Gold Rush: How Elliott’s Billion-Dollar Bet Shook Northern Star

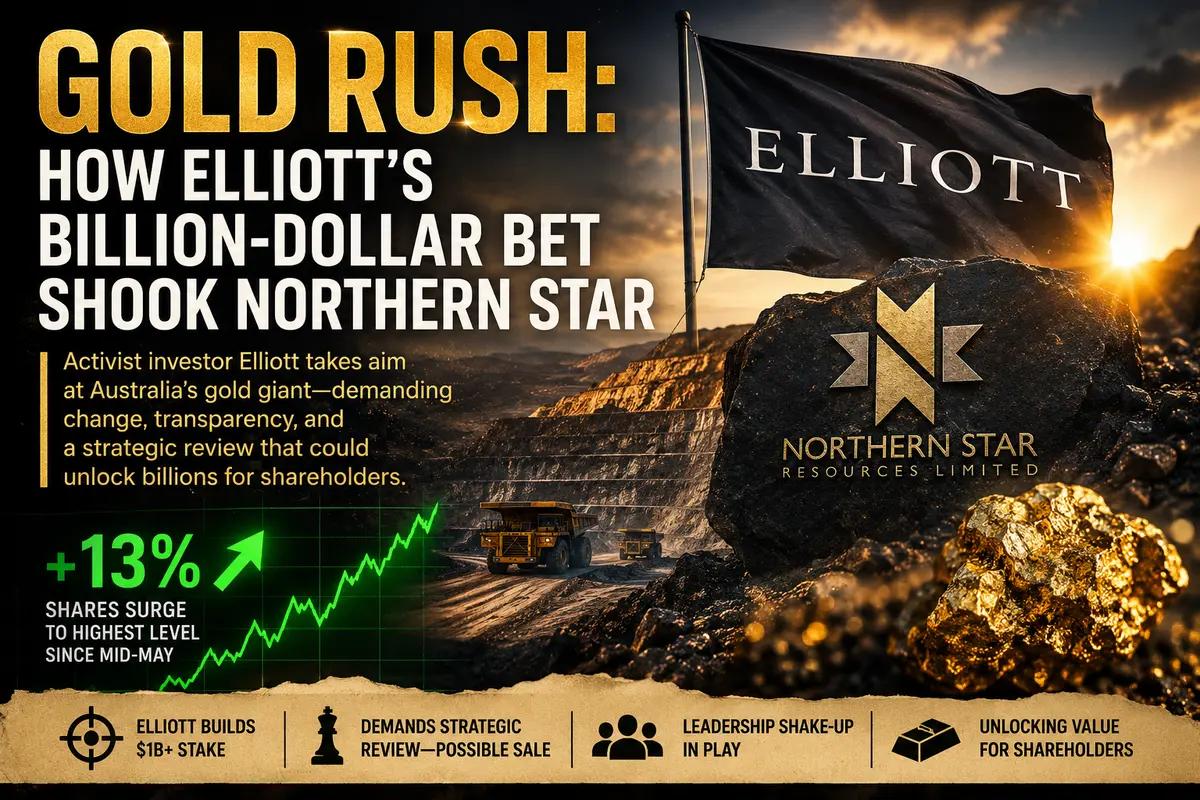

There are certain types of news in financial markets that hit like an electric shock. When Elliott Investment Management, one of the world’s most prominent and aggressive activist hedge funds, reveals a major stake in a company, it is never accidental. There is always a strategy, a plan, and a willingness to fight behind the move. On Tuesday, Elliott disclosed a stake worth more than A$1 billion in Northern Star Resources, the Australian gold miner. The company’s shares immediately surged more than 13%, reaching their highest level since mid-May.

This is a classic market reaction to the arrival of an activist investor: everyone knows Elliott will not sit quietly on the sidelines. It will push for change. And those changes typically lead to higher shareholder value.

Elliott Isn’t Just Visiting: What’s Behind the Stake Disclosure

Elliott Investment Management is not a passive fund that buys shares and waits quietly for dividends. It is an activist investor with a long history of successful campaigns against companies it believes are undervalued due to poor management. When Elliott takes a position, it usually means significant changes are coming—either voluntarily or under pressure.

In Northern Star’s case, Elliott wasted no time getting to the point. The fund stated that the gold miner should undertake a strategic review that could include a sale of the company. This is not merely a suggestion—it is effectively an ultimatum. Elliott believes Northern Star is undervalued and argues that the problem lies not in market conditions but in management execution.

