Industry Loses Momentum

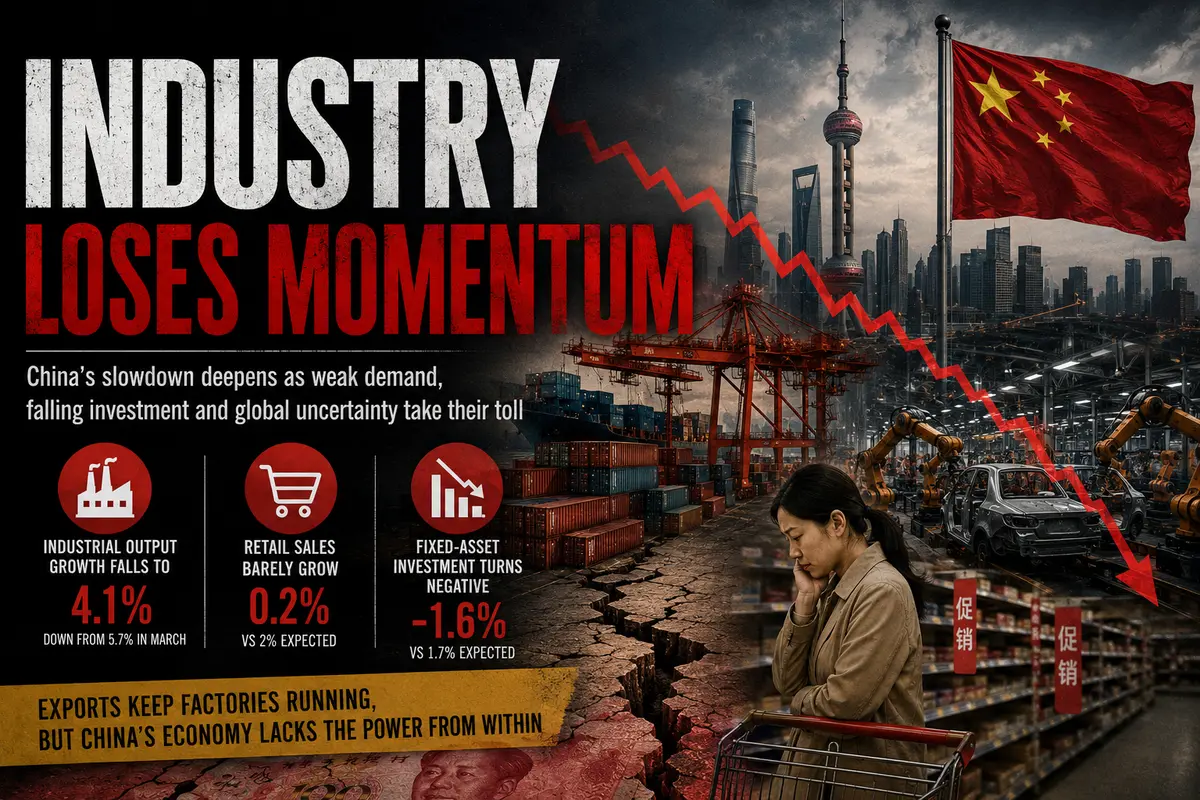

When China’s April industrial production figures were released on Monday morning, analysts had to quietly put away their forecasts. Growth came in at 4.1% year-over-year. That is not just below March’s 5.7% — it is dramatically below the consensus forecast, which had expected an acceleration to 6%. A gap of nearly two percentage points between expectations and reality is not a statistical error; it is a full-scale miss that forces a reassessment of the picture of the Chinese economy.

What is behind this slowdown? Analysts at ING offered a fairly accurate assessment in their review: industrial activity is being supported by strong external demand, while virtually all indicators of domestic demand remain weak. In other words, Chinese factories are still operating because Americans and Europeans continue buying Chinese goods, but Chinese consumers themselves have largely stopped spending. Exports have been masking the weakness of the domestic market, and the April data ripped that mask away.

This model — relying on exports while domestic consumption remains weak — is not new for China. But in the past, it worked: rapid global economic growth pulled Chinese factories forward, and those factories, in turn, created jobs and incomes that gradually supported domestic demand. Now, however, the global economy itself is balancing on the edge, trade wars have not disappeared, and geopolitical tensions surrounding Iran have pushed energy prices higher, hurting Chinese manufacturers that import oil and gas. In such an environment, relying solely on exports is becoming increasingly risky.

Retail Sales: A Consumer Unwilling to Spend

If industrial production is at least still growing, albeit slowly, retail sales have practically stalled. Growth of just 0.2% year-over-year is a statistical figure barely distinguishable from zero. For comparison, analysts had expected 2%, while March recorded 1.7%. A drop from nearly 2% to nearly zero in a single month is a warning signal that cannot be ignored.

