Sterling Gains, but Its Position Looks Fragile

A Small Green Ray Through the Clouds

Thursday brought a modest sense of relief to holders of British pounds and euros. After several days in which the U.S. dollar bulldozed its way through virtually every major currency, the market finally paused. Sterling gained 0.27% against the dollar, reaching 1.3459. The euro performed slightly better, rising 0.35% to 1.1640.

These are modest, almost symbolic moves. Yet after the previous day’s decline, even such gains felt like a welcome gift.

Still, don’t be fooled by the green numbers on the screen. The pound and the euro remain on extremely shaky ground. They resemble a person walking across thin ice—every next step could be the last. The fundamental drivers behind these currencies have not changed. The dollar remains strong. Geopolitical risks remain severe. And economic data from Europe and the UK continue to disappoint.

On Thursday, the dollar merely took a breather. Investors paused ahead of Friday’s key event—the U.S. nonfarm payrolls report. This release could either reinforce the dollar’s recent momentum or call it into question. Few traders are willing to establish major positions ahead of such uncertainty. As a result, the dollar stood still while the pound and euro managed a modest rebound.

But let’s take a closer look. Why does sterling remain so vulnerable? Why is the euro struggling to strengthen despite its gains? And what lies ahead for these currencies after the U.S. employment data is released?

Sterling: Recovering After a Blow

Let’s begin with the pound. Thursday’s modest rise followed a sharp decline the previous day.

On Wednesday, sterling fell heavily after disappointing UK services-sector PMI data.

The figures were alarming. For the first time in more than a year, the index dropped below the psychologically important 50-point threshold. A reading above 50 signals expansion; below 50 indicates contraction. The services sector—which accounts for the lion’s share of Britain’s economy—slipped into recession territory. The composite PMI, combining services and manufacturing, also moved into negative territory.

For sterling, this was a cold shower.

The UK economy was already walking a tightrope. Inflation, while lower than before, remains elevated. Interest rates are at multi-year highs. Consumers are cutting spending. Businesses are scaling back investment. And now the services sector—the traditional backbone of the British economy—is beginning to wobble as well.

Persistent cost pressures add another layer of difficulty. Companies continue to report rising expenses for raw materials, energy, and logistics. The conflict with Iran and the resulting surge in oil prices have hit Britain particularly hard, given its dependence on imported energy. Costs are rising while profit margins are shrinking.

This leaves the Bank of England facing an uncomfortable choice: continue raising rates to fight inflation or leave them unchanged to avoid choking economic growth.

Markets increasingly appear to favor the latter scenario. Traders are no longer expecting aggressive monetary tightening from the Bank of England. Instead, they are beginning to price in the possibility of rate cuts later in the year.

For sterling, that is bad news. Lower rates generally make a currency less attractive to foreign investors.

As a result, the recovery of GBP/USD to 1.3459 looks highly fragile. There are no fresh domestic catalysts capable of pushing the pound significantly higher. There are no optimistic forecasts for the UK economy. There is little confidence that the Bank of England can dramatically improve the situation.

What remains is merely a temporary pause before Friday’s storm.

