Thames Water: A Life-or-Death Deal for Britain’s Water Empire

Nightmare on Kensington Road: How Britain’s Largest Water Company Ended Up on Its Knees

Imagine London without water. Not for an hour, not for a day — forever. Taps run dry, toilets stop flushing, showers stop working, factories shut down, and hospitals switch to emergency mode. It sounds like the plot of a disaster movie. Yet for the 16 million people served by Thames Water, this scenario has seemed increasingly plausible over the past two years.

The company that supplies water and wastewater services to London and the Thames Valley has been teetering on the brink of collapse. Its debts exceed £15 billion. Its infrastructure is aging and leaking. Regulators have been poised to intervene at any moment. Shareholders have been fleeing without looking back.

Then, on Wednesday, June 10, 2026, a glimmer of hope appeared. Or perhaps another nail in the coffin, depending on your perspective.

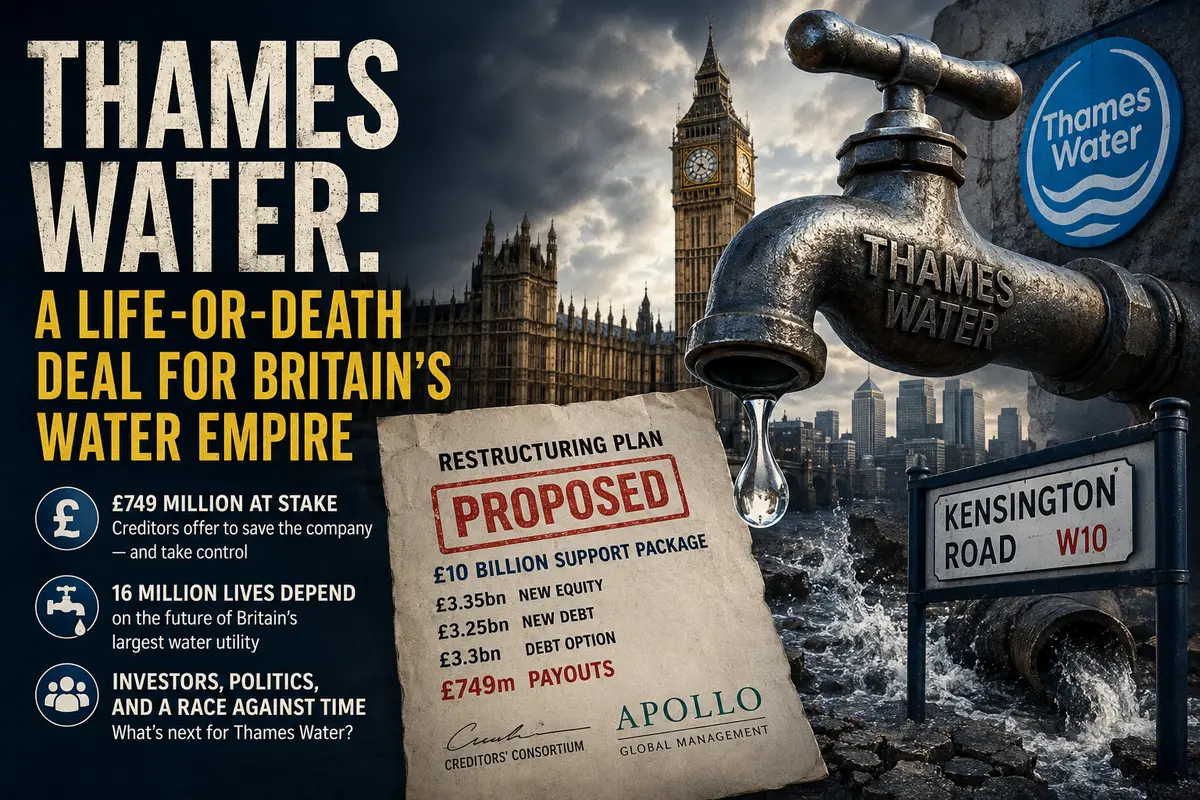

Thames Water’s creditors have proposed a restructuring plan that could save the company. But the price of salvation is control. The creditors want ownership of the company—and they are prepared to pay £749 million to secure it.

That may sound like a large sum. For a company carrying tens of billions in debt, however, £749 million is pocket change. This deal is not really about money. It is about who will control water services for millions of people.

The creditors are hedge funds and investment firms based in New York, Delaware, and the Cayman Islands. They are not water utility specialists. They are specialists in extracting returns from distressed assets. And a British public already frustrated by decades of underinvestment in infrastructure is watching this deal with equal measures of hope and alarm.

Let’s take a closer look at what exactly the creditors are proposing, who is behind the plan, and what lies ahead for Thames Water.

