Asian Stocks Fall as Chip Rally Cools

When the Party Ends

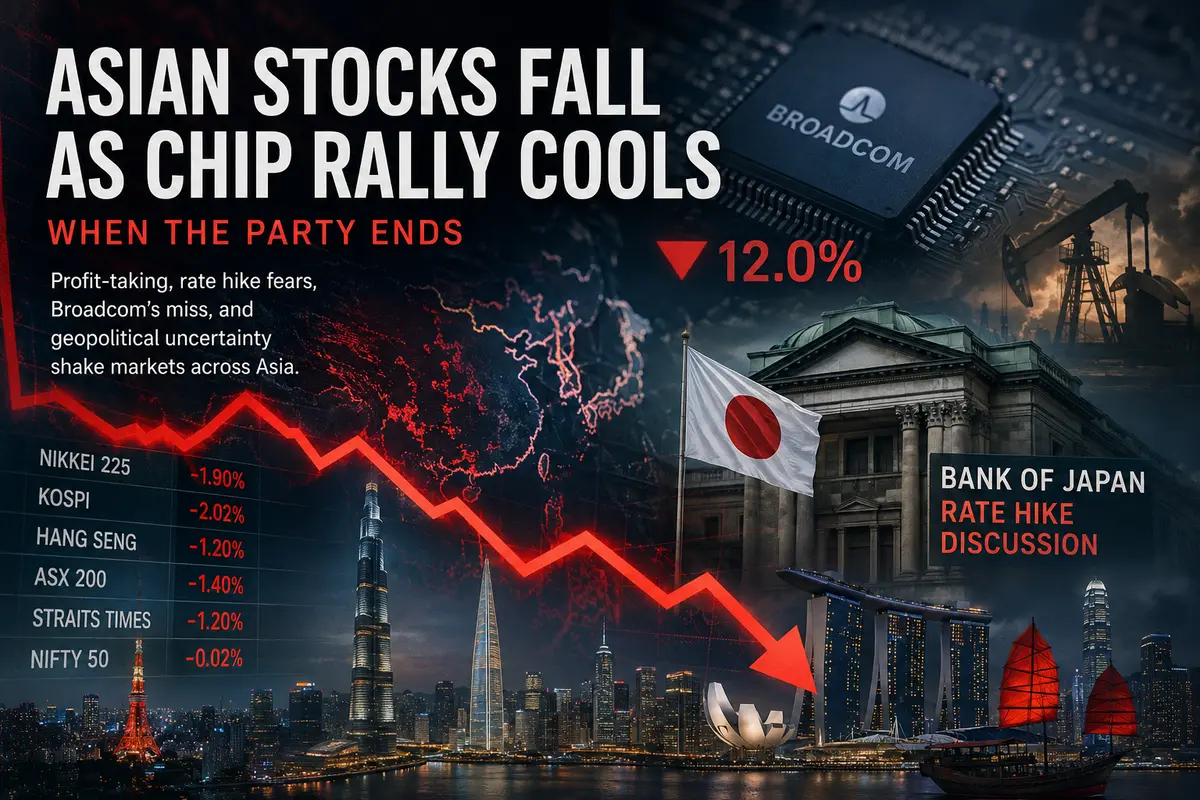

Thursday began with a hangover across Asian equity markets. After several days of record-breaking gains in technology and semiconductor stocks, reality set in. Indexes drifted lower—not in a panic, not in a crash, but steadily enough to leave little doubt: the rally is taking a pause.

Several factors contributed to the shift. The main one is simple exhaustion. After the Nikkei reached a fresh all-time high and South Korea’s KOSPI approached its own peaks, investors decided it was time to take profits—especially against a backdrop of increasingly unsettling news.

There were also more concrete triggers. Comments from the Governor of the Bank of Japan regarding possible interest-rate hikes. Mixed results from Broadcom that weighed on the entire semiconductor sector. Ongoing uncertainty surrounding U.S.-Iran negotiations. Together, these factors created a cocktail that Asian markets found hard to stomach.

S&P 500 futures, which often set the tone for global trading, fell 0.4% in after-hours trading. American investors are taking profits as well. The example is contagious.

Japan: Records Give Way to Losses

The Japanese market, which was celebrating only yesterday, found itself deep in the red today. The Nikkei 225 lost 1.9%, while TOPIX, the broader Tokyo Stock Exchange index, fell 1.4%. These are significant moves—the kind that prompt analysts to revisit their forecasts.

What happened?