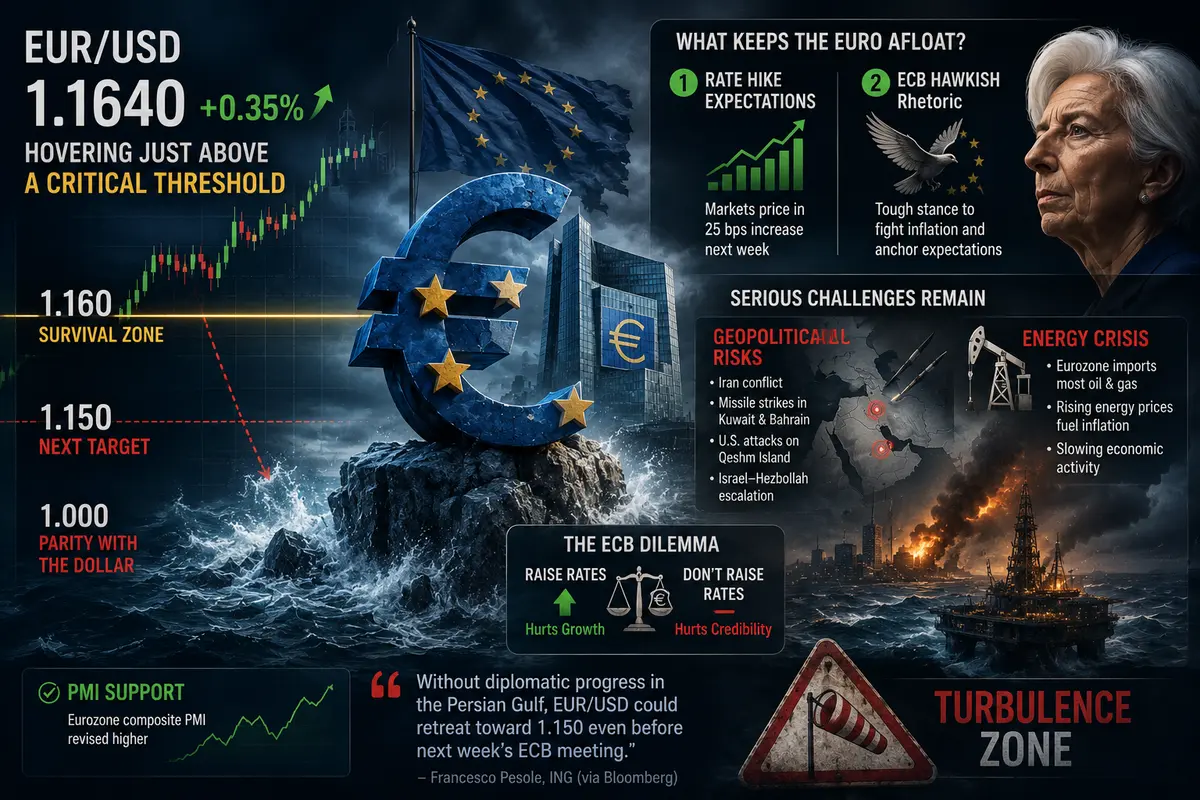

Euro: Hovering Just Above a Critical Threshold

The euro is faring only slightly better than sterling.

EUR/USD rose 0.35% to 1.1640, putting it just above the critical 1.160 level that ING analysts describe as a “survival zone.” If the euro falls below 1.160, the next likely target is 1.150—and from there, parity with the dollar begins to enter the conversation once again.

What is keeping the euro afloat?

Two factors.

The first is expectations that the European Central Bank will raise interest rates at next week’s meeting. Markets are pricing in a 25-basis-point increase, which would mark the eighth hike in just over a year.

The second is the ECB’s hawkish rhetoric. ING analysts expect policymakers to maintain a tough stance in order to preserve expectations for further tightening and keep inflation expectations under control. Inflation in the eurozone has slowed, but it remains roughly double the ECB’s target.

The central bank cannot afford to relax.

Yet serious challenges remain.

The biggest is geopolitics. The conflict involving Iran, missile strikes in Kuwait and Bahrain, U.S. attacks on Qeshm Island, and escalating tensions between Israel and Hezbollah have all undermined confidence in risk-sensitive assets.

Unfortunately for the euro, it is still widely viewed as a risk currency—especially when compared with the U.S. dollar.

Energy is another major concern.

The eurozone imports most of its oil and gas. Rising energy prices are fueling inflation while simultaneously slowing economic activity. This combination of inflation and stagnation—stagflation—is a central bank’s worst nightmare.

The ECB faces the same dilemma as the Bank of England: raising rates hurts growth, while failing to raise rates hurts inflation-fighting credibility.

Wednesday’s upward revision of eurozone composite PMI data provided some support for the euro, but the impact was limited. Market sentiment remains dominated by energy prices and global risk appetite—both of which currently work against the single currency.

Francesco Pesole of ING, quoted by Bloomberg, warns that without diplomatic progress in the Persian Gulf, EUR/USD could retreat toward 1.150 even before next week’s ECB meeting.

This is less a forecast than a warning.

The euro remains firmly in a turbulence zone.

Dollar: The Calm Before the Storm

While the pound and euro enjoy a modest respite, the dollar is preparing for the week’s defining event.

The U.S. Dollar Index remains close to two-month highs. ING analysts believe the 100 level is well within reach if the Middle East situation fails to show meaningful progress toward de-escalation.

What’s driving the dollar’s strength?

First, economic data.

Wednesday’s ADP employment report showed that U.S. private employers created more jobs than expected. The ISM services PMI increased, while its price component surged to its highest level in nearly four years.

Despite elevated interest rates, the U.S. economy continues to demonstrate remarkable resilience.

Second, the Federal Reserve’s Beige Book.

The report pointed to stable employment prospects across regions. Inflationary pressures remain present, and concerns about slowing growth persist, but employers continue to hire workers.

A strong labor market gives the Fed little reason to rush into rate cuts.

Third, geopolitics.

The dollar remains the world’s premier safe-haven currency.

When global conflict escalates, investors tend to sell risk assets and buy dollars. Headlines involving Iran, Israel, Hezbollah, and the Strait of Hormuz continue to drive capital toward the United States.

Thursday’s pause in the dollar was largely due to a light U.S. economic calendar. The only notable releases were Challenger job-cut announcements and weekly unemployment claims data.

Neither report delivered any major surprises.

As a result, investors remained on the sidelines, waiting for Friday’s nonfarm payrolls report.

The outcome will likely determine the next move not only for the dollar, but also for sterling and the euro.

Nonfarm Payrolls: Three Possible Scenarios

Friday’s U.S. employment report is the week’s most important event for currency markets.