The Numbers: £749 Million at Stake

Let’s begin with the hard numbers, because they are striking even by the standards of seasoned bankers.

According to documents reviewed by the Financial Times, the total payments associated with the restructuring could reach £749 million.

How is that figure allocated?

-

£160 million in fees for senior creditors—the lenders first in line to be repaid in the event of insolvency.

-

£254 million in various transaction-related expenses.

-

£285 million in accrued interest that Thames Water would pay upon completion of the deal.

-

£50 million in fees for other creditors.

Total: £749 million.

But this is only the tip of the iceberg.

The core of the deal is not the fees but the fresh capital. Creditors are prepared to inject:

-

£3.35 billion in new equity capital, making them the owners of the company.

-

£3.25 billion in new debt financing.

-

An additional £3.3 billion debt option if further funding becomes necessary.

In total, the financial support package could approach £10 billion.

That is a serious commitment—larger than the net worth of some British billionaires and comparable to the annual budget of a small country.

Who stands behind these commitments?

Apollo Global Management, the U.S. investment giant with more than $500 billion in assets under management, is guaranteeing the entire financing package. Apollo could receive the £160 million fee earmarked for senior creditors, while the remaining creditors would receive smaller shares.

What Changes for Consumers: Penalties, Investment, and Hope

For ordinary Londoners paying their water bills, this deal could either improve or worsen the situation. Much depends on how the regulator, Ofwat, evaluates the proposal.

On one hand, creditors have agreed to a framework under which Thames Water could avoid certain new regulatory penalties over a four-year period.

In exchange, the company would commit £700 million of investor funding toward improving its assets and infrastructure.

Rather than paying fines for leaks, poor water quality, and overloaded sewer systems, the company would be able to spend that money repairing pipelines, upgrading treatment plants, and modernizing pumping stations.

In theory, this should improve service quality.

On the other hand, avoiding penalties means the company would not be punished for past failures.

And Thames Water has accumulated plenty of them.

For years, Ofwat has warned about deteriorating infrastructure. Water is lost through leaking pipes. Untreated sewage is discharged into rivers because sewer systems cannot cope with heavy rainfall. Investment levels have been inadequate for a long time.

The current shareholders—primarily major investment funds from Canada, China, and Abu Dhabi—failed to invest enough in modernization. They preferred collecting dividends to replacing pipes.

Now the creditors are proposing a different model. They would own the company, control it, and invest in it.

The question is whether they will invest enough—and in the right areas. Or whether they, too, will prioritize profits while leaving the infrastructure fundamentally unchanged.

The Political Dimension: Conservative Defenses, Left-Wing Demands

In Britain, Thames Water is more than a business. It is a political issue.

Opposition parties have accused successive Conservative governments of allowing the crisis to develop. Labour, which has long argued for greater public control over utilities, has repeatedly raised the possibility of bringing water infrastructure back under public ownership.

Their argument is simple:

Water is a public necessity and should not be controlled by financial speculators.

Supporters of the current model counter that private-sector management is more efficient and that nationalization would cost taxpayers tens of billions of pounds.

Interestingly, the creditors’ proposal contains one element that may appeal to both sides.

The plan envisions a governance structure that could lead to an initial public offering (IPO) in 2030.

In other words, Thames Water could once again become a publicly traded company within four years—privately managed but publicly listed, with all the transparency and accountability requirements that come with stock market scrutiny.

That could represent a compromise:

Not nationalization, but not a company hidden entirely within the portfolios of hedge funds either.

A public company accountable to investors, regulators, and customers.

Ofwat has stated that it is reviewing the proposal to determine whether it would benefit consumers and the environment.

That is the key test.

The regulator’s role is to protect consumers—not shareholders. If Ofwat concludes that the deal does not serve the public interest, it could block the proposal.

The Creditors: Who Are They and What Do They Want?

Let’s look more closely at the mysterious creditors seeking control over the water supply of 16 million people.

The leading player is Apollo Global Management.

Founded in 1990 by Leon Black, Josh Harris, and Marc Rowan, Apollo manages more than half a trillion dollars in assets. Its investments span real estate, insurance, renewable energy, and even space technologies.

Apollo is known for its aggressive investment style and its ability to generate profits from distressed situations.

But Apollo is only one participant.

The creditor group includes dozens of hedge funds, investment firms, and insurance funds. Many are registered in offshore jurisdictions such as the Cayman Islands, Delaware, and Bermuda.

Many are not required to disclose their ultimate beneficial owners.

The public often has little visibility into who ultimately controls the money behind these funds.

Why are they interested?

Because Thames Water is effectively a monopoly.

If you live in London, you cannot simply switch to another water supplier.

That creates a highly predictable revenue stream. Millions of customers pay their bills every month, and regulated tariff increases remain possible.

