Japan’s Debt on the Brink: How an Oil Checkmate Brought the Bond Market to Its Knees

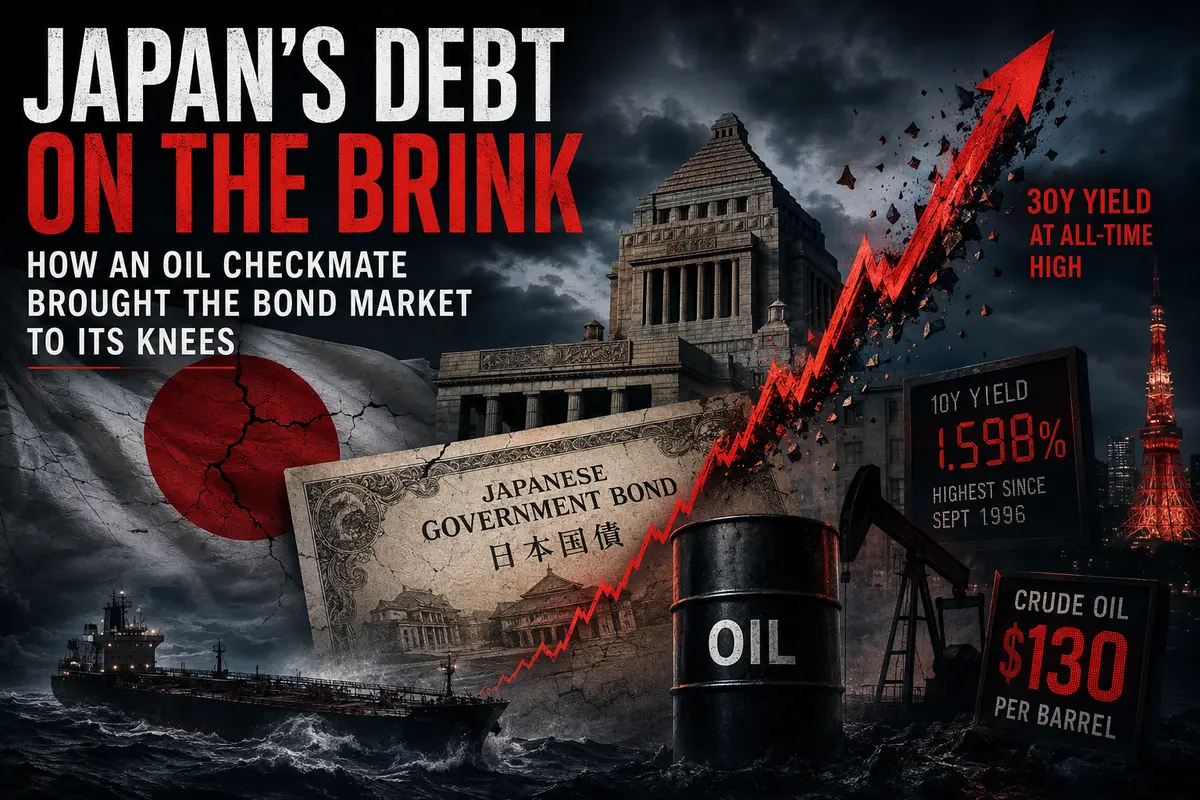

The global bond selloff, which two weeks ago looked like a chaotic stampede for the exits, has eased somewhat in recent days. But that does not mean the fire has been extinguished. Rather, the flames have spread elsewhere, and now the fiercest blaze is raging in a market that for decades was considered a bastion of stability. Japanese government bonds are facing a moment of truth. Yields on ten-year bonds have surged to levels unseen since September 1996 — an era when Bill Clinton was president of the United States and the word “smartphone” did not yet exist. Thirty-year bond yields have reached an all-time record high. And this is happening not just anywhere, but in Japan — a country that spent decades battling deflation and whose bonds seemed like a permanent refuge of calm. Now that refuge is beginning to crack.

The Reflation Trade: How a Longstanding Bet Ran Out of Steam

In recent years, Japan’s debt market has lived in a reality unlike that of other developed nations. While the Federal Reserve, the ECB, and the Bank of England fought inflation by raising interest rates, the Bank of Japan stubbornly maintained an ultra-loose monetary policy. This gave rise to the so-called “reflation trade” — investors betting that Japan would finally escape its deflationary spiral, inflation would begin to rise, and the central bank would eventually be forced to normalize policy. It was a profitable trade: Japanese bonds fell in price, yields crept higher, and traders made money.

But now, as Thomas Mathews of Capital Economics warns, that trade is nearing a critical point. “Most of the recent rise in yields has been benign,” he wrote in a recent note. In other words, the market had gradually priced in normalization, and that was considered a healthy process. But now, according to the analyst, the reflation trade is either already fully priced in or very close to reaching that point. And that means further increases in yields are no longer benign. They become malignant. What was once a reflection of positive expectations begins to look like a symptom of a genuine crisis.

When yields rise too far and too fast, the story stops being about a return to normality. It becomes a story about the market losing faith in the government’s ability to manage its debt and in the central bank’s ability to maintain control. Japan, with its colossal public debt exceeding 260 percent of GDP, is especially vulnerable. Every percentage point increase in yields adds trillions of yen to debt-servicing costs, squeezing fiscal space that is already under severe strain.

