willing to raise rates if necessary.

That matters because Japan spent decades battling deflation. Now inflation has become a genuine concern. Prices are rising, and policymakers may no longer be able to ignore them.

Higher Japanese rates would support the yen by narrowing the interest-rate gap between Japan and the United States.

However, higher rates also pose risks for an economy accustomed to ultra-cheap money. That is why Ueda remains careful with his language. He is not promising hikes—he is merely keeping the option open.

Markets, however, heard what mattered most: the door is no longer closed.

Analysts at ING noted that traders are likely to continue testing the upper limits of USD/JPY. June is traditionally a seasonally weak month for the yen, meaning the dollar may once again attempt to break decisively above 160.

If that happens, Japanese authorities may be forced to respond.

The only question is how.

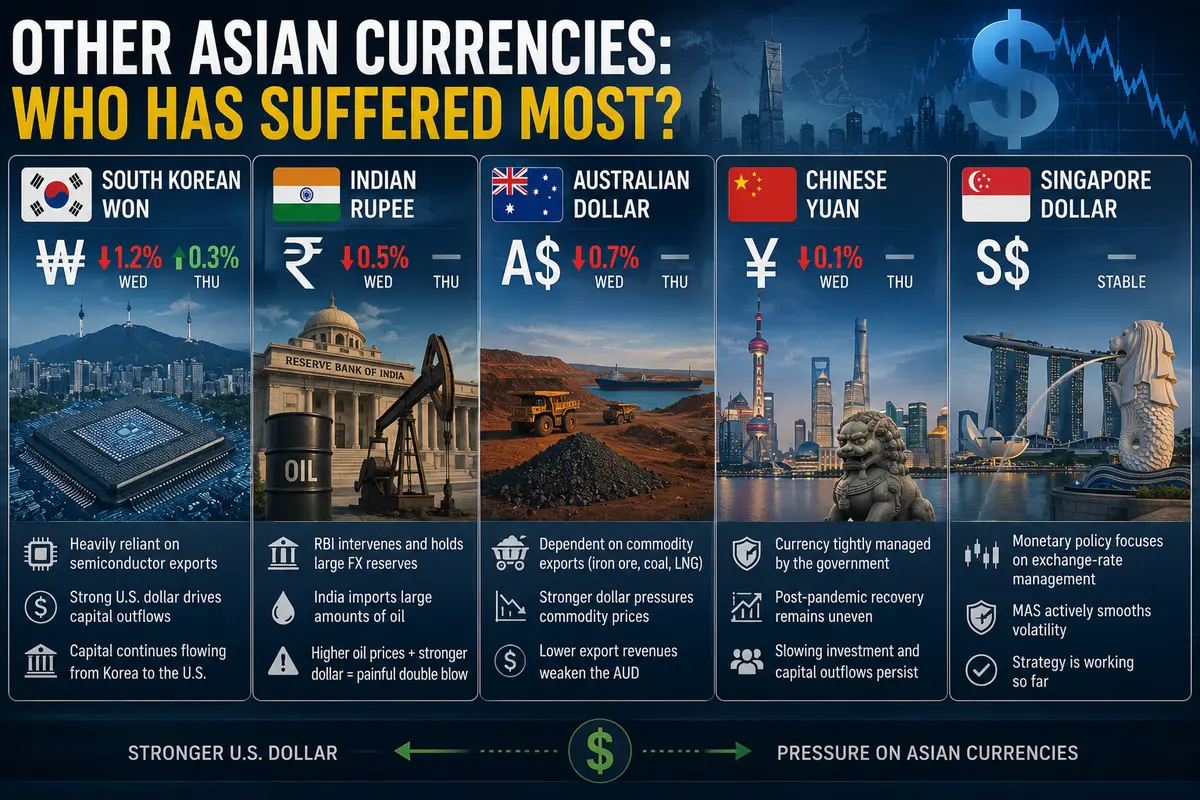

Other Asian Currencies: Who Has Suffered Most?

South Korean Won

The won fell 1.2% in the previous session—a substantial overnight move. On Thursday, it recovered just 0.3%, barely making a dent in the prior day’s losses.

