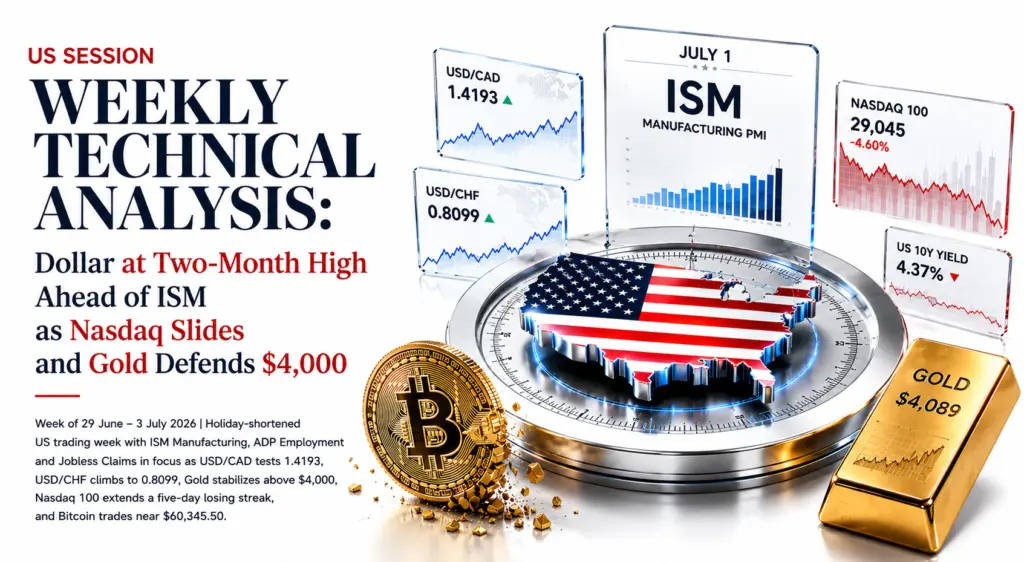

US Session Weekly | 29 June–3 July 2026 | Holiday-Shortened Week Dollar Hits Two-Month High. Nasdaq 100 Five-Day Losing Streak. Bitcoin at $60,345.50. ISM Manufacturing Is the Week’s Decisive Catalyst

DXY above 100 for first time since May 2025. USD/CAD 1.4193 — best since late January. USD/CHF 0.8099. Gold $4,089 after fourth consecutive weekly decline, briefly sub-$4,000. Nasdaq 100 -4.60% on five-day losing streak from June 3 record near 30,762. US 10Y 4.37% (-7bps). BTC $60,345.50 — lowest since late 2024. ADA $0.146 multi-year lows. US markets closed Friday.

LEVEL

HEADING INTO THE WEEK

USD/CAD

1.4193

Five-month high (best since late Jan). Dollar + deteriorating Canadian growth + gold pullback. ISM Tue + NFP Thu are the gates.

USD/CHF

0.8099

DXY above 100 first time since May 2025. CHF safe-haven demand outweighed by greenback rally.

Gold XAU

$4,089

Fourth consecutive weekly decline. Briefly sub-$4,000 before Friday PCE bounce reclaimed $4K. $3,800-$3,900 structural floor.

Wheat CBOT

588.45c

Eased from 3-week high. Hormuz freight premium easing + improving US harvest + Black Sea conditions.

Nasdaq 100

29,045

-4.60%. Five-day losing streak from June 3 record near 30,762. Chip rout + delayed AI IPO headlines drove the fall.

US 10Y Yield

4.37%

-7bps. Seven-week low. In-line PCE trimmed (not eliminated) multiple-hike bets. Core PCE held at 3.4%.

Bitcoin BTC

$60,345.50

Lowest since late 2024. Spot ETF outflows accelerated. Capital rotating to defensive equity + AI infrastructure.

Cardano ADA

$0.146

Multi-year lows. Amplified BTC breakdown on smaller cap + thinner institutional liquidity.

A hawkish-priced dollar and a five-day Nasdaq losing streak. Does ISM Manufacturing on Tuesday deliver the reprieve, or does a holiday-shortened week with Friday closure deliver thinner liquidity and sharper moves?

USD/CAD at 1.4193: The Most Consequential North American Pair

USD/CAD at 1.4193 is the most consequential North American pair for the week. The loonie’s slide to a five-month high in USD/CAD terms — its best level since late January — reflects a combination of broad-based dollar strength and a deteriorating Canadian growth profile that has left the pair without a meaningful domestic counterweight to the Fed’s hawkish posture. The article specifically notes that gold’s pullback has become a more relevant driver for CAD than oil, which captures something important about the current CAD dynamic: the traditional commodity-currency support that oil had been providing is being replaced by gold-driven risk sentiment, and with gold in its fourth consecutive weekly decline, CAD is losing that secondary support channel.

