Ciena Hits Pause: $2.5 Billion of Interest-Free Debt and a Delicate Dance with Shareholders

Silence in the Telecom Market: Why Everyone Is Watching Ciena

On Monday, while the financial world was focused on missiles in the Middle East and a falling Bitcoin, a Maryland-based company quietly executed a move that left many investors scratching their heads. Ciena Corporation, a global leader in high-speed optical networking, announced a $2.5 billion offering of convertible notes.

With a zero coupon.

That means no interest payments. Investors are lending the company nearly two and a half billion dollars and receiving no regular income in return. Zero.

Would you lend someone $2.5 billion at 0% interest?

Apparently, the answer is yes—if you’re a large institutional investor who sees this as more than just a loan. Demand was so strong that Ciena increased the offering from the originally planned $2 billion to $2.5 billion and added an option for initial purchasers to acquire another $375 million of notes within 13 days of issuance.

So what kind of financial magic is this? How can a company whose stock has fallen 25.6% over the past week raise billions of dollars at zero interest?

Let’s take a closer look.

The Deal: The Mechanics of an Almost Perfect Financial Crime

Let’s start with the numbers, because in finance, the devil is always in the details.

Ciena is issuing $2.5 billion of senior convertible notes due in September 2031.

The key word is convertible.

This means noteholders have the right to exchange their bonds for Ciena common stock at a predetermined conversion price.

What price?

$746.66 per share.

At the time of the announcement, Ciena stock was trading at $466.67 per share. That represents a 60% conversion premium.

Investors are willing to wait nearly five years—until the conversion period begins in June 2031—and bet that Ciena’s stock will rise by at least 60% from current levels.

If it does, they convert and profit.

If it doesn’t, they get their principal back.

And what does Ciena get?

$2.5 billion.

Essentially for free.

No interest.

For roughly seven and a half years.

Imagine a friend asking to borrow a million dollars and promising to return exactly the same amount seven years later—without paying you a cent in interest. You’d only agree if you believed there was significant upside elsewhere in the arrangement.

That’s exactly what’s happening here.

Institutional investors aren’t simply lending money.

They’re buying an option.

A chance—but not an obligation—to acquire Ciena shares at $746.66 if the market eventually values them much higher.

It’s a $2.5 billion wager on Ciena’s future.

Where the Money Is Going: Debt Repayment, Buybacks, and Hedging

The most interesting part isn’t how the company raised the money—it’s how it plans to spend it.

Ciena has laid out the allocation with surgical precision.

1. $100 Million for Convertible Note Hedges

The company will spend approximately $100 million on hedge transactions designed to offset potential shareholder dilution if the notes are eventually converted into stock.

In simple terms:

Ciena is insuring itself against its own success.

2. $140 Million for Share Repurchases

Another $140 million will be used to buy back roughly 300,000 shares at approximately $466.67 per share.

It’s a clever move.

The company is simultaneously creating the possibility of future share issuance through conversion while reducing the existing share count today.

This partially offsets dilution and sends a message to the market:

“We believe our stock is valuable.”

3. $1.14 Billion for Debt Reduction

The largest portion—$1.14 billion—will be used to repay outstanding term-loan debt.

Like any major corporation, Ciena carries debt.

After this transaction, it will carry less.

That means lower interest expense, a cleaner balance sheet, and potentially stronger credit metrics.

4. The Rest for Corporate Growth

The remaining proceeds will fund general corporate purposes, including investments in supply-chain expansion.

In other words, the company plans to invest in what it does best:

Optical networking.

Data-center connectivity.

Telecommunications infrastructure.