The fund accused the company of “operational missteps” and “insufficient disclosure” compared with its peers. Put simply, other gold miners are operating more effectively and communicating more transparently, while Northern Star has, in Elliott’s view, obscured problems behind limited reporting.

The market clearly agreed. Shares jumped 13% because investors understand that when a fund like Elliott gets involved, corporate value often increases. Elliott is expected to pressure the board to improve operational performance, enhance transparency, and potentially explore a sale to a strategic buyer. Any of these outcomes could create substantial value for shareholders.

Operational Missteps: What Went Wrong at Northern Star?

Northern Star is one of Australia’s largest gold producers. The company operates mines in Western Australia and Alaska, producing hundreds of thousands of ounces of gold annually.

At first glance, the business should be thriving. Gold prices remain near historic highs, demand for the precious metal is strong, and geopolitical uncertainty continues to fuel interest in safe-haven assets.

Yet Northern Star’s shares had fallen 14% since the start of 2026. While many gold producers benefited from strong gold prices, Northern Star lagged behind. Elliott attributes this underperformance to operational shortcomings.

What exactly are those shortcomings? They likely include cost overruns in developing new projects, delays in bringing operations online, and mining costs that have risen above expectations. When gold prices are elevated, investors expect margins to expand. If margins fail to improve, it suggests the company is not managing costs efficiently.

Insufficient disclosure is a separate concern. When a company fails to provide detailed information about its operations, investors struggle to assess risks accurately. In the absence of clarity, markets tend to assume the worst and apply a valuation discount. Elliott’s demand for greater transparency is one that investors appear to fully support.

Leadership Transition: The Perfect Time for an Activist Campaign

Elliott has chosen an ideal moment to make its move.

Northern Star’s Managing Director, Stuart Tonkin, has announced plans to step down after thirteen years with the company. His departure creates a leadership vacuum. The old leader is leaving, while a successor has yet to be appointed. The board is in a transitional phase and therefore more vulnerable to external pressure.

Elliott is taking advantage of that situation. The fund has stated that it will push for a faster CEO appointment process and changes to the composition of the board.

This is a classic activist strategy: prevent the company from quietly selecting a successor and instead influence the process—or potentially secure a preferred candidate. A CEO appointed under Elliott’s influence would likely be expected to pursue the strategic agenda favored by the fund. That agenda begins with a strategic review and could ultimately culminate in a sale of the company.

For shareholders, such an outcome could be highly attractive. Corporate sales typically occur at a premium to the market price. Based on its public statements, Elliott appears convinced that Northern Star is worth substantially more than the market currently recognizes—and it is prepared to fight to unlock that value.

An Underperformer That Could Become a Leader

The irony is that Northern Star operates in a sector that should currently be flourishing.

Gold prices are rising, inflation remains elevated, and geopolitical risks continue to mount. Other major gold producers, including Newmont, Barrick, and Agnico Eagle, have delivered stronger results.

Elliott sees Northern Star as an asset that trails its competitors not because of inferior mines, but because of inferior management execution. Improve leadership, boost operational efficiency, increase transparency, and the company could be revalued accordingly.

The market appears to share that view. A 13% gain in a single day is more than a reaction to headlines—it represents a reassessment of the company’s intrinsic value based on the possibility that Elliott can successfully drive change.

Investors are effectively pricing in the probability of a successful activist campaign. If Elliott achieves its objectives, the shares could rise further. If it fails, they could retreat toward previous levels. History, however, suggests that Elliott rarely loses these battles.

What Comes Next for Northern Star?

Northern Star now faces several potential paths.

The first scenario is that the board accepts Elliott’s demands, launches a strategic review, and ultimately sells the company. In this case, shareholders would likely receive a takeover premium.

The second scenario is resistance. The board could oppose Elliott’s proposals, prompting the fund to increase its stake and launch a proxy battle for board seats. Such campaigns are lengthy and exhausting, but Elliott has extensive experience fighting—and winning—these contests.

The third scenario is a compromise. The company appoints a new CEO acceptable to Elliott and undertakes internal reforms without pursuing a sale. In that case, the stock could appreciate as operational performance improves.

Every one of these outcomes appears preferable to the status quo. That is why the market reacted so strongly to the news.

Elliott has not arrived to dismantle value—it has arrived to create it. And Northern Star appears to be on the verge of significant change.

The gold mine may end up with a new owner—or, at the very least, a new management team. For shareholders who have watched the stock decline throughout the year, there is finally a reason to see light at the end of the tunnel.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.