First, profit-taking. The Nikkei hit record highs this week, and many investors who bought stocks a month or two ago saw their portfolios rise by 20–30%. The temptation to lock in real gains rather than admire paper profits proved stronger than faith in further upside.

Second—and perhaps more importantly—there were comments from Bank of Japan Governor Kazuo Ueda. Speaking at a seminar on Wednesday, he said something markets were not expecting, at least not yet.

Ueda warned that inflation in Japan could exceed target levels. The reason: an energy shock caused by the conflict with Iran. Japan imports nearly all of the oil and gas it consumes. When oil prices rise, everything becomes more expensive—from gasoline and groceries to utility bills and airline tickets.

According to Ueda, the central bank must discuss the pros and cons of raising interest rates. He did not say rates would definitely rise. He simply said the issue deserves discussion. But for a market accustomed to decades of near-zero interest rates, even a hint of tightening was enough to cause shockwaves.

Why are higher rates bad for stocks? Because they make borrowing more expensive for businesses, reduce corporate profits, lower the discounted value of future cash flows, and increase competition from bonds, which begin offering more attractive guaranteed returns.

The technology sector suffered the most. SoftBank Group, the giant investment holding company with stakes in dozens of tech firms worldwide, plunged nearly 11% in a single day. An 11% decline qualifies as a rout. The reasons include both rate concerns and the sharp drop in Broadcom shares in the U.S. While SoftBank does not directly own Broadcom, it has indirect exposure through its investment funds. When Broadcom falls, SoftBank feels the pain.

Chipmakers Tokyo Electron and Advantest also declined. They had risen too far, too fast on AI-driven optimism. Now comes the correction.

South Korea: Chips Drag the Market Lower

South Korea’s KOSPI fell as much as 2% during trading. In a country whose economy is deeply tied to semiconductor production, the market found itself at the center of the storm.

Samsung Electronics and SK Hynix—the two giants that together carry enormous weight within the index—fell between 2% and 4%. The decline was not catastrophic, but it was noticeable. More importantly, it followed a string of record highs. Traders were locking in profits, and buyers were scarce at current levels.

The Broadcom story added fuel to the fire.

Broadcom is an American company, but its influence on Asian markets is immense. It produces chips for communications, data centers, and automobiles. Its earnings and outlook serve as a barometer for the entire industry.

Broadcom reported quarterly results. Revenue came in slightly below expectations. The company maintained—but did not raise—its AI-related sales forecast for the current quarter, despite widespread expectations that guidance would be increased. The market punished the company accordingly, sending its shares down 12% in after-hours trading.

For Korean chipmakers, that is a troubling signal. If Broadcom, one of the industry leaders, cannot demonstrate accelerating growth in AI-related demand, perhaps demand for chips is not as unstoppable as many believed. And if chip demand weakens, Samsung and SK Hynix inevitably suffer.

The Korean market is also highly sensitive to geopolitical risks. North Korea has long been a source of concern. Now the Iranian factor has joined the equation. South Korea is a U.S. ally. If tensions with Iran escalate further, Korea could be affected indirectly. For now, it remains a hypothetical risk, but investors are already pricing it in.