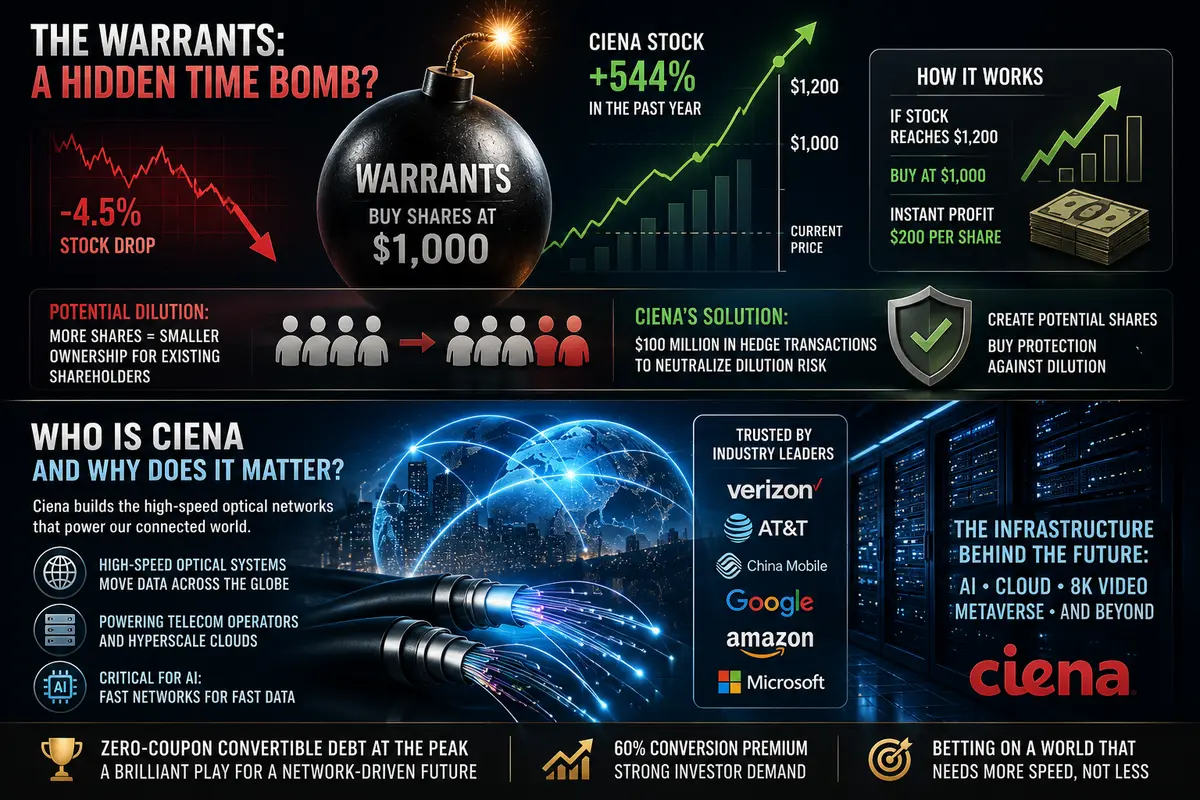

The Warrants: A Hidden Time Bomb?

There is one aspect of the transaction that caused concern among investors.

Alongside the convertible notes, Ciena entered into warrant transactions that effectively allow counterparties to purchase shares at $1,000 per share.

That’s a 114% premium to the current stock price.

It sounds far-fetched today.

But if Ciena’s stock continues its extraordinary rise—having already gained 544% over the past year—those warrants could become highly valuable.

If the stock reaches, say, $1,200, warrant holders would be able to buy at $1,000 and immediately profit.

That creates potential dilution.

More shares outstanding means existing shareholders own a smaller percentage of the company.

This dilution risk is precisely what spooked the market, contributing to a 4–5% decline in Ciena shares following the announcement.

However, Ciena anticipated this concern.

The hedge transactions funded by that $100 million are specifically designed to neutralize much of the dilution effect.

It’s a sophisticated structure:

Create potential shares on one side.

Purchase protection against dilution on the other.

Like a juggler tossing three balls into the air and catching each one exactly where intended.

Who Is Ciena and Why Does This Matter?

For those who don’t follow telecom infrastructure, some context is helpful.

Ciena isn’t a consumer brand.

You won’t buy a Ciena smartphone.

You won’t subscribe to a Ciena internet package.

But without companies like Ciena, the internet itself would struggle to function.

The company builds optical systems that move enormous volumes of data across vast distances at extremely high speeds.

Its customers include major telecom operators and hyperscale cloud providers such as Verizon, AT&T, China Mobile, Google, Amazon, and Microsoft.

In the age of artificial intelligence, that makes Ciena increasingly important.

Training large AI models requires moving massive amounts of data between servers and data centers.

The fastest NVIDIA chip in the world is useless if data can’t reach it quickly.

And that data travels across optical networks—many of which rely on equipment supplied by Ciena.

This is one reason the company’s stock has surged more than 544% over the past year.

The market isn’t merely rewarding current results.