South Korea remains heavily dependent on exports, particularly semiconductors. While the AI boom has boosted chip demand, strong semiconductor sales alone cannot offset the pressure created by a powerful U.S. dollar.

Capital continues flowing from Korea into the United States, weighing on the currency.

Indian Rupee

The rupee lost 0.5% on Wednesday before stabilizing on Thursday.

The Reserve Bank of India actively manages exchange-rate volatility and possesses significant foreign-exchange reserves. However, even central-bank intervention cannot fully shield the rupee.

India imports large quantities of oil, and oil prices have risen because of Middle Eastern tensions.

Higher oil prices combined with a stronger dollar create a painful double blow.

Australian Dollar

The Australian dollar fell 0.7% in the previous session.

Australia is heavily reliant on exports of iron ore, coal, and natural gas. Commodity prices are typically denominated in U.S. dollars, meaning a stronger dollar often places downward pressure on commodity markets.

Lower commodity prices reduce export revenues, which in turn weaken the Australian dollar.

Thursday brought stabilization, but the broader trend remains under pressure.

Chinese Yuan

The yuan slipped 0.1% in onshore trading.

The move was modest but symbolic.

China tightly manages its currency, yet even Beijing is finding it increasingly difficult to prevent depreciation against a surging dollar.

China’s post-pandemic recovery remains uneven. Foreign investment has slowed, capital outflows persist, and economic momentum remains weaker than policymakers would like.

All of these factors weigh on the yuan.

Singapore Dollar

The Singapore dollar was the most stable currency among its regional peers.

Singapore’s monetary policy framework focuses on exchange-rate management rather than interest rates. The Monetary Authority of Singapore actively smooths volatility, preventing excessive swings against the dollar.

So far, that strategy has been working.

Looking Ahead: Friday’s Payroll Report

All eyes are now on Friday’s U.S. nonfarm payrolls report.

Few economic indicators carry more weight in global financial markets.

The report measures how many jobs were created outside the agricultural sector and influences everything from the dollar and bond yields to stock markets and even cryptocurrencies.

If payroll growth comes in strong—say above 200,000 jobs—the dollar will likely strengthen further.

Asian currencies could resume their decline.

The yen could break through 160.

The won could lose another percentage point.

The rupee might approach new record lows.

If payrolls disappoint—below 150,000 jobs—the opposite could occur.

The dollar would likely weaken.

Asian currencies would gain some breathing room.

The yen could pull back from 160, reducing immediate intervention risks.

The most interesting outcome may be somewhere in the middle, around 150,000–180,000 jobs.

In that case, markets would receive no decisive signal. The dollar could remain range-bound, while Asian currencies continue balancing precariously between stability and renewed weakness.

That scenario may actually be the most likely.

The U.S. economy is slowing—but not collapsing.

The labor market is cooling—but not freezing.

Inflation is easing—but not surrendering.

What Should Investors Expect?

Asia’s currency markets currently resemble someone walking across thin ice.

The ice is cracking—but not breaking.

The dollar is pushing—but not overwhelming everything in its path.

Middle Eastern conflicts continue smoldering—but have not exploded into a wider regional war.

Federal Reserve rates remain high—but have not choked off economic growth.

This uneasy equilibrium could persist for quite some time.

Or it could unravel at any moment.

For investors holding assets denominated in Asian currencies, diversification remains the most sensible strategy. Avoid concentrating exposure in a single currency. Maintain a mix of dollars, gold, and equities that can generate returns regardless of exchange-rate movements.

For companies operating across Asia and earning revenues in local currencies, now may be an ideal time to consider hedging foreign-exchange risk. The dollar could strengthen further, and profits converted into dollars may shrink rapidly.

For ordinary savers watching their local currencies weaken against the dollar, the advice is simple:

Do not panic.

Currencies fluctuate. The dollar has been strong before. And history shows that forces eventually emerge to restore balance.

Thursday offered a brief respite.

Friday may bring another storm.

Or it may not.

Markets dislike certainty.

That is what makes them frightening.

And that is what makes them fascinating.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.