China and Hong Kong: Diverging Paths

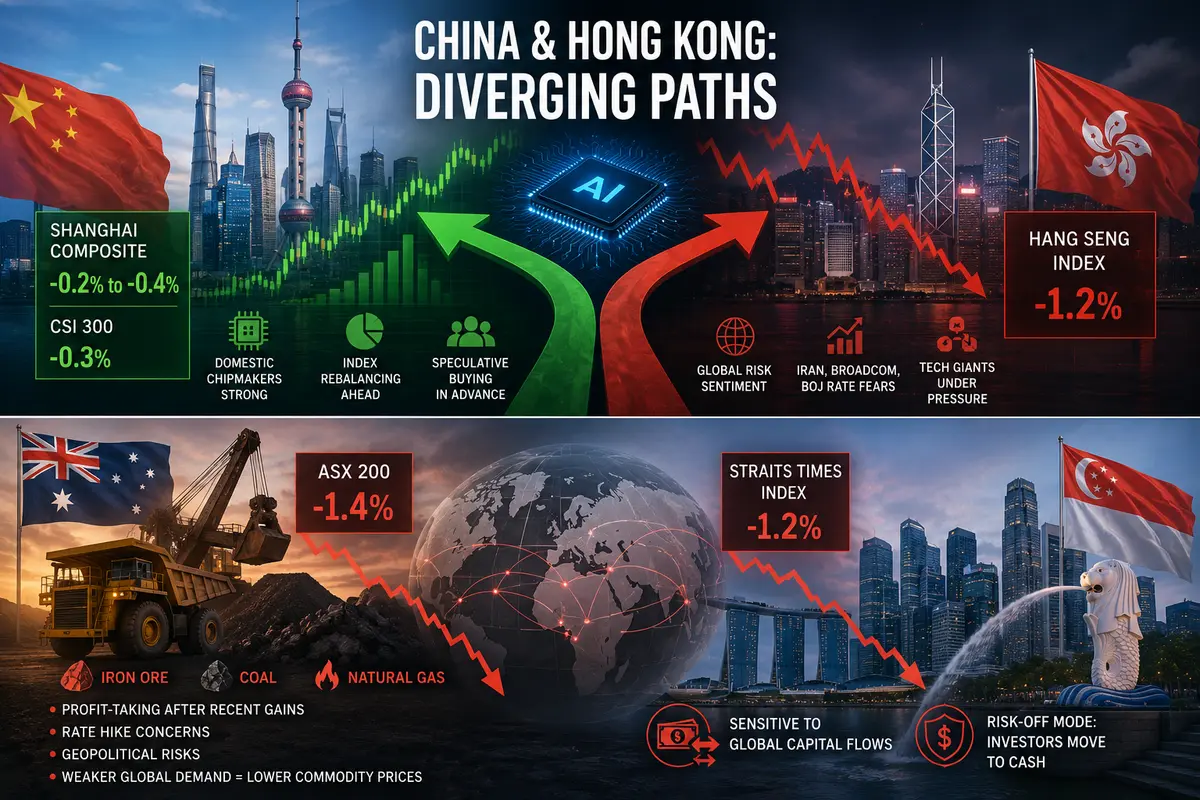

Chinese indexes held up better than most, though they still finished lower. The Shanghai Composite declined between 0.2% and 0.4%, depending on the benchmark, while the CSI 300 slipped roughly 0.3%.

Why did China fall less?

Because it is playing a different game. Domestic chipmakers continued to gain ground. Optimism surrounding China’s progress in artificial intelligence proved stronger than the prevailing global pessimism.

There is another factor as well. A major index rebalancing is expected on Friday. Funds tracking these indexes will be forced to buy stocks entering the benchmark and sell those leaving it. Semiconductor companies are expected to be among the beneficiaries. Speculators are positioning ahead of the event, buying now in anticipation of selling at higher prices to passive funds later.

Hong Kong’s Hang Seng Index performed worse, falling 1.2%.

As a global financial hub, Hong Kong is more exposed to international risk sentiment. When something goes wrong anywhere in the world, Hong Kong often reacts first. Concerns over Iran, Broadcom, and Japanese interest rates all weighed on the market.

Hong Kong technology giants Tencent, Alibaba, and Meituan lost ground after strong gains the previous week. A correction was inevitable.

Australia and Singapore: Also in the Red

Australia’s ASX 200 fell 1.4%.

The reasons were familiar: profit-taking after recent gains, concerns over interest rates—the Reserve Bank of Australia could also raise rates if inflation remains persistent—and, of course, geopolitics.

Australia’s economy depends heavily on commodity exports such as iron ore, coal, and natural gas. When the world appears to be edging closer to conflict, expectations for global demand can weaken. Lower demand means lower commodity prices, which in turn reduce mining profits and pressure the ASX 200.

Singapore’s Straits Times Index lost 1.2%.

Singapore may be small, but it is highly sensitive to global capital flows. When investors worldwide shift into cash and lock in profits, Singapore tends to feel the impact.

India: An Outlier

India’s Nifty 50 was little changed on Thursday.

That is not necessarily because the Indian market is particularly strong. Rather, it had already declined earlier. This week, the Nifty fell to its lowest level in nearly two months. The reasons include expensive oil—India imports more than 80% of its crude oil needs—and the lack of major domestic AI players.

Indian companies excel in outsourcing, IT services, and generic pharmaceuticals. But they do not dominate semiconductor manufacturing. They are not building large language models at scale. They are not constructing massive AI training data centers. As a result, the AI boom that propelled markets in the U.S., Japan, and South Korea largely bypassed India.

On the other hand, rising oil prices hit India particularly hard.

The country spends billions of dollars importing crude oil. When oil prices rise, the trade deficit widens, the rupee weakens, inflation accelerates, and the central bank may be forced to tighten monetary policy. Higher rates are generally bad news for equities.