The consensus forecast calls for roughly 180,000 new jobs in May.

As always, surprises are possible.

Scenario 1: Dollar-Negative

If nonfarm payrolls come in significantly below expectations—around 120,000 to 130,000 or lower—it would suggest that the U.S. economy is slowing more rapidly than anticipated.

The Federal Reserve could begin signaling future rate cuts sooner.

The dollar would likely weaken sharply.

Sterling and the euro could rally strongly, with GBP/USD potentially moving toward 1.3600 and EUR/USD toward 1.1800.

Scenario 2: Dollar-Positive

If payroll growth significantly exceeds expectations—220,000 to 250,000 or more—it would reinforce the view that the labor market remains overheated and inflation pressures remain persistent.

The Fed would have little reason to cut rates and might even need to consider additional tightening.

The dollar would strengthen further.

GBP/USD could fall below 1.3300, while EUR/USD could break beneath 1.1500.

Scenario 3: Neutral

If payroll growth lands between 160,000 and 190,000, markets would receive no clear signal.

The dollar would remain strong but gain no fresh momentum.

Sterling and the euro would likely continue trading within their current ranges:

-

GBP/USD: 1.3400–1.3500

-

EUR/USD: 1.1600–1.1700

Most analysts view this third scenario as the most likely outcome.

The U.S. economy appears to be slowing, but not collapsing. The labor market is cooling, but not freezing.

Still, in today’s environment, “most likely” is far from “certain.”

That uncertainty is exactly why investors remain cautious.

ECB and Bank of England: Challenges Ahead

While attention remains focused on the Federal Reserve, both the European Central Bank and the Bank of England are preparing for upcoming policy meetings.

The ECB meets next week.

The Bank of England follows two weeks later.

Markets broadly expect both institutions to raise rates by 25 basis points.

Yet rate hikes are a double-edged sword.

They may support currencies in the short term, but they also weigh on already fragile economies.

The upward revision of eurozone PMI data offers some hope.

The UK’s PMI collapse below 50 largely destroys it.

Europe and Britain are currently moving through different phases of the economic cycle, complicating the task for policymakers.

ING analysts expect the ECB to maintain a hawkish tone next week, signaling that further tightening remains possible even after a widely expected 25-basis-point hike.

That could support the euro—but probably only temporarily.

Without diplomatic progress in the Middle East, geopolitical risks are likely to outweigh anything the ECB says.

The Bank of England, by contrast, may adopt a more dovish stance.

Weak PMI data provide a strong argument for caution.

If policymakers hint that the tightening cycle is nearing its end, sterling could come under renewed pressure—even if rates are increased at the meeting itself.

European currencies are therefore caught between multiple competing forces: the Fed, the ECB, the Bank of England, geopolitical tensions, and oil prices.

At the moment, the net effect still points downward.

Geopolitics: The Dominant Driver

We’ve spent a great deal of time discussing economics, interest rates, and PMI data.

But the primary driver of currency markets right now is not economics.

It is war.

The United States and Iran remain locked in an escalating confrontation. Missiles are flying. Military strikes continue. Diplomatic negotiations have stalled.

Each new confrontation reinforces defensive positioning across global markets.

And defensive positioning typically means buying dollars and selling risk-sensitive currencies, including the pound and the euro.

The key levels highlighted by ING—EUR/USD at 1.160, USD/JPY at 160, and USD/CAD at 1.390—are more than technical markers.

They are psychological battlegrounds.

A break below EUR/USD 1.160 would signal that bears are taking control. The next target would be 1.150. If that level also gives way, discussions about euro-dollar parity (1.000) would become increasingly serious.

Similarly, a move in USD/JPY beyond 160 could force Japanese authorities to intervene again, as they did in April.

And if USD/CAD rises beyond 1.390, it would suggest that even commodity-linked currencies are failing to benefit from elevated oil prices.

That would be a troubling signal for the broader currency market.

What to Watch on Friday

Everything now hinges on Friday’s U.S. nonfarm payrolls report.

Weak employment growth would support sterling and the euro.

Strong employment growth would favor the dollar and pressure both European currencies.

A result near expectations would likely leave markets range-bound.

But regardless of the outcome, geopolitics is not going away.

The United States and Iran will not resolve their differences overnight.

Israel and Hezbollah are unlikely to lay down their arms tomorrow.

Oil prices are likely to remain elevated.

As a result, any rally in sterling or the euro remains vulnerable.

Any reversal remains possible.

Markets are likely to stay nervous, volatile, and unpredictable.

For investors holding pounds or euros, one approach may be to lock in profits and wait out the uncertainty in cash. Those with a higher appetite for risk may prefer to position for further dollar strength, as most fundamental factors currently support that view.

And the pound and euro?

They will continue trying to recover lost ground.

But their foundations remain fragile.

Like buildings constructed on marshland—impressive on the surface, yet vulnerable to collapse when the first earthquake arrives.

And judging by the current landscape, that earthquake may not be far away.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.