The Chinese consumer, who only a few years ago was considered the world economy’s greatest hope, is now sitting tightly on their wallet and reluctant to open it. The reasons are well known and form a vicious cycle. The real estate market, where Chinese households invested the lion’s share of their savings, continues to decline. When the value of a household’s primary asset falls, people feel poorer — even if their current income has not changed. This is known as the wealth effect, and in China it is now working in reverse, compressing consumer spending like a tightening spring.

Add to that sluggish wage growth. Companies facing weakening demand and rising uncertainty are in no rush to raise salaries. On the contrary, many are cutting bonuses, freezing hiring, and shifting employees to part-time work. When incomes stagnate and savings shrink, consumers switch into survival mode: buying only essentials, postponing major purchases, and generally behaving as though tomorrow offers little reason for optimism.

Deflationary pressure adds yet another layer of problems. When prices stagnate or decline, consumers delay purchases in anticipation of even lower prices later. Why buy today what may cost less tomorrow? This psychology, familiar to Japan from its lost decades, is now taking root in China as well. And uprooting it will be far more difficult than launching another infrastructure project.

Fixed-Asset Investment: Business No Longer Believes in Growth

The third blow from Monday’s data came from fixed-asset investment — a key indicator of whether businesses are willing to spend money on expanding production, purchasing equipment, and construction. Here the numbers actually turned negative: investment fell 1.6% year-over-year, while analysts had expected growth of 1.7%.

This is perhaps the most alarming signal of all. Consumers may be cautious — that is their right. But when businesses refuse to invest, it means entrepreneurs see little prospect for growth. Why build a new factory if existing capacity is underutilized? Why purchase new equipment if demand for products is not increasing? Why hire additional workers if the current workforce can handle existing volumes?

The decline in fixed-asset investment is effectively a vote by businesses against a near-term recovery. Entrepreneurs, who see the real economy from the inside — monitoring inventories, orders, and customer payments firsthand — are voting with their wallets, and they are voting against optimism. This is not the picture China’s leadership wants to see.

The Beijing Summit: Talks Without Breakthroughs

The weak economic data arrived just days after talks between Donald Trump and Xi Jinping concluded in Beijing. The summit had raised high hopes — if not for a full resolution of trade disputes, then at least for some easing of tensions. The leaders agreed to continue economic dialogue, discussed potential tariff reductions, and explored expanding American agricultural exports.

But the summit produced no meaningful breakthroughs. The two sides talked, exchanged pleasantries, reaffirmed their intention to continue negotiations — and then walked away. For the Chinese economy, which desperately needs lower trade barriers and reduced uncertainty, this offers little comfort. Tariffs remain in place, technological restrictions are tightening, and geopolitical disagreements remain unresolved.

Moreover, the conflict surrounding Iran — where China could potentially play the role of mediator — still shows no sign of resolution. That means oil prices are likely to remain elevated, inflationary pressures will persist, and global uncertainty will continue weighing on investment decisions worldwide, including in China.

Beijing’s Promises: Will They Help?

Chinese officials have recently been generous with promises. Additional support measures to stimulate domestic demand, efforts to stabilize the property sector, commitments to maintaining economic growth — all of these messages are coming from Beijing with impressive regularity. But markets have already learned to distinguish rhetoric from concrete action.

The problem is that the proposed measures often prove too targeted and insufficient. Lower mortgage rates are helpful, but they do little if people are afraid to take on debt because of job insecurity. Subsidies for car purchases are positive, but they cannot offset collapsing property prices that are eroding household savings. Infrastructure projects — China’s traditional remedy — create jobs, but they do not solve the structural problems weighing on consumer demand.

Analysts point to a persistent set of pressures still weighing on consumers: weak wage growth, deflationary pressure, and the real estate crisis. These are systemic problems that cannot be solved with a single stimulus package. They require a long-term, consistent policy aimed at redistributing income from the state and large corporations to households, strengthening the social safety net, and restoring confidence in the future.

External Demand: A Double-Edged Sword

For now, Chinese industry is surviving on external demand. That is positive — exports bring in foreign currency, keep factories running, and support employment. But it is also dangerous: dependence on demand from the United States and Europe makes China vulnerable to foreign economic problems and political decisions.

If the American economy begins to slow — and the risks are rising amid high interest rates and geopolitical instability — Chinese exports will suffer a blow that the domestic market will be unable to offset. If trade negotiations deteriorate and tariffs rise further, the export engine will begin to sputter. And if conflict in the Middle East continues driving oil prices higher, Chinese manufacturers will face rising costs that eat away at their competitive advantage.

The April data are not a catastrophe. Industry is still growing, and retail sales are not collapsing — merely stagnating. But this is the picture of an economy that has lost its internal momentum and is moving forward largely by inertia, powered by external winds. And winds, as we know, have a tendency to change. When they do, China will need entirely different sources of growth — the very domestic drivers it has so far struggled unsuccessfully to ignite. April showed that success on that front remains far away.

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.