For now, Indian investors remain defensive. They are not buying aggressively, but neither are they rushing for the exits. They are watching oil prices, the U.S. dollar, the Federal Reserve—and hoping the storm passes by.

Broadcom: How One Company Shook an Entire Sector

The Broadcom story deserves a closer look. It is a textbook example of how the earnings report of a single company can influence markets worldwide.

Broadcom may not be a household name, but among professionals it is a giant, with a market capitalization approaching $800 billion. Its chips power everything from smartphones and servers to automobiles and satellites.

On Wednesday after the market close, Broadcom reported quarterly revenue of $14.5 billion. That represented 12% year-over-year growth, but came in slightly below analysts’ consensus expectations.

The company projected roughly $3 billion in AI-related revenue for the current quarter—essentially unchanged from its previous forecast. Analysts had hoped for an upward revision, given expectations of accelerating AI-chip demand.

The market reacted harshly.

Broadcom shares plunged 12% in after-hours trading, erasing nearly $100 billion in market value in a single evening.

Why does this matter so much for Asia?

Because Broadcom serves as a canary in the coal mine for the semiconductor industry. If Broadcom struggles, investors worry the entire sector may be facing headwinds. That affects companies such as Samsung, SK Hynix, Tokyo Electron, Advantest, and dozens of other firms listed on Asian exchanges.

Of course, it is possible the reaction was excessive. Perhaps investors were simply looking for an excuse to take profits. Perhaps markets will recover tomorrow.

But today, the verdict was clear: sell.

Bank of Japan: A Hint Worth Billions

Kazuo Ueda’s remarks about possible rate hikes deserve separate analysis.

Ueda is known as a cautious and conservative policymaker. He does not make dramatic statements without reason. If he says the Bank of Japan should discuss raising rates, it suggests serious internal deliberations are already underway.

The driving force behind this shift is inflation.

For decades, Japan battled deflation. The Bank of Japan printed money, purchased bonds, and kept interest rates near zero, all in an effort to stimulate growth. Yet prices remained stagnant and economic expansion was sluggish.

Now the environment has changed.

The conflict with Iran has pushed energy prices higher. Japan imports most of its oil and gas. As gasoline, electricity, and heating costs rise, broader inflation follows. Food, clothing, and transportation become more expensive.

Inflation has already exceeded the Bank of Japan’s 2% target, and there is concern that it could climb further. If left unchecked, inflation could erode household savings and undermine economic stability.

That is why Ueda raised the issue of interest rates.

Higher rates are the traditional tool for fighting inflation. More expensive borrowing reduces demand and helps cool price pressures.

The problem is that tighter monetary policy comes at a cost. Japan has become accustomed to cheap money. Businesses have relied on low-cost financing, and households have benefited from extremely affordable mortgages. If rates rise significantly, debt servicing becomes more difficult and bankruptcies could increase.

Ueda understands this. That is why he did not say, “We will raise rates.” Instead, he said, “We need to discuss it.”

He is giving markets time to adjust to the idea.

Markets, however, reacted faster than expected. Stocks fell. The yen strengthened, since higher rates tend to make a currency more attractive. For equities, however, the implications were negative.

What Comes Next?

Thursday’s trading session was a reminder that rallies do not last forever. Sooner or later, every market experiences a correction.

The key question is how deep the correction will be and how long it will last.

Optimists argue this is merely profit-taking after a powerful advance. The fundamental drivers—artificial intelligence, China’s economic recovery, and low U.S. unemployment—remain intact. Once investors digest the Broadcom news and Ueda’s comments, the upward trend could resume.

Pessimists disagree. They argue the problems run deeper. Broadcom suggests AI-chip demand may not be limitless. Ueda signals that the Bank of Japan may be willing to sacrifice growth to fight inflation. And tensions involving Iran could persist for years.

In their view, this is not just a temporary pullback—it could be the beginning of a broader downtrend.

As usual, the truth likely lies somewhere in between.

Markets have become overheated. A correction is both healthy and necessary. It flushes out late-arriving speculators and restores balance. Yet the broader trend may still remain positive. Too much liquidity has been created over recent years. Enthusiasm around AI remains powerful. And the U.S. economy continues to show resilience.

Thursday belongs to the bears.

But Friday comes next. Then another week.

Markets never stand still.

What falls today may rise tomorrow.

Or it may not.

That uncertainty is the risk.

And it is also the opportunity.

Comments

No comments yet. Be the first to share your thoughts!

Authentication Required

You must be logged in to post a comment.