The Bank of Canada’s rate path is the structural anchor. With the Fed holding at 3.50 to 3.75% under Warsh and the BoC having been in an easing cycle, the rate differential has been widening in the dollar’s favour. USD/CAD’s 52-week high is the upside target once the 1.4193 level is confirmed as a platform rather than a peak. The ISM Manufacturing print on Tuesday and NFP on Thursday are the week’s primary directional catalysts — a strong ISM extends USD/CAD toward 1.4300; a miss would create the first meaningful pullback opportunity toward 1.4100.

USD/CAD direction: Higher; five-month high with both rate differential and commodity headwinds for CAD

Entry: 1.4150-1.4170 on any intraweek dip

Stop: 1.4050 — below structural support; would require sharp dollar reversal

Target: 1.4300-1.4350 — next extension above five-month high

Key gates: ISM Manufacturing Tuesday; NFP Thursday

USD/CHF at 0.8099: DXY Above 100 for First Time Since May 2025

USD/CHF at 0.8099 reflects the same dollar story as USD/CAD but with the Swiss franc’s safe-haven overlay removed by the Iran ceasefire. The DXY breaking above 100 for the first time since May 2025 is the headline dollar milestone of the week — it marks the dollar index at a two-month high and represents the cumulative effect of Warsh’s hawkish hold, the 3.4% core PCE print, and the market’s repricing of September hike probability. The CHF safe-haven demand that had been a structural support for the franc was outweighed by the broad-based greenback rally. With the Iran ceasefire now established and Hormuz normalising, the war-premium support for CHF has also deflated.

USD/CHF at 0.8099 is approaching the 52-week high range of 0.8190 to 0.8217. The near-term catalyst for whether it reaches that zone: ISM Manufacturing on Tuesday. A beat above 52 that signals US manufacturing re-expansion would be the clearest possible argument for continued dollar strength and push USD/CHF toward the 52-week high. A miss below 48 would give the first meaningful evidence of a slowdown and create a pullback opportunity.

USD/CHF direction: Higher toward 52-week high range 0.8190-0.8217

Entry: 0.8060-0.8080 on any dip

Stop: 0.7980 — below structural support

Target: 0.8190-0.8217 — 52-week high range

Gold at $4,089: The Fourth Weekly Decline and the PCE Floor

Gold’s fourth consecutive weekly decline — marked by a brief break below $4,000 for the first time since November 2025 before a Friday PCE-driven dollar pause sparked a recovery to $4,089 — is the most analytically important price action in the commodities complex. The sub-$4,000 print and the subsequent recovery tell two different stories simultaneously. The break below $4,000 is the war premium continuing to exit: with Hormuz normalising, the Iran conflict-era premium that took gold from $3,000 to $5,595 is being systematically removed. The recovery back above $4,000 is the structural bid from central bank accumulation — WGC Q1 2026 demand at 1,231 tonnes — asserting itself as the floor.

The $3,800 to $3,900 zone is where CSFX identifies the structural support as most credible. The $4,089 level is approximately $189 to $289 above that zone. For the coming week, gold is a passive instrument rather than an active one: the primary direction will be set by ISM Manufacturing and NFP, with strong data extending the dollar and pushing gold toward $3,900 to $3,950, and a data miss providing relief that allows gold to recover toward $4,200. A Warsh speech at Sintra that is more neutral than expected is the tail risk bullish catalyst for gold.

Gold structural floor: $3,800-$3,900 — central bank accumulation bid zone

Accumulate on dips: $3,900-$3,950 — approaching structural floor; better R:R than $4,089

Stop: $3,700 — below structural support; would require full war-premium removal and hawkish PCE combo

Target: $4,300-$4,350 — recovery if dollar softens on weak ISM/NFP

Wheat at 588.45 Cents: Hormuz Premium Exits

Chicago wheat at 588.45 cents per bushel eased back from a three-week high as the easing Strait of Hormuz tensions reduced the war-risk freight premium that had been embedded in agricultural commodity prices since February. Improving US harvest progress and favourable Black Sea conditions — both sources of supply-side relief — compounded the freight premium removal. The EU heatwave pushing 40 degrees Celsius across France, which had been providing supply-side support through concern about crop quality, is the offsetting factor that prevented a sharper decline.

