Industry Loses Momentum

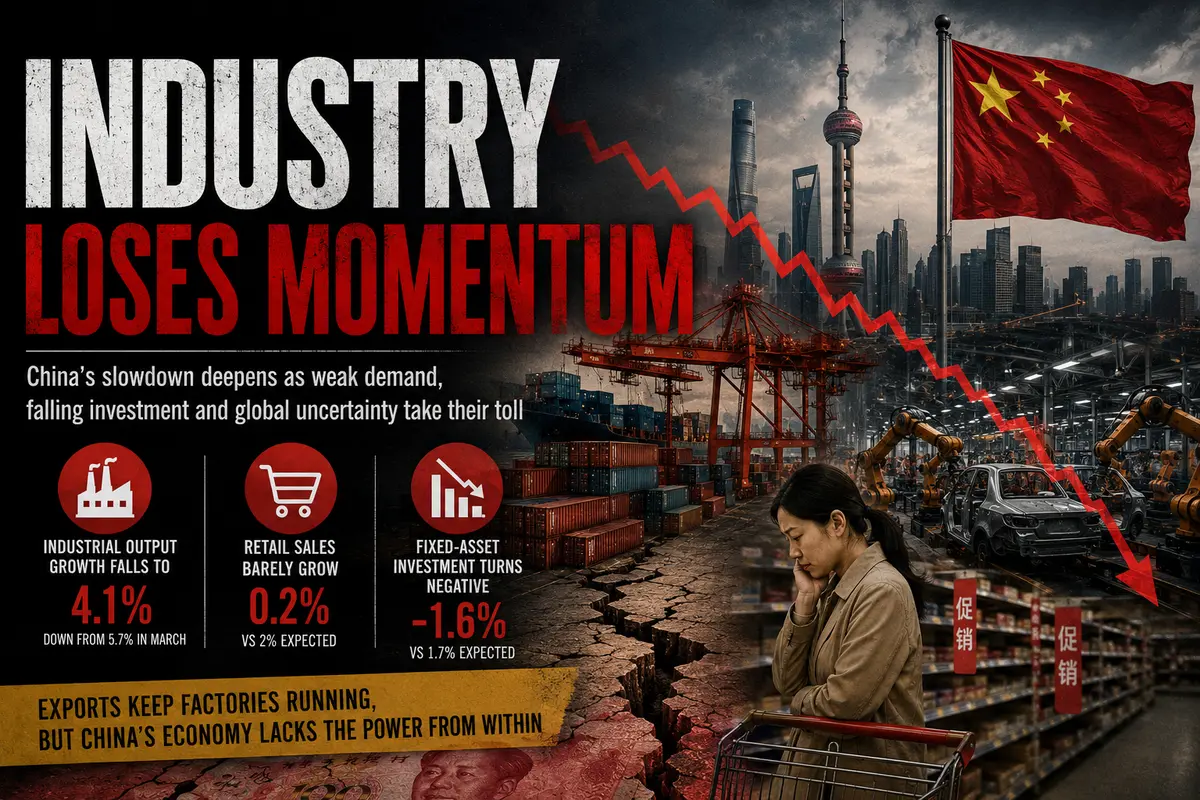

When China’s April industrial production figures were released on Monday morning, analysts had to quietly put away their forecasts. Growth came in at 4.1% year-over-year. That is not just below March’s 5.7% — it is dramatically below the consensus forecast, which had expected an acceleration to 6%. A gap of nearly two percentage points between expectations and reality is not a statistical error; it is a full-scale miss that forces a reassessment of the picture of the Chinese economy.

What is behind this slowdown? Analysts at ING offered a fairly accurate assessment in their review: industrial activity is being supported by strong external demand, while virtually all indicators of domestic demand remain weak. In other words, Chinese factories are still operating because Americans and Europeans continue buying Chinese goods, but Chinese consumers themselves have largely stopped spending. Exports have been masking the weakness of the domestic market, and the April data ripped that mask away.

This model — relying on exports while domestic consumption remains weak — is not new for China. But in the past, it worked: rapid global economic growth pulled Chinese factories forward, and those factories, in turn, created jobs and incomes that gradually supported domestic demand. Now, however, the global economy itself is balancing on the edge, trade wars have not disappeared, and geopolitical tensions surrounding Iran have pushed energy prices higher, hurting Chinese manufacturers that import oil and gas. In such an environment, relying solely on exports is becoming increasingly risky.

Retail Sales: A Consumer Unwilling to SpendIf industrial production is at least still growing, albeit slowly, retail sales have practically stalled. Growth of just 0.2% year-over-year is a statistical figure barely distinguishable from zero. For comparison, analysts had expected 2%, while March recorded 1.7%. A drop from nearly 2% to nearly zero in...