It’s pricing in a future where AI demands ever-faster, ever-larger network capacity.

And at that peak, Ciena chose to issue zero-coupon convertible debt.

A strategically brilliant moment.

When your stock is near record highs, you can demand a larger conversion premium and still attract strong investor demand.

Market Reaction: Why Did the Stock Fall?

At first glance, the transaction seems overwhelmingly positive.

Cheap capital.

Balance-sheet improvement.

Share repurchases.

Dilution protection.

So why did the stock decline?

The answer lies in signaling.

First, investors worried about potential dilution from the warrants.

Second, large debt offerings announced when a stock is near all-time highs often raise questions:

“Is management moving too quickly?”

“Do they know something we don’t?”

Third, after a 544% run, some investors simply chose to take profits.

That’s understandable.

A gain of that magnitude invites at least some profit-taking.

Historically, however, transactions like this often benefit long-term shareholders.

The company gains growth capital without meaningful interest costs and—with proper hedging—without significant dilution.

It’s about as close to free financing as public markets allow.

Financial metrics also suggest Ciena wasn’t desperate for cash.

With a current ratio of 2.73 and a debt-to-equity ratio of 0.55, the company appears financially healthy.

It simply took advantage of favorable market conditions.

What Happens Next?

The next major milestone is the expected closing of the offering on June 11, 2026.

After that, the clock starts ticking.

Until June 15, 2031, conversion will generally be permitted only under specific conditions.

One likely trigger would be the stock trading above the conversion price for a designated period.

If the stock remains below $746.66 when the notes mature in September 2031, investors receive their principal back.

No gain.

No loss.

(Inflation, of course, is another matter.)

If the stock rises above that level, noteholders can convert and participate in the upside.

Ciena may issue shares, but thanks to the hedge structure, the net effect on share count could be largely neutralized.

In theory, everyone wins:

-

Bondholders get downside protection and upside participation.

-

Shareholders get a stronger balance sheet.

-

The company obtains low-cost capital.

At least that’s the plan.

Not Their First Rodeo

Ciena is no stranger to convertible debt.

The company has issued convertible notes before.

In 2023, for example, it sold notes carrying a 4.00% coupon that continue to trade in the market today.

This deal is different.

A zero coupon.

A 60% conversion premium.

Those terms suggest substantial confidence from both management and investors.

Ciena isn’t merely hoping its stock rises.

It has effectively staked $2.5 billion of market credibility on that outcome.

Recent performance supports that confidence.

The company reported fiscal second-quarter 2026 revenue growth of roughly 40% year-over-year, beating consensus expectations.

Management also raised its full-year growth outlook to approximately 34%.

This is not a company struggling to survive.

It’s a company benefiting from powerful secular trends.

The Bigger Picture

Behind the numbers lies a larger story.

The world is moving toward ever-higher speeds.

Artificial intelligence.

Metaverses.

8K streaming.

Cloud gaming.

Remote surgery.

All require levels of network bandwidth that seemed unimaginable just a few years ago.

Ciena stands among a small group of infrastructure beneficiaries alongside companies such as NVIDIA, TSMC, and Broadcom.

The fact that it can raise $2.5 billion at zero interest sends a powerful signal.

Investors are willing to fund the infrastructure of the future.

Even in a world where U.S. dollar interest rates are around 5%, institutional capital is willing to lock up billions for seven years without a coupon payment simply for the possibility of future equity participation.

That’s more than financing.

It’s conviction.

It’s a bet on the future.

It’s confidence that seven years from now, high-speed networks will be even more essential than they are today.

Final Thoughts: Was It Worth It?

Ciena executed a remarkably elegant financing transaction.

At a moment when its stock was near historic highs and investors were eager to pay for future growth, the company secured the cheapest debt financing in its history.

Almost free.

It then used those proceeds to refinance more expensive debt, repurchase shares, and hedge future dilution risks.

Bondholders are betting on a 60% rise in the stock over the next seven years.

Investors who sold on Monday were worried about warrants and dilution.

Time will reveal who was right.

What is already clear is that Ciena delivered a master class in corporate finance:

When to raise capital.

How to deploy it.

And how to protect existing shareholders in the process.

Free money is free money.

When you use it to reduce debt, buy back stock, and strengthen your business at the same time, that’s financial engineering at its finest.

Now we’ll see where Ciena goes next—both literally and figuratively.

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.