Wheat at 588.45 cents is in a range defined by the intersection of two forces: the supply-restoration from Hormuz normalisation pushing prices lower, and the EU heatwave-driven crop quality concern pushing them higher. That range is approximately 570 to 620 cents. The EIA inventory data and any update on Black Sea corridor activity are the near-term directional catalysts this week.

Wheat range: 570-620 cents — Hormuz deflation vs EU heatwave support

Accumulate dips: 570-580 cents — EU heatwave supply concern provides structural bid

Nasdaq 100 at 29,045: The Five-Day Losing Streak From Record Highs

The Nasdaq 100’s 4.6% decline on the week — its worst since the early-June record near 30,762 — is the equity story of the session. The index posted a fifth consecutive losing session on Friday, with the move driven by a chip-sector rout and reports of a delayed AI-sector IPO triggering the sharpest weekly decline since the record high. The distance from the June 3 record of approximately 30,762 to Friday’s close at 29,045 is 1,717 points — a 5.6% correction from the high.

The analytical question is whether this is a healthy pullback from record territory or the beginning of a more sustained de-rating of high-multiple technology names. The context: the US 10-year yield at 4.37% represents an opportunity cost for long-duration equity valuations. Warsh’s hawkish hold with September hike probability elevated means the rate environment for high-multiple tech is not improving near term. The Nasdaq’s five-day losing streak in the context of a two-month dollar high is the expression of that valuation headwind. The 28,500 to 28,800 zone is the next support. A Warsh Sintra speech that is neutral or dovish on Tuesday would be the clearest catalyst for a relief rally back toward 30,000.

Nasdaq 100 direction: Cautious; five-day streak from record high

Support: 28,500-28,800 — next technical support below 29,045

Recovery gate: Warsh Sintra neutral + weak ISM = relief rally toward 30,000

Short entry: 29,800-30,000 on any rally — fade extended move back toward record

US 10-Year at 4.37% and Bitcoin at $60,345.50

The US 10-year Treasury yield easing to 4.37% — a seven-week low, down seven basis points on the week — is somewhat paradoxical in a week that also saw the DXY hit a two-month high and September hike probability remain elevated. The explanation is the PCE print: the 3.4% core year-on-year reading was marginally above the 3.3% consensus but broadly in-line, and the market’s read was that May represents the inflation peak rather than a new upward trend. That interpretation trimmed but did not eliminate multiple-hike bets. With the 10-year at 4.37% and the dollar at a two-month high, the bond market is sending a slightly more ambiguous signal than the FX market on the Fed’s path.

Bitcoin at $60,345.50 — its lowest level since late 2024, down 8.4% — is experiencing the specific problem of a crypto market that is losing on two fronts simultaneously. Spot ETF outflows are accelerating, which removes the institutional accumulation floor that had been supporting BTC through the year. Capital is rotating toward defensive equity sectors and AI infrastructure plays, which means the rotation away from crypto is not just macro risk-off but also AI-thematic: institutional allocators who had been using BTC as a technology proxy are moving toward direct AI infrastructure exposure. Cardano at $0.146 at multi-year lows reflects the same dynamic with amplified downside.

BTC critical level: $60,000 — psychological floor; breach opens $56,000-$58,000

Accumulate: $58,000-$60,000 — structural accumulation zone if $60K holds

Stop: $55,000 — below key structural support

ADA: Patience at multi-year lows; 10% max speculative size

The Week’s Events: ISM, ADP, NFP

Tuesday: ISM Manufacturing PMI (15:00 ET). The single most important data release of the week for the US session. Above 52 = US manufacturing re-expansion, dollar extends, Nasdaq under further pressure from rate headwind. Below 48 = contraction signal, dollar softens, Nasdaq relief rally possible. Also Tuesday: ADP employment for June (13:15 ET, consensus ~150,000). A strong ADP raises the bar for Thursday’s NFP.

Wednesday: Weekly jobless claims (08:30 ET). Secondary indicator but relevant context for Thursday.

Thursday: US Nonfarm Payrolls and Average Hourly Earnings for June, released Thursday rather than the usual Friday due to the Independence Day closure. This is the week’s definitive macro event for the US session. Holiday-shortened week with lighter liquidity means NFP Thursday carries larger-than-typical move potential. US markets then close Friday. Consensus for NFP approximately 180,000. Above 200,000 with earnings above 3.5% = dollar extends, Nasdaq faces renewed rate pressure, BTC tests $58,000. Below 150,000 = dollar softens, Nasdaq relief rally, BTC holds $60,000 floor.

Read Full Report: capitalstreetfx.com/market-analysis/daily-market-analysis/

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.