Istanbul, Thursday: The Numbers Everyone Feared

On Thursday in Istanbul, the Central Bank’s quarterly inflation report presentation took place — an event that only a few years ago was a routine bureaucratic procedure, but now feels more like a wartime emergency briefing. Central Bank Governor Fatih Karahan stepped before the press and announced figures that likely made Turkish households reach for a strong cup of tea.

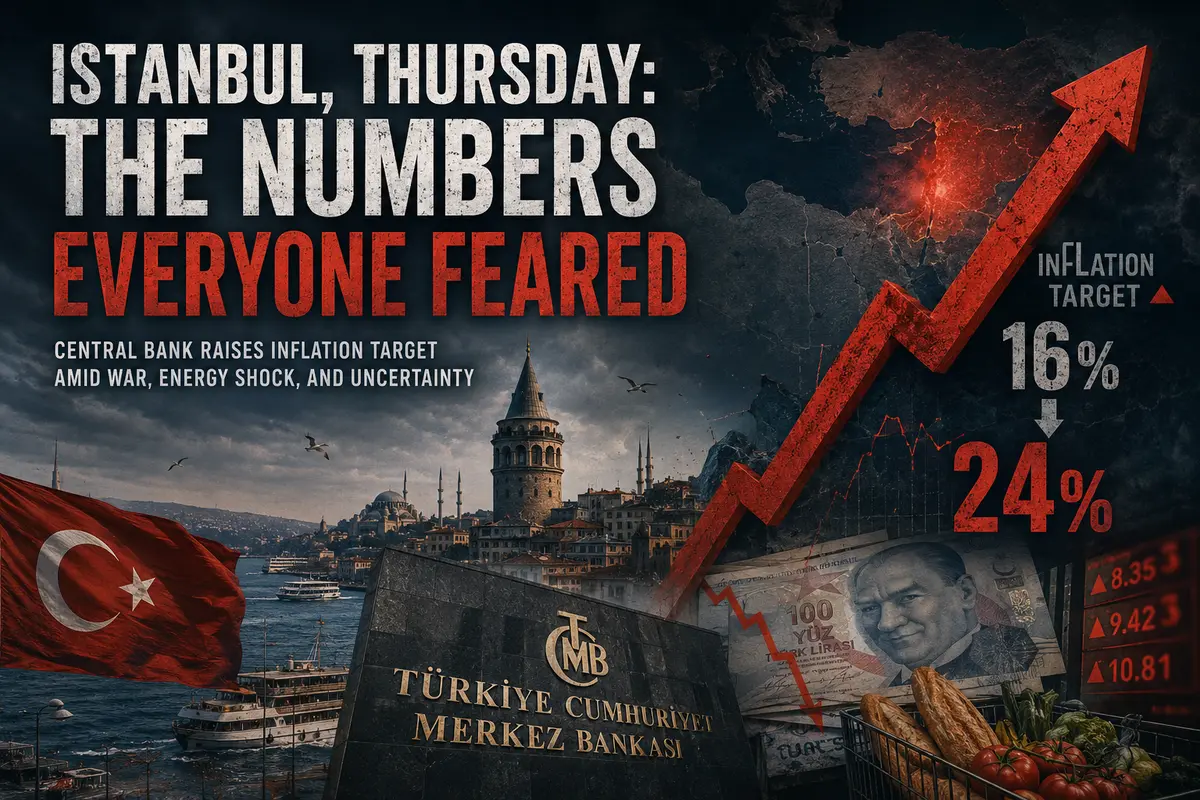

The interim year-end inflation target was raised from 16 percent to 24 percent. In a single stroke — an increase of eight percentage points.

This was not a minor adjustment, a technical clarification, or some statistical footnote that could be blamed on imperfect models. It was an admission that reality has turned out far harsher than even the most pessimistic analysts expected. And the main culprit was identified directly: the war involving Iran and its inflationary consequences, which, according to Karahan, will remain significant in the short term.

The Bank did not hide behind euphemisms or vague references to “geopolitical uncertainty.” The source of the shock was named explicitly.

A Chain of Revisions: 2027, 2028, and Beyond

But the revision did not stop with the current year. Karahan also announced that the Bank had raised its interim target for the end of 2027 from 9 percent to 15 percent. A new benchmark of 9 percent was then set for the end of 2028.

These figures tell an entire story on their own.

The Bank is effectively acknowledging that inflation will remain in double digits for at least another two years. The road downward will be long, painful, and filled with obstacles. Even by the end of 2028 — two and a half years from now — inflation, according to the Central Bank’s own projections, is still expected to stand at 9 percent.

That is not a number any central banker would proudly celebrate. But in Turkish realities, where inflation in recent years has surged above 80 percent, even these targets resemble a stabilization program rather than a surrender.

Context matters here. Turkey has lived with high inflation for years. Citizens have grown accustomed to mentally recalculating prices every few months. Businesses have learned to survive in an environment where planning horizons have shrunk to mere weeks. Meanwhile, the lira continues to lose purchasing power.

Under such conditions, revising the inflation target from 16 to 24 percent is not merely a statistical exercise. It is a signal to markets, citizens, and international partners that the Central Bank understands the scale of the problem and is no longer pretending that everything is proceeding according to plan.