The Oil Shock: How the Strait of Hormuz Reached Tokyo

The roots of Japan’s current problems lie not in Tokyo or even Osaka. They lie in the Strait of Hormuz, where American destroyers and Iranian patrol boats continue their dangerous game. Japan is almost entirely dependent on imported energy. When oil surges to $130 a barrel, the Japanese economy suffers a devastating blow. Inflation rises — and it is cost-push inflation, the most unpleasant kind, because it is beyond the central bank’s direct control.

The government tried to soften the impact by introducing massive subsidies for wholesale fuel distributors and capping gas prices. It worked — headline annual inflation slowed in April to a four-year low. But there is another side to the coin. Subsidies cost money, and a great deal of it. According to Mathews, oil prices remaining around $130 through the end of the year would cost the government roughly 2 percent of GDP. That creates a hole in the budget that will have to be filled either with new borrowing or through supplementary spending packages. Prime Minister Takaichi has already hinted at such a possibility.

And this is where the circle closes. The market sees rising fiscal spending, sees the need for additional borrowing, sees the enormous public debt burden — and starts demanding a risk premium. Long-term bond yields continue climbing, with the move especially pronounced at the ultra-long end of the curve. This is the “bear steepening” of the JGB yield curve that Mathews describes — a situation in which long-term yields rise faster than short-term ones. The market is effectively telling the government: we are no longer sure that, ten, twenty, or thirty years from now, you will be able to service this debt without major problems. And investors now want to be paid extra for taking that risk.

The Bank of Japan Between a Rock and a Hard Place

At the center of this storm stands the Bank of Japan and its governor, Kazuo Ueda. The situation he faces resembles a classic trap. On the one hand, rising inflation calls for higher interest rates. The market has already priced in such hikes — that is precisely why yields are climbing. On the other hand, the Japanese economy is too fragile to withstand aggressive tightening. Decades of ultra-loose policy have made it dependent on cheap money the way a patient becomes dependent on medication.

At recent G7 meetings, Ueda noted that the Bank is closely monitoring the market. That is a standard phrase, but in the current context it sounds almost like a warning. The Bank of Japan, perhaps the most cautious central bank in the world, is now being forced toward decisions it has spent years trying to avoid. Either it raises rates, risking an economic downturn and a real estate crisis. Or it accelerates balance-sheet operations — reducing its enormous bond holdings, which would also push yields higher. Or it does nothing and watches the market tighten the noose around Japan’s debt burden on its own.

Every option here is a choice between bad and worse. And the fact that Japan’s bond market is coming under “increasing pressure,” as Mathews puts it, is not a temporary difficulty. It is the beginning of a structural shift that could reshape Japanese finance for the next decade.

The Yen: Interventions Forgotten, Pressure Returns

While bonds burn, the yen continues its painful decline. Back in late April, Tokyo was widely believed by traders to have intervened in currency markets in an attempt to stop the weakening of the national currency. It worked — for a while. But now the yen is once again approaching the psychologically important level of 160 per dollar, and interventions, no matter how massive, no longer appear effective.

A weak yen is yet another source of inflationary pressure. An expensive dollar makes imported goods — including energy and food — even more costly. The result is a vicious cycle: a weak yen fuels inflation, inflation leads markets to expect higher rates, expectations of higher rates drive bond yields upward, rising yields increase debt-servicing costs, and fiscal stress once again weighs on the yen. Breaking this cycle would require decisive action — something the Bank of Japan still seems unwilling to take.

The Global Context: Japan Is Not Alone, but It Is Unique

Japan’s bond selloff is not the most severe among major economies. Yields in the United Kingdom have risen more sharply, while those in the United States and France have seen comparable increases. But Japan’s case stands out because of the nature of the move itself. The “bear steepening” described by Mathews is a distinctly Japanese phenomenon, reflecting a unique combination of factors: colossal public debt, near-total dependence on imported energy, and a central bank cornered by decades of ultra-loose policy.

Other countries can raise rates without immediately risking fiscal collapse. The United States has a large debt burden, but also a strong and diversified economy. Britain has its own currency and room to maneuver. France has the backing of European institutions. Japan stands apart. Its debt burden is so enormous relative to the size of its economy that even modest increases in yields create pressures comparable to a full-blown sovereign debt crisis elsewhere.

Traders and analysts are now watching the Japanese bond market with the same tension that seismologists watch earthquake readings before a volcanic eruption. The critical point Mathews warns about may already have been reached. Or perhaps we are only approaching it. Either way, Japan has become the part of the global financial system where tensions accumulated over decades are now searching for an outlet. And when they finally find one, the consequences may be global.

Japanese bonds are held by Japanese banks, pension funds, and insurance companies. Their problems become problems for the entire Japanese financial system. And the problems of the Japanese financial system become problems for the whole world, which has long viewed Japan as an island of stability in the turbulent sea of global finance. That island no longer looks so stable. And whether it withstands the pressure may matter far beyond Tokyo.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.