The creditors want to replace shareholders who invested too little while demanding too much.

Their pledge of £3.35 billion in fresh equity is a substantial commitment.

They are not merely seeking control—they are betting on a turnaround.

The challenge is that British consumers have heard similar promises before.

Since the privatization of the water industry in 1989, many water companies accumulated large debts while paying generous dividends and underinvesting in infrastructure.

Now another group of investors is arriving with promises of reform.

Will the public believe them?

The Alternatives: Nationalization and Other Scenarios

If the creditor-led deal collapses, Thames Water has several alternatives.

None of them are attractive.

1. Temporary Nationalization

The government could place the company into a Special Administration Regime.

This resembles bankruptcy protection but with one crucial difference: water service cannot be interrupted.

The government would run the company until a new owner is found.

That could cost taxpayers billions of pounds through debt restructuring, emergency funding, and infrastructure investment.

2. Sale to Another Private Investor

Another possibility would be selling the company to a different investor.

But who wants to buy a utility carrying more than £15 billion in debt?

Only someone willing to write off a substantial portion of that debt.

That would mean significant losses for existing creditors, who are likely to resist such an outcome.

3. Full Bankruptcy and Liquidation

The worst-case scenario.

The company would cease to exist, assets would be broken up and sold, and water services would have to be reorganized under emergency conditions.

Virtually nobody wants this outcome—not even the fiercest critics of private ownership.

As a result, the creditor proposal is widely viewed as the least disruptive option.

It preserves the company as a functioning entity, attracts fresh investment, and avoids operational chaos.

But the cost is handing control of critical infrastructure to financial investors.

International Experience: Are There Success Stories?

There are examples around the world of water utilities successfully restructuring after debt crises.

In the United States, several municipal water providers emerged from bankruptcy with new owners and improved infrastructure.

Europe has also seen successful restructuring cases in countries such as Spain, Portugal, and Germany.

Yet there are cautionary tales as well.

In parts of Latin America, water privatization often led to higher prices, deteriorating service quality, and public protests. Governments canceled contracts, and companies exited with significant losses.

Thames Water sits somewhere between these extremes.

This is not a developing country with weak institutions.

It is the United Kingdom, with a strong regulatory framework, independent oversight, and active public scrutiny.

If the deal is approved, Ofwat will closely monitor whether the new owners fulfill their commitments.

One particularly controversial element remains the proposed suspension of certain penalties.

The policy cuts both ways.

On one hand, it frees up money for investment.

On the other, it reduces immediate pressure on management to improve performance.

The regulator must strike a delicate balance:

Avoid crippling the company with fines while ensuring it does not become complacent.

What Happens Next?

The deal is far from complete.

Several hurdles remain:

-

Formal approval by creditors.

-

Regulatory review by Ofwat.

-

Potential government involvement if political concerns escalate.

-

Possible legal challenges.

Any of these stages could derail the process.

Creditors could disagree over fee allocations.

Ofwat could conclude that consumers would not benefit.

Political leaders could intervene, particularly if water policy becomes a major election issue.

The biggest risk may be legal.

Existing shareholders, whose stakes would effectively be wiped out, could challenge the restructuring in court.

These are large institutional investors with significant resources and legal firepower.

They are unlikely to surrender quietly.

Nevertheless, reports indicate that creditors remain optimistic.

They have already invested considerable resources into developing the proposal.

Apollo’s role as guarantor underscores the seriousness of the effort.

Deals involving billions of pounds are not assembled casually.

Conclusion: Rescue or Merely a Transfer of Ownership?

Thames Water stands at a crossroads.

The creditor-led restructuring, involving £749 million in payments and a transfer of control, could save the company.

Or it could simply replace one group of financial owners with another.

The proposed owners promise £3.35 billion in fresh equity investment—far more than current shareholders have invested in years.

That offers hope that pipes will be repaired, treatment facilities upgraded, and rivers cleaned up.

Yet the cost is significant:

-

Control of strategic infrastructure passing to American financial investors.

-

A four-year period with reduced exposure to certain penalties.

-

Continued debate over whether essential public services should be owned by private capital at all.

Ofwat is now reviewing the proposal.

Its decision will determine whether Londoners see meaningful improvements—or continue watching water leak from aging pipes while bills keep rising.

For now, life continues as normal. Water flows. Bills are paid.

But beneath the surface, a battle worth billions is underway.

A battle for control of water.

A battle for the future of 16 million people.

The deal could be finalized within weeks.

Or it could collapse under the weight of lawsuits, politics, and competing interests.

One thing is certain:

Water is life.

And whether life itself should become an asset class traded by Wall Street remains a question that Britain has yet to answer.

Comments

No comments yet. Be the first to share your thoughts!

Comments only for logged-in users.