Three Reasons Why HSBC Expects Decisive Action from the Bank of Japan

For decades, the Bank of Japan has been synonymous with monetary easing. While the Federal Reserve, the European Central Bank, and the Bank of England raised interest rates, fought inflation, and adopted more hawkish rhetoric, Tokyo remained an island of cheap money in a world of expensive capital. But that island now appears to be sinking.

HSBC has revised its forecast and now expects the Japanese central bank to raise rates twice this year. The first hike is projected for June rather than July, as previously anticipated. The second is expected in December. By year-end, the policy rate is forecast to reach 1.25%.

For a country that has spent decades with zero or even negative interest rates, this is close to a revolution. HSBC economist Frederik Neumann outlined three factors behind the revised outlook, and each deserves close attention.

Factor One: Changes on the Policy Board

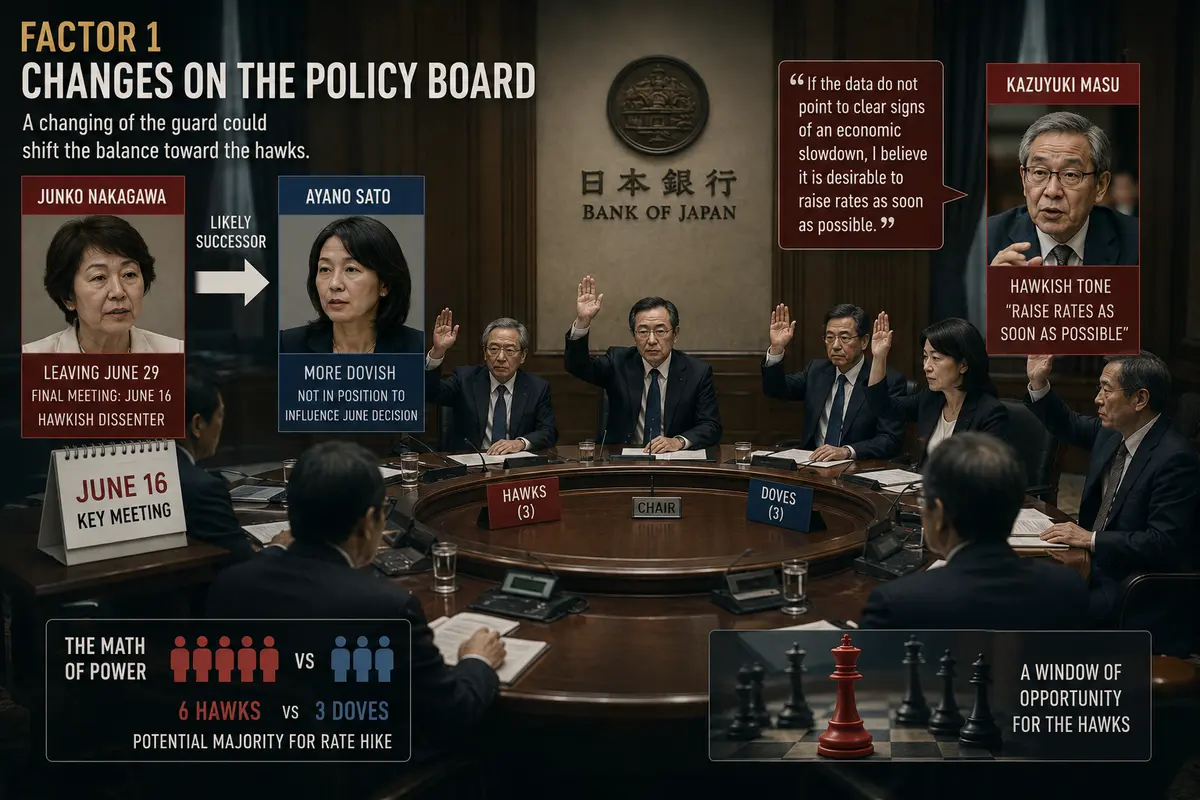

Central banks are not abstract institutions run by algorithms. They are run by people—specific men and women who sit around a table, debate, vote, and make decisions. The fate of entire economies can depend on who occupies those seats. At the Bank of Japan, a changing of the guard is underway that could shift the balance of power toward the hawks.

Junko Nakagawa, a member of the Policy Board, will leave her post on June 29. Her final meeting will take place on June 16—the very meeting at which HSBC believes a rate hike could be approved. Nakagawa was one of three dissenting members who voted in favor of a rate increase at the previous meeting. In other words, she was already part of the hawkish camp. Yet her departure could paradoxically strengthen that camp’s influence.