The Energy Shock as the Main Enemy

Karahan was unusually specific when discussing the reasons behind the revision.

The key issue, he said, is the duration of regional tensions and the resulting pressure on energy supplies. Unlike many other countries, Turkey sits directly beside the conflict zone. Iran is a neighbor, and any disruption in regional energy flows hits the Turkish economy immediately.

Turkey imports a significant share of its energy resources. When oil and gas prices surge because of conflict in the region, the impact is instantly reflected in the cost of gasoline, heating, and electricity — and then spreads through the economy in a chain reaction, driving up food prices, transportation costs, and industrial goods.

This is a classic energy shock, one Turkey has experienced before. But now it is colliding with already elevated underlying inflation, creating an especially dangerous mix.

The governor stressed that the duration of this regional instability remains a critical risk factor for inflation forecasts. Behind those words lies a simple and unsettling logic: if the conflict drags on, if energy disruptions become chronic, and if oil prices continue climbing, then even the newly raised targets may prove unattainable.

The Bank understands this and appears to be trying to warn markets honestly that the situation remains highly uncertain.

The Language of Determination: No Compromises

Against this backdrop of grim numbers, Karahan delivered what was clearly intended as an anchor of confidence.

The Bank, he said, “will not compromise” in its determination to reduce inflation and will continue using all available tools to contain price growth.

This rhetoric matters.

In the past, Turkey’s Central Bank repeatedly came under political pressure to cut interest rates despite mounting inflation risks. There were periods when rates were slashed obediently, inflation exploded, and the lira collapsed.

Judging by Karahan’s tone, the current leadership is trying to signal that those days are over. The Bank intends to act as it sees necessary to rein in prices, even if doing so proves politically inconvenient or unpopular.

Still, there is always a gap between words and action.

Markets will now watch closely to see how this determination manifests itself in concrete policy moves. So far, the Bank has not announced emergency rate hikes or other drastic measures. What it has done is revise its forecasts upward — effectively admitting that previous assumptions were too optimistic.

Now investors and ordinary citizens alike are waiting for actions that demonstrate the tough rhetoric is backed by a genuine willingness to fight inflation, even at the cost of slower economic growth.

What This Means for Ordinary Turks

Behind all the macroeconomic language lies the daily reality faced by millions of people.

When the Central Bank raises its inflation forecast to 24 percent, it means prices for bread, cheese, meat, rent, and public transportation will continue rising at a pace that most Europeans or Americans would consider catastrophic. In Turkey, unfortunately, this has become normal.

The lira keeps weakening. Savings evaporate. Salaries, even when indexed, fail to keep pace with real price growth.

Every trip to the grocery store becomes an exercise in mental arithmetic: how much did this cost last month, how much does it cost now, and how much more expensive will it be next month?

In such an environment, economic behavior changes radically. Nobody keeps savings in the national currency longer than absolutely necessary. Anyone with the means converts money into dollars, gold, or real estate — anything rather than watching the lira dissolve before their eyes.

Businesses face similar pressures. When inflation expectations are both high and unstable, long-term investment planning becomes nearly impossible. Companies do not know what raw materials or labor will cost six months from now, so instead of expanding operations, they prefer holding hard currency or moving capital abroad altogether.

Regional Context: War at the Doorstep

It is impossible to understand Turkey’s current economic situation without considering what is happening just across its borders.

For Turkey, the conflict involving Iran is not some distant geopolitical abstraction or a headline scrolling across television screens. It is a direct threat to energy supplies, trade routes, and regional stability.

Turkey shares a border with Iran, and any upheaval there immediately reverberates through the Turkish economy. Refugee flows, supply disruptions, rising military expenditures, and uncertainty along the borders all place pressure on the budget, fuel inflation, and frighten away foreign investors.

“War at the doorstep” is not a metaphor here — it is an economic reality Ankara must contend with every day.

Moreover, Turkey is attempting to play its own role in regional diplomacy, balancing between competing power centers. That requires resources, diplomatic effort, and, once again, money. Every additional day of instability in the Middle East represents not only a geopolitical headache for Turkey, but also a direct blow to its inflation outlook.

Can the Central Bank Hold the Line?

The question now being asked by observers and market participants is straightforward: can the Central Bank truly guide the country through this storm?

On one hand, Karahan’s rhetoric sounds firm. He speaks of determination, of using every available tool, of refusing compromise. On the other hand, inflation targets have been revised sharply upward, and even the new projections look ambitious given current price dynamics.

The history of Turkish monetary policy over recent years encourages caution.

Too often, bold declarations about fighting inflation were followed by abrupt reversals and politically motivated rate cuts. Investors, hardened by experience, will wait not for speeches but for actions — concrete measures demonstrating that the Bank is genuinely prepared to keep interest rates high for as long as necessary, even if it means slower lending growth and a cooling economy.

For now, Karahan has delivered the market an honest, if unpleasant, forecast. He acknowledged the scale of the problem. He identified the principal threat — prolonged regional instability. And he promised not to surrender.

Now comes the harder part: action.

And every day, the Turkish lira, the prices in Istanbul’s bazaars, and millions of households will deliver their own verdict on whether the Central Bank can withstand the pressure — or whether inflation will once again prove stronger than forecasts, promises, and policy alike.

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.