Her likely successor is Ayano Sato, whom HSBC characterizes as more inclined toward accommodative monetary policy. This means that Nakagawa, aware that her term is ending, may wish to leave her mark on history by supporting a rate hike at her final meeting. Her successor, being more dovish, would not yet be in a position to influence the June decision. This is a classic “lame duck” effect, where an outgoing policymaker enjoys greater freedom of action unconstrained by future career considerations.

But the story does not end with Nakagawa. Another board member, Kazuyuki Masu, has adopted an increasingly hawkish tone in recent weeks. His remarks sounded almost like an ultimatum:

“If the data do not point to clear signs of an economic slowdown, I believe it is desirable to raise rates as soon as possible.”

This is more than hawkish rhetoric. It is a direct signal to his colleagues: he is prepared to vote for higher rates.

If three hawks align with the three recent dissenters, the result would be six votes against three—a clear majority in favor of tightening. It is simple arithmetic that could alter Japanese monetary policy faster than many expect. HSBC has analyzed this balance of power and concluded that the June meeting represents a window of opportunity for the hawks—and they are likely to seize it.

Factor Two: Inflation That Refuses to Fade

HSBC’s second argument is based on the data. Core consumer inflation, excluding institutional factors, has risen to 2.8% year-over-year. That is well above the Bank of Japan’s 2% target.

Japan, which spent decades battling deflation, is now facing the opposite challenge: inflation has not only arrived—it has become entrenched.

An inflation rate of 2.8% is not something policymakers can simply ignore. This is not a temporary spike caused by expensive oil. It is persistent price pressure that is spreading through consumer spending and changing behavior. Japanese consumers, long accustomed to stable prices, are seeing higher costs for food, transportation, and utilities. As a result, they are demanding higher wages. Rising wages, in turn, reinforce the inflation cycle.

At the same time, economic growth is being supported by AI-related exports. Japanese semiconductor and equipment manufacturers are experiencing a boom. Companies such as Renesas, Rohm, and Tokyo Electron are benefiting from strong demand. Meanwhile, government support measures designed to cushion households from higher energy prices are adding further stimulus to the economy.

Together, these factors create an environment in which inflation is unlikely to slow on its own. It must be restrained—and the primary tool for doing so is higher interest rates.

Factor Three: A Yen That Cannot Wait

The third factor highlighted by HSBC is the Japanese yen.

The currency remains under persistent pressure. USD/JPY continues to hover near the 160 level, which triggered large-scale currency interventions earlier this year. Tokyo spent tens of billions of dollars supporting the yen. The intervention worked temporarily, but the underlying problem remains unresolved.

The interest-rate gap between Japan and other G10 economies remains enormous. The Bank of Japan maintains a policy rate that leaves the yen at a significant disadvantage.

HSBC warns that keeping rates too low for too long risks renewed yen depreciation. A weak yen is not merely an abstract macroeconomic indicator—it is a direct threat to Japan’s economy. More expensive imports of energy and food fuel inflation. Companies dependent on foreign supplies face higher costs. Consumers lose purchasing power.

Currency intervention can smooth volatility, but it cannot reverse the trend. Only a reduction in the interest-rate differential can accomplish that.

If the Bank of Japan raises rates in June and again in December, the gap with other G10 economies will begin to narrow. According to HSBC, this would “at the very least help stabilize the yen.”

But yen stabilization is not an end in itself. It is a way to contain imported inflation, support consumers, and provide the economy with greater flexibility. Higher interest rates are a remedy that addresses several problems at once.

The Market Agrees

Overnight index swap (OIS) markets—where traders bet on future interest-rate moves—are already pricing in nearly two 25-basis-point rate hikes this year.

That means HSBC’s revised forecast is neither radical nor surprising. The market has independently arrived at a similar conclusion.

Two quarter-point increases may seem modest compared with the aggressive tightening cycles carried out by the Federal Reserve or the ECB. But for Japan, they would represent a tectonic shift. After decades of near-zero rates, every move higher is significant. Two hikes in a single year is almost a sprint.

With its latest note, HSBC is effectively confirming what markets have already begun to suspect: the Bank of Japan can no longer afford to stand still. Inflation is persistent, the yen remains weak, and personnel changes have opened a window of opportunity for the hawks.

The June meeting will be the moment of truth. If HSBC is right, June 16 may be remembered as the day Japan finally said goodbye to the